|

Principals Of Managerial Accounting: Homework Chapter 8 Part 2

Tempo

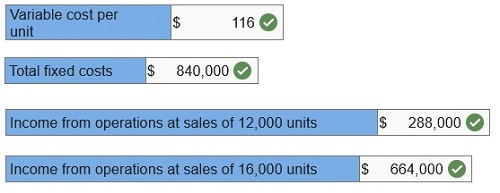

Company’s fixed budget (based on sales of 14,000 units) for the first quarter

reveals the following.

|

Fixed Budget

|

|

Sales (14,000 units × $210 per unit)

|

|

|

|

|

|

$

|

2,940,000

|

|

|

Cost of goods sold

|

|

|

|

|

|

|

|

|

|

Direct materials

|

|

$

|

336,000

|

|

|

|

|

|

|

Direct labor

|

|

|

602,000

|

|

|

|

|

|

|

Production supplies

|

|

|

378,000

|

|

|

|

|

|

|

Plant manager salary

|

|

|

136,000

|

|

|

|

1,452,000

|

|

|

Gross profit

|

|

|

|

|

|

|

1,488,000

|

|

|

Selling expenses

|

|

|

|

|

|

|

|

|

|

Sales commissions

|

|

|

98,000

|

|

|

|

|

|

|

Packaging

|

|

|

210,000

|

|

|

|

|

|

|

Advertising

|

|

|

100,000

|

|

|

|

408,000

|

|

|

Administrative expenses

|

|

|

|

|

|

|

|

|

|

Administrative salaries

|

|

|

186,000

|

|

|

|

|

|

|

Depreciation—office equip.

|

|

|

156,000

|

|

|

|

|

|

|

Insurance

|

|

|

126,000

|

|

|

|

|

|

|

Office rent

|

|

|

136,000

|

|

|

|

604,000

|

|

|

Income from operations

|

|

|

|

|

|

$

|

476,000

|

|

|

|

(1)

Compute the total variable cost per unit.

(2) Compute the total fixed costs.

(3) Compute the income from operations for sales volume of 12,000 units.

(4) Compute the income from operations for sales volume of 16,000 units.

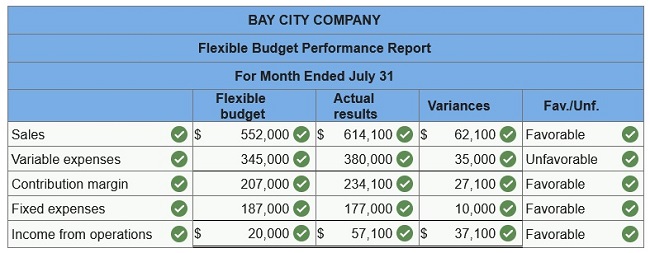

Bay

City Company’s fixed budget performance report for July follows. The $587,000

budgeted total expenses include $400,000 variable expenses and $187,000 fixed

expenses. Actual expenses include $177,000 fixed expenses.

|

Fixed Budget

|

Actual Results

|

Variances

|

|

Sales (in units)

|

|

8,000

|

|

|

6,900

|

|

|

|

|

|

Sales (in dollars)

|

$

|

640,000

|

|

$

|

614,100

|

|

$

|

25,900

|

U

|

|

Total expenses

|

|

587,000

|

|

|

557,000

|

|

|

30,000

|

F

|

|

Income from operations

|

$

|

53,000

|

|

$

|

57,100

|

|

$

|

4,100

|

U

|

|

Prepare

a flexible budget performance report that shows any variances between budgeted

results and actual results. List fixed and variable expenses separately.

(Indicate the effect of each variance by selecting for favorable,

unfavorable, and no variance. Do not round your intermediate calculations.

Round your final answers to whole dollars.)

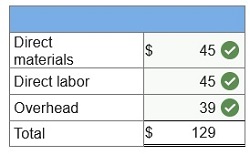

A

manufactured product has the following information for June.

|

Standard

|

Actual

|

|

Direct materials

|

5 lbs. @ $9 per lb.

|

|

42,000

|

lbs. @ $9.10 per lb.

|

|

Direct labor

|

3 hrs. @ $15 per hr.

|

|

24,600

|

hrs. @ $15.40 per hr.

|

|

Overhead

|

3 hrs. @ $13 per hr.

|

$

|

329,400

|

|

|

Units manufactured

|

|

|

8,300

|

|

|

|

(1)

Compute the standard cost per unit.

(2) Compute the total cost variance for June.

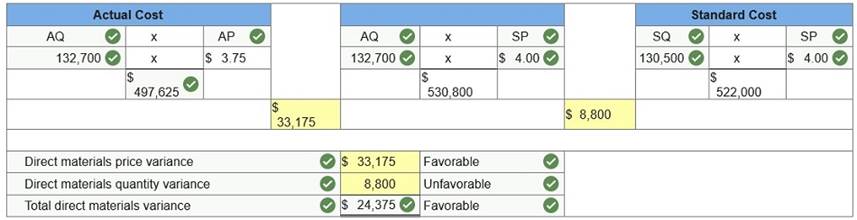

Reed

Corp. has set the following standard direct materials and direct labor costs

per unit for the product it manufactures.

|

|

|

|

|

|

Direct materials (15 lbs. @ $4 per

lb.)

|

|

|

$60

|

|

|

Direct labor (4 hrs. @ $15 per hr.)

|

|

|

60

|

|

|

|

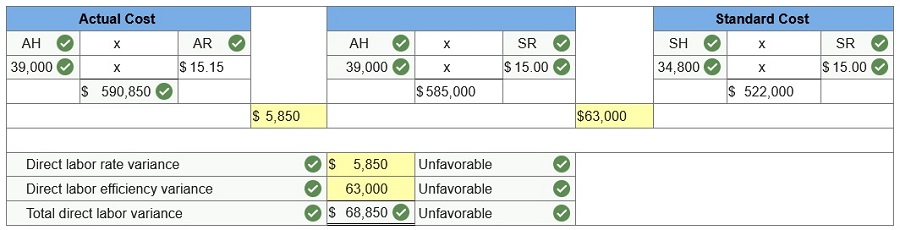

During June the company incurred the following actual costs to

produce 8,700 units.

|

|

|

|

|

|

Direct materials (132,700 lbs. @ $3.75

per lb.)

|

|

$

|

497,625

|

|

|

Direct labor (39,000 hrs. @ $15.15 per

hr.).

|

|

|

590,850

|

|

|

|

AH = Actual Hours

SH = Standard Hours

AR = Actual Rate

SR = Standard Rate

AQ = Actual Quantity

SQ = Standard Quantity

AP = Actual Price

SP = Standard Price

(1) Compute the direct

materials price and quantity variances.

(Indicate the effect of

each variance by selecting for favorable, unfavorable, and no variance.)

(2) Compute the direct

labor rate variance and the direct labor efficiency variance.

(Indicate the effect of

each variance by selecting for favorable, unfavorable, and no variance.)

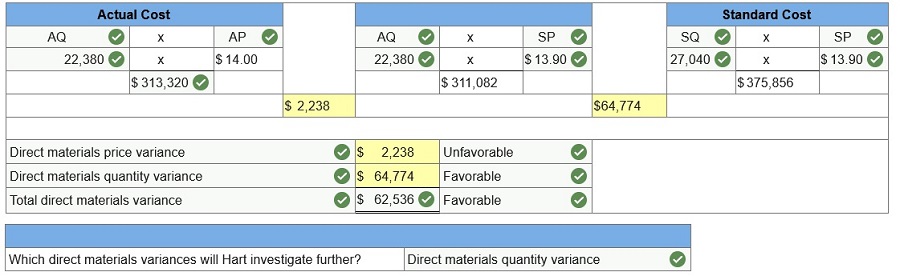

Hart

Company made 3,380 bookshelves using 22,380 board feet of wood costing $313,320.

The company’s direct materials

standards for one bookshelf are 8 board feet of

wood at $13.90 per board foot.

AQ

= Actual Quantity

SQ = Standard Quantity

AP = Actual Price

SP = Standard Price

(1)

Compute the direct materials price and quantity variances and classify each as

favorable or unfavorable.

(2) Hart applies management by exception by investigating direct materials

variances of more than 5% of actual direct materials costs.

Which

direct materials variances will Hart investigate further?

Hart

Company made 3,380 bookshelves using 22,380 board feet of wood costing

$313,320. The company’s direct materials standards for one bookshelf are 8

board feet of wood at $13.90 per board foot.

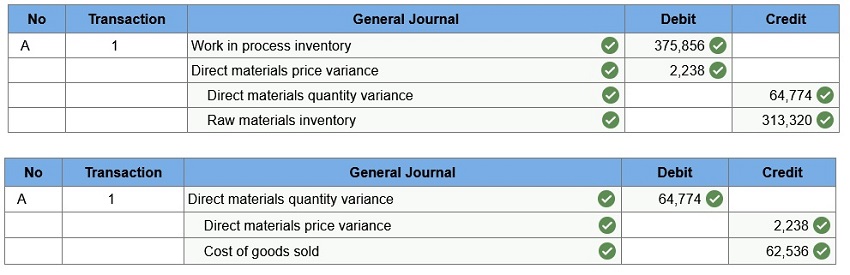

Hart

Company uses a standard costing system.

(1)

Prepare the journal entry to charge direct materials costs to Work in Process

Inventory and record the materials variances.

(2) Assume that Hart’s materials variances are the only variances accumulated

in the accounting period and that they are immaterial. Prepare the adjusting

journal entry to close the variance accounts at period-end.

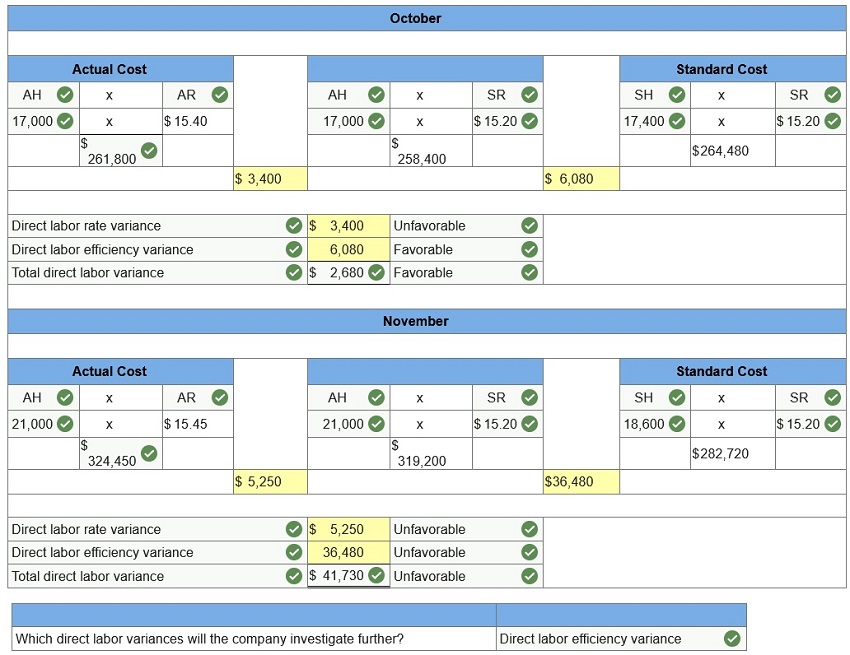

Javonte

Co. set standards of 3 hours of direct labor per unit of product and $15.20 per

hour for the labor rate. During October, the company uses 17,000 hours of

direct labor at a $261,800 total cost to produce 5,800 units of product. In

November, the company uses 21,000 hours of direct labor at a $324,450 total

cost to produce 6,200 units of product.

AH

= Actual Hours

SH = Standard Hours

AR = Actual Rate

SR = Standard Rate

(1)

Compute the direct labor rate variance, the direct labor efficiency variance,

and the total direct labor cost variance for each of these two months. Classify

each variance as favorable or unfavorable.

(2) Javonte investigates variances of more than 5% of actual direct labor cost.

Which direct labor variances will the company investigate further?

Sedona

Company set the following standard costs for one unit of its product for this

year.

|

|

|

|

|

|

Direct material (30 Ibs. @ $2.30 per

Ib.)

|

|

$

|

69.00

|

|

|

Direct labor (20 hrs. @ $4.30 per hr.)

|

|

|

86.00

|

|

|

Variable overhead (20 hrs. @ $2.30 per

hr.)

|

|

|

46.00

|

|

|

Fixed overhead (20 hrs. @ $1.20 per

hr.)

|

|

|

24.00

|

|

|

Total standard cost

|

|

$

|

225.00

|

|

|

|

The

$3.50 ($2.30 + $1.20) total overhead rate per direct labor hour is based on an

expected operating level equal to 60%

of the factory’s capacity of 69,000 units

per month. The following monthly flexible budget information is also available.

|

|

Operating Levels (% of capacity)

|

|

|

Flexible Budget

|

|

|

55%

|

|

|

|

60%

|

|

|

|

65%

|

|

|

Budgeted output (units)

|

|

|

37,950

|

|

|

|

41,400

|

|

|

|

44,850

|

|

|

Budgeted labor (standard hours)

|

|

|

759,000

|

|

|

|

828,000

|

|

|

|

897,000

|

|

|

Budgeted overhead (dollars)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Variable overhead

|

|

$

|

1,745,700

|

|

|

$

|

1,904,400

|

|

|

$

|

2,063,100

|

|

|

Fixed overhead

|

|

|

993,600

|

|

|

|

993,600

|

|

|

|

993,600

|

|

|

Total overhead

|

|

$

|

2,739,300

|

|

|

$

|

2,898,000

|

|

|

$

|

3,056,700

|

|

|

|

During

the current month, the company operated at 55% of capacity, employees worked

731,000 hours, and the following

actual overhead costs were incurred.

|

|

|

|

|

|

Variable overhead costs

|

|

$

|

1,710,000

|

|

|

Fixed overhead costs

|

|

|

1,031,500

|

|

|

Total overhead costs

|

|

$

|

2,741,500

|

|

|

|

|

|

|

|

|

|

Sedona

Company set the following standard costs for one unit of its product for this

year.

|

|

|

|

|

|

Direct material (30 Ibs. @ $2.30 per Ib.)

|

|

$

|

69.00

|

|

|

Direct labor (20 hrs. @ $4.30 per hr.)

|

|

|

86.00

|

|

|

Variable overhead (20 hrs. @ $2.30 per

hr.)

|

|

|

46.00

|

|

|

Fixed overhead (20 hrs. @ $1.20 per

hr.)

|

|

|

24.00

|

|

|

Total standard cost

|

|

$

|

225.00

|

|

|

|

The

$3.50 ($2.30 + $1.20) total overhead rate per direct labor hour is based on an

expected operating level equal to

60% of the factory’s capacity of 69,000 units

per month. The following monthly flexible budget information is also available.

|

|

Operating Levels (% of capacity)

|

|

|

Flexible Budget

|

|

|

55%

|

|

|

|

60%

|

|

|

|

65%

|

|

|

Budgeted output (units)

|

|

|

37,950

|

|

|

|

41,400

|

|

|

|

44,850

|

|

|

Budgeted labor (standard hours)

|

|

|

759,000

|

|

|

|

828,000

|

|

|

|

897,000

|

|

|

Budgeted overhead (dollars)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Variable overhead

|

|

$

|

1,745,700

|

|

|

$

|

1,904,400

|

|

|

$

|

2,063,100

|

|

|

Fixed overhead

|

|

|

993,600

|

|

|

|

993,600

|

|

|

|

993,600

|

|

|

Total overhead

|

|

$

|

2,739,300

|

|

|

$

|

2,898,000

|

|

|

$

|

3,056,700

|

|

|

|

During

the current month, the company operated at 55% of capacity, employees worked

731,000 hours,

and the following actual overhead costs were incurred.

|

|

|

|

|

|

Variable overhead costs

|

|

$

|

1,710,000

|

|

|

Fixed overhead costs

|

|

|

1,031,500

|

|

|

Total overhead costs

|

|

$

|

2,741,500

|

|

|

|

AH

= Actual Hours

SH = Standard Hours

AVR = Actual Variable Rate

SVR = Standard Variable Rate

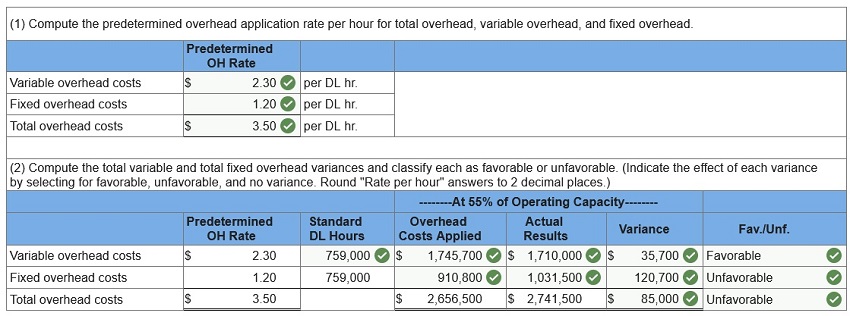

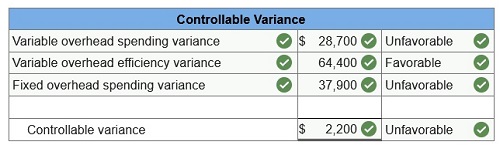

1. Compute the variable overhead spending and efficiency variances.

2. Compute the fixed overhead spending and volume variances and classify each

as favorable or unfavorable.

3. Compute the controllable variance.

Q10.

World Company expects to operate at 70% of its productive capacity of 38,000

units per month. At this planned level, the

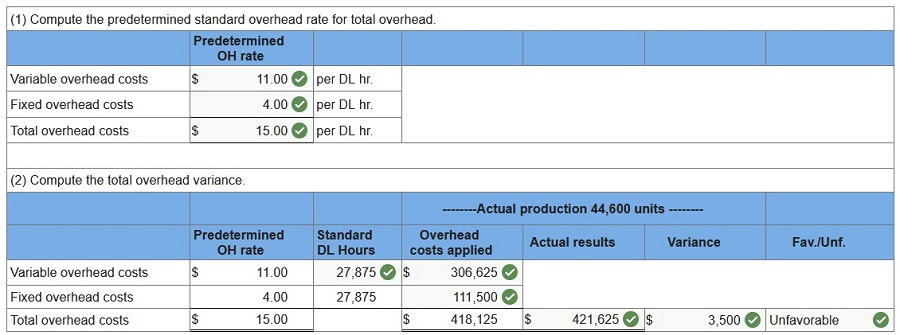

Q10.

World Company expects to operate at 70% of its productive capacity of 38,000

units per month. At this planned level, the

company expects to use 16,625

standard hours of direct labor. Overhead is allocated to products using a

predetermined standard

rate of 0.625 direct labor hour per unit. At the 70%

capacity level, the total budgeted cost includes $66,500 fixed overhead cost

and

$182,875 variable overhead cost. In the current month, the company incurred

$421,625 actual overhead and 16,405 actual labor

hours while producing 44,600

units. (Indicate the effect of each variance by selecting for favorable,

unfavorable, and no variance.

Do not round intermediate calculations. Round “OH

costs per DL hour” to 2 decimal places.)

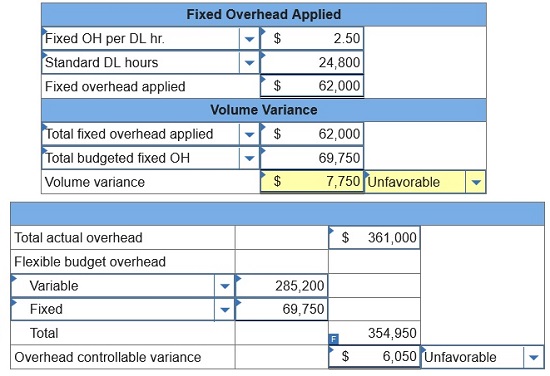

World

Company expects to operate at 80% of its productive capacity of 56,250 units

per month. At this planned level, the company expects to use 27,900 standard

hours of direct labor. Overhead is allocated to products using a predetermined

standard rate of 0.620 direct labor hour per unit. At the 80% capacity level,

the total budgeted cost includes $69,750 fixed overhead cost and $320,850

variable overhead cost. In the current month, the company incurred $361,000

actual overhead and 24,900 actual labor hours while producing 40,000 units.

(1)

Compute the overhead volume variance. Classify each as favorable or

unfavorable.

(2) Compute the overhead controllable variance. Classify each as favorable or

unfavorable.

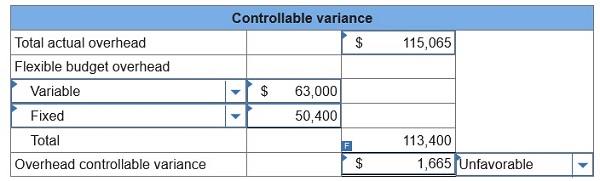

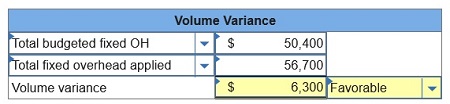

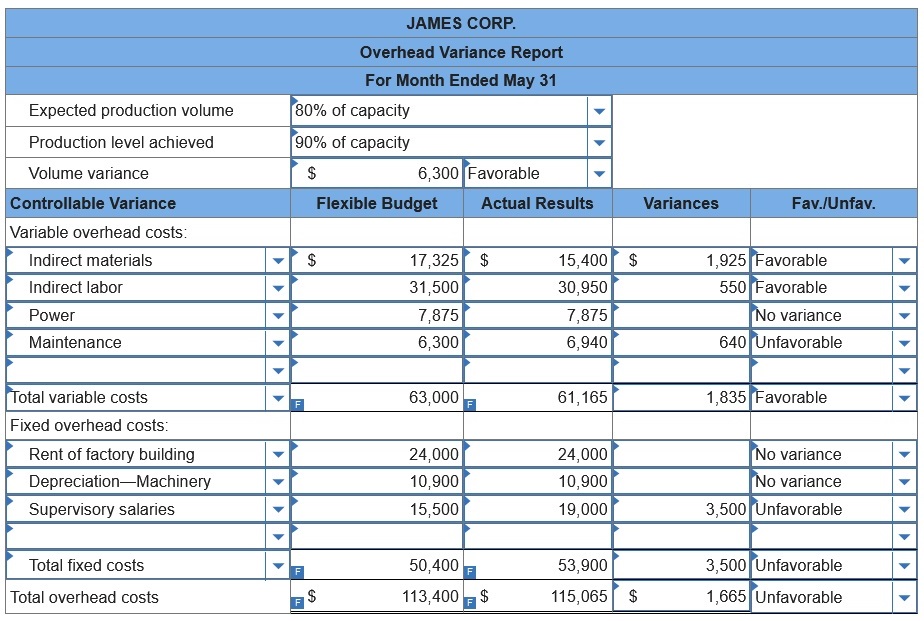

James

Corp. applies overhead on the basis of direct labor hours. For the month of

May, the company planned production of

10,000 units (80% of its production

capacity of 12,500 units) and prepared the following overhead budget:

|

Operating Levels

|

|

Overhead Budget

|

80%

|

|

Production in units

|

|

10,000

|

|

|

Standard direct labor hours

|

|

28,000

|

|

|

Budgeted overhead

|

|

|

|

|

Variable overhead costs

|

|

|

|

|

Indirect materials

|

$

|

15,400

|

|

|

Indirect labor

|

|

28,000

|

|

|

Power

|

|

7,000

|

|

|

Maintenance

|

|

5,600

|

|

|

Total variable costs

|

|

56,000

|

|

|

Fixed overhead costs

|

|

|

|

|

Rent of factory building

|

|

24,000

|

|

|

Depreciation—Machinery

|

|

10,900

|

|

|

Supervisory salaries

|

|

15,500

|

|

|

Total fixed costs

|

|

50,400

|

|

|

Total overhead costs

|

$

|

106,400

|

|

|

|

During

May, the company operated at 90% capacity (11,250 units) and incurred the

following actual overhead costs:

|

Overhead costs (actual)

|

|

Indirect materials

|

$

|

15,400

|

|

|

Indirect labor

|

|

30,950

|

|

|

Power

|

|

7,875

|

|

|

Maintenance

|

|

6,940

|

|

|

Rent of factory building

|

|

24,000

|

|

|

Depreciation—Machinery

|

|

10,900

|

|

|

Supervisory salaries

|

|

19,000

|

|

|

Total actual overhead costs

|

$

|

115,065

|

|

|

|

1. Compute the overhead

controllable variance and classify it as favorable or unfavorable.

2. Compute the overhead

volume variance and classify it as favorable or unfavorable.

3. Prepare an overhead variance report at the actual activity level of 11,250

units.

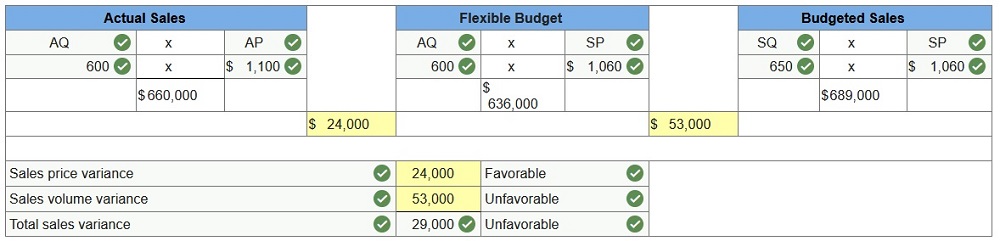

Comp Wiz sells computers.

During May, it sold 600 computers at a $1,100 average price each.

The May fixed budget

included sales of 650 computers at an average price of $1,060 each.

AQ = Actual Quantity

SQ = Standard Quantity

AP = Actual Price

SP = Standard Price

1&2. Compute the sales

price variance and the sales volume variance for May.

Classify it as favorable

or unfavorable. (Indicate the effect of each variance by selecting for

favorable, unfavorable, and no variance.)

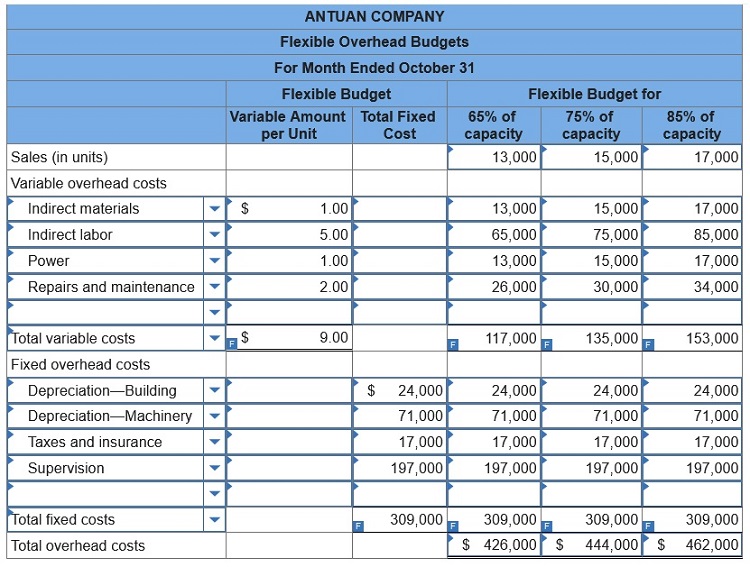

Antuan

Company set the following standard costs for one unit of its product.

|

|

|

|

Direct materials (4.0 Ibs. @ $4.00 per

Ib.)

|

$

|

16.00

|

|

Direct labor (1.6 hrs. @ $11.00 per

hr.)

|

|

17.60

|

|

Overhead (1.6 hrs. @ $18.50 per hr.)

|

|

29.60

|

|

Total standard cost

|

$

|

63.20

|

|

|

The predetermined overhead

rate ($18.50 per direct labor hour) is based on an expected volume of 75% of

the factory’s capacity

of 20,000 units per month. Following are the company’s

budgeted overhead costs per month at the 75% capacity level.

|

Overhead Budget (75% Capacity)

|

|

Variable overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

15,000

|

|

|

|

|

Indirect labor

|

|

75,000

|

|

|

|

|

Power

|

|

15,000

|

|

|

|

|

Repairs and maintenance

|

|

30,000

|

|

|

|

|

Total variable overhead costs

|

|

|

|

$

|

135,000

|

|

Fixed overhead costs

|

|

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

71,000

|

|

|

|

|

Taxes and insurance

|

|

17,000

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

|

|

Total fixed overhead costs

|

|

|

|

|

309,000

|

|

Total overhead costs

|

|

|

|

$

|

444,000

|

|

|

The

company incurred the following actual costs when it operated at 75% of capacity

in October.

|

|

|

|

|

|

|

Direct materials (61,000 Ibs. @ $4.10

per lb.)

|

|

|

|

$

|

250,100

|

|

Direct labor (20,000 hrs. @ $11.20 per

hr.)

|

|

|

|

|

224,000

|

|

Overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

41,600

|

|

|

|

|

Indirect labor

|

|

176,450

|

|

|

|

|

Power

|

|

17,250

|

|

|

|

|

Repairs and maintenance

|

|

34,500

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

95,850

|

|

|

|

|

Taxes and insurance

|

|

15,300

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

601,950

|

|

Total costs

|

|

|

|

$

|

1,076,050

|

|

|

Required:

1&2. Prepare flexible overhead budgets for October showing the amounts of

each variable and fixed cost at the 65%, 75%,

and 85% capacity levels and

classify all items listed in the fixed budget as variable or fixed.

Antuan Company set the

following standard costs for one unit of its product.

|

|

|

|

Direct materials (4.0 Ibs. @ $4.00 per

Ib.)

|

$

|

16.00

|

|

Direct labor (1.6 hrs. @ $11.00 per

hr.)

|

|

17.60

|

|

Overhead (1.6 hrs. @ $18.50 per hr.)

|

|

29.60

|

|

Total standard cost

|

$

|

63.20

|

|

|

|

|

|

|

|

The

predetermined overhead rate ($18.50 per direct labor hour) is based on an

expected volume of 75% of the factory’s capacity

of 20,000 units per month.

Following are the company’s budgeted overhead costs per month at the 75%

capacity level.

|

Overhead Budget (75% Capacity)

|

|

Variable overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

15,000

|

|

|

|

|

Indirect labor

|

|

75,000

|

|

|

|

|

Power

|

|

15,000

|

|

|

|

|

Repairs and maintenance

|

|

30,000

|

|

|

|

|

Total variable overhead costs

|

|

|

|

$

|

135,000

|

|

Fixed overhead costs

|

|

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

71,000

|

|

|

|

|

Taxes and insurance

|

|

17,000

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

|

|

Total fixed overhead costs

|

|

|

|

|

309,000

|

|

Total overhead costs

|

|

|

|

$

|

444,000

|

|

|

The

company incurred the following actual costs when it operated at 75% of capacity

in October.

|

|

|

|

|

|

|

Direct materials (61,000 Ibs. @ $4.10

per lb.)

|

|

|

|

$

|

250,100

|

|

Direct labor (20,000 hrs. @ $11.20 per

hr.)

|

|

|

|

|

224,000

|

|

Overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

41,600

|

|

|

|

|

Indirect labor

|

|

176,450

|

|

|

|

|

Power

|

|

17,250

|

|

|

|

|

Repairs and maintenance

|

|

34,500

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

95,850

|

|

|

|

|

Taxes and insurance

|

|

15,300

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

601,950

|

|

Total costs

|

|

|

|

$

|

1,076,050

|

|

|

3.

Compute the direct materials cost variance, including its price and quantity

variances. (Indicate the effect of each

variance by selecting for

favorable, unfavorable, and No variance.)

Antuan

Company set the following standard costs for one unit of its product.

|

|

|

|

Direct materials (4.0 Ibs. @ $4.00 per

Ib.)

|

$

|

16.00

|

|

Direct labor (1.6 hrs. @ $11.00 per

hr.)

|

|

17.60

|

|

Overhead (1.6 hrs. @ $18.50 per hr.)

|

|

29.60

|

|

Total standard cost

|

$

|

63.20

|

|

|

The

predetermined overhead rate ($18.50 per direct labor hour) is based on an

expected volume of 75% of the factory’s capacity

of 20,000 units per month.

Following are the company’s budgeted overhead costs per month at the 75%

capacity level.

|

Overhead Budget (75% Capacity)

|

|

Variable overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

15,000

|

|

|

|

|

Indirect labor

|

|

75,000

|

|

|

|

|

Power

|

|

15,000

|

|

|

|

|

Repairs and maintenance

|

|

30,000

|

|

|

|

|

Total variable overhead costs

|

|

|

|

$

|

135,000

|

|

Fixed overhead costs

|

|

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

71,000

|

|

|

|

|

Taxes and insurance

|

|

17,000

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

|

|

Total fixed overhead costs

|

|

|

|

|

309,000

|

|

Total overhead costs

|

|

|

|

$

|

444,000

|

|

|

The

company incurred the following actual costs when it operated at 75% of capacity

in October.

|

|

|

|

|

|

|

Direct materials (61,000 Ibs. @ $4.10

per lb.)

|

|

|

|

$

|

250,100

|

|

Direct labor (20,000 hrs. @ $11.20 per

hr.)

|

|

|

|

|

224,000

|

|

Overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

41,600

|

|

|

|

|

Indirect labor

|

|

176,450

|

|

|

|

|

Power

|

|

17,250

|

|

|

|

|

Repairs and maintenance

|

|

34,500

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

95,850

|

|

|

|

|

Taxes and insurance

|

|

15,300

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

601,950

|

|

Total costs

|

|

|

|

$

|

1,076,050

|

|

|

4.

Compute the direct labor cost variance, including its rate and efficiency

variances. (Indicate the effect of each variance by selecting for

favorable, unfavorable, and No variance. Round “Rate per hour” answers to two

decimal places.)

Antuan Company set the

following standard costs for one unit of its product.

|

|

|

|

Direct materials (4.0 Ibs. @ $4.00 per

Ib.)

|

$

|

16.00

|

|

Direct labor (1.6 hrs. @ $11.00 per

hr.)

|

|

17.60

|

|

Overhead (1.6 hrs. @ $18.50 per hr.)

|

|

29.60

|

|

Total standard cost

|

$

|

63.20

|

|

|

The

predetermined overhead rate ($18.50 per direct labor hour) is based on an

expected volume of 75% of the factory’s

capacity of 20,000 units per month.

Following are the company’s budgeted overhead costs per month at the 75%

capacity level.

|

Overhead Budget (75% Capacity)

|

|

Variable overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

15,000

|

|

|

|

|

Indirect labor

|

|

75,000

|

|

|

|

|

Power

|

|

15,000

|

|

|

|

|

Repairs and maintenance

|

|

30,000

|

|

|

|

|

Total variable overhead costs

|

|

|

|

$

|

135,000

|

|

Fixed overhead costs

|

|

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

71,000

|

|

|

|

|

Taxes and insurance

|

|

17,000

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

|

|

Total fixed overhead costs

|

|

|

|

|

309,000

|

|

Total overhead costs

|

|

|

|

$

|

444,000

|

|

|

The

company incurred the following actual costs when it operated at 75% of capacity

in October.

|

|

|

|

|

|

|

Direct materials (61,000 Ibs. @ $4.10 per lb.)

|

|

|

|

$

|

250,100

|

|

Direct labor (20,000 hrs. @ $11.20 per hr.)

|

|

|

|

|

224,000

|

|

Overhead costs

|

|

|

|

|

|

|

Indirect materials

|

$

|

41,600

|

|

|

|

|

Indirect labor

|

|

176,450

|

|

|

|

|

Power

|

|

17,250

|

|

|

|

|

Repairs and maintenance

|

|

34,500

|

|

|

|

|

Depreciation—Building

|

|

24,000

|

|

|

|

|

Depreciation—Machinery

|

|

95,850

|

|

|

|

|

Taxes and insurance

|

|

15,300

|

|

|

|

|

Supervision

|

|

197,000

|

|

|

601,950

|

|

Total costs

|

|

|

|

$

|

1,076,050

|

|

|

Spot Company's master budget shows expected sales of

10,000 units and expected production of 11,000 units for the month of March.

Each unit requires 1/2 hour of direct labor. The direct labor rate is $15.00

per hour. Calculate the expected total direct labor cost for t

he month of March:

$82,000

11,000 x 1/2 x 15 = 82,500

Carter Production Inc required production for the

first six month of the year is as follows

Jan 50,000

Feb 70,000

Mar 85,000

Apr 105,000

May 110,000

Jun 120,000

Each unit requires two pounds of material. Given a desired ending inventory of

20% of the next month's

production needs, the pounds of material to be

purchased in April is:

212,000 pounds

(105,000 x 2) + (110,000 x 2 x .20) 44,000 -

(.20% x 105,000) = 212,000

A company's flexible budget for

15,000 units of production showed sales, $90,000; variable costs,

$37,500; and

fixed costs, $25,000. The sales expected if the company produces and sells

19,000 units is:

$114,000

90,000

/ 15,000 units = 6.00

6.00

× 19,000 units = 114,000

|