|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Principals Of Managerial Accounting: Homework Chapter 4 Part 2 Homework 1.1 1.2 2.1 2.2 3.1 3.2 4.1 4.2 5.1 5.2 6.1 6.2 7.1 7.2 8.1 8.2 9.1 9.2 10.1 10.2 11.1 11.2 12.1 12.2 13.1 13.2 14.1 14.2 15.1 15.2

Learnsmart 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Final Exam 1 2 Homework Help?

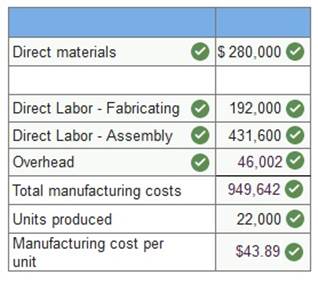

Laval produces lamps and

home lighting fixtures. Its most popular product is a brushed aluminum desk

lamp.

This lamp is made from components shaped in the fabricating department and assembled in the assembly department. Information related to the 22,000 desk lamps produced annually follows.

Expected overhead cost and related data for the two production departments follow.

Required 1. Determine the plantwide overhead rate for Laval using direct labor hours as a base. 2. Determine the total manufacturing cost per unit for the aluminum desk lamp using the plantwide overhead rate. 3. Compute departmental overhead rates based on machine hours in the fabricating department and direct labor hours in the assembly department. 4. Use departmental overhead rates from requirement 3 to determine the total manufacturing cost per unit for the aluminum desk lamps. 1. Determine the plantwide overhead rate for Laval using direct labor hours as a base.

2. Determine the total manufacturing cost per unit for the aluminum desk lamp using the plantwide overhead rate.

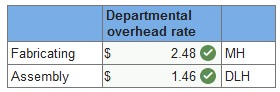

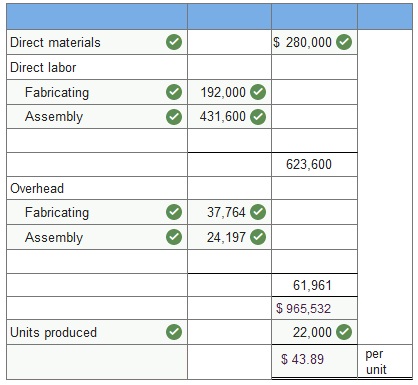

3. Compute departmental overhead rates based on machine hours in the fabricating department and direct labor hours in the assembly department.

4. Use departmental overhead rates from requirement 3 to determine the total manufacturing cost per unit for the aluminum desk lamps.

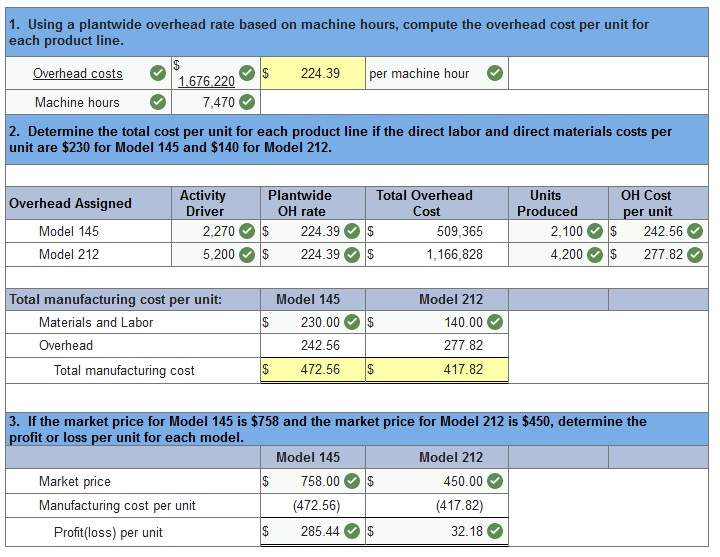

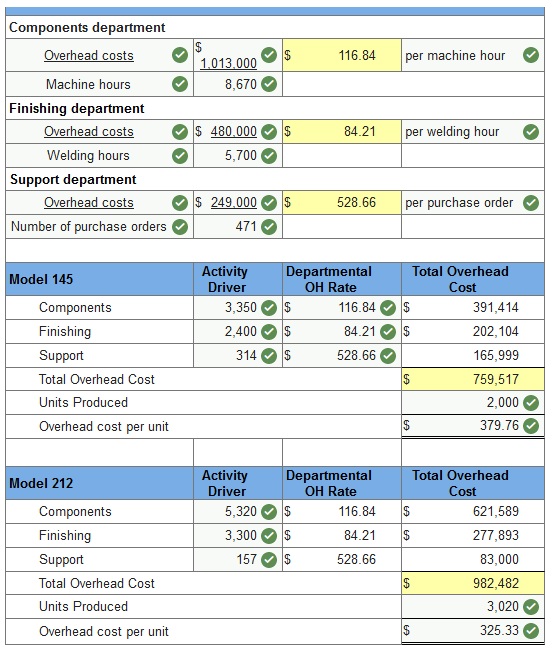

Way Cool produces two different models of air conditioners. The company produces the mechanical systems in their components department. The mechanical systems are combined with the housing assembly in its finishing department. The activities, costs, and drivers associated with these two manufacturing processes and the production support process follow. (Loss amounts should be indicated with a minus sign. Round your intermediate calculations and round “Cost per unit and OH rate” answers to 2 decimal places.)

Additional production information concerning its two product lines follows.

Way Cool produces two different models of air conditioners. The company produces the mechanical systems in their components department. The mechanical systems are combined with the housing assembly in its finishing department. The activities, costs, and drivers associated with these two manufacturing processes and the production support process follow.

Additional production information concerning its two product lines follows.

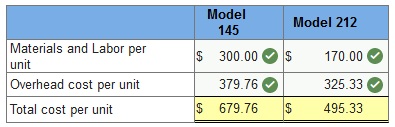

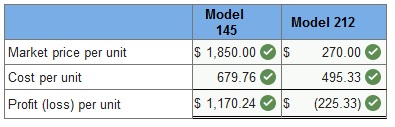

Required: 1. Determine departmental overhead rates and compute the overhead cost per unit for each product line. Base your overhead assignment for the components department on machine hours. Use welding hours to assign overhead costs to the finishing department. Assign costs to the support department based on number of purchase orders. 2. Determine the total cost per unit for each product line if the direct labor and direct materials costs per unit are $300 for Model 145 and $170 for Model 212. 3. If the market price for Model 145 is $1,850 and the market price for Model 212 is $270, determine the profit or loss per unit for each model. 1. Determine departmental overhead rates and compute the overhead cost per unit for each product line. Base your overhead assignment for the components department on machine hours. Use welding hours to assign overhead costs to the finishing department. Assign costs to the support department based on number of purchase orders.

2. Determine the total cost per unit for each product line if the direct labor and direct materials costs per unit are $300 for Model 145 and $170 for Model 212.

3. If the market price for Model 145 is $1,850 and the market price for Model 212 is $270 determine the profit or loss per unit for each model.

Way Cool produces two different models of air conditioners. The company produces the mechanical systems in their components department. The mechanical systems are combined with the housing assembly in its finishing department. The activities, costs, and drivers associated with these two manufacturing processes and the production support process follow.

Additional production information concerning its two product lines follows. Model 145 Model 212

1. Using ABC, compute the overhead cost per unit for each product line. (Round your intermediate calculations and round activity rate and cost per unit answers to 2 decimal places.) 2. Determine the total cost per unit for each product line if the direct labor and direct materials costs per unit are $210 for Model 145 and $116 for Model 212. (Round your final answers to 2 decimals places.) 3. Assume if the market price for Model 145 is $862.41 and the market price for Model 212 is $470.79, determine the profit or loss per unit for each model. (Round your final answers to 2 decimals places.) 1. Using ABC, compute the overhead cost per unit for each product line. (Round your intermediate calculations and round activity rate and cost per unit answers to 2 decimal places.)

2. Calculation of total cost per unit for each product line if the direct labor and direct materials costs per unit are $210 for Model 145 and $116 for Model 212

All of the following statements are correct when referring to process costing except: A) Process costing would be appropriate for a jeweler who makes custom jewelry to order. B) A process costing system has the same basic purposes as a job‐order costing system. C) Units produced are indistinguishable from each other. D) Costs are accumulated by department Jared Beverage Corporation uses a process costing system to collect costs related to the production of its celery flavored cola. The cola is first processed in a Mixing Department and is then transferred out and finished up in the Bottling Department. The finished cases of cola are then transferred to Finished Goods Inventory. The following information relates to the company's two departments for the month of Jan.:

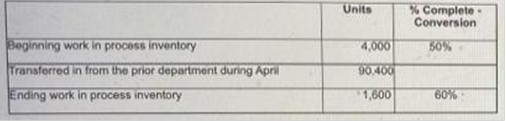

How many cases of cola were completed and transferred to Finished Goods Inventory during January? A) 70,000 B) 63,000 C) 58,000 D) 77,000 5,000 + 65,000 - 7,000 = 63,000 Janner Corp uses the weighted average method in its process costing system. Operating data for the painting department for the month of April appear below:

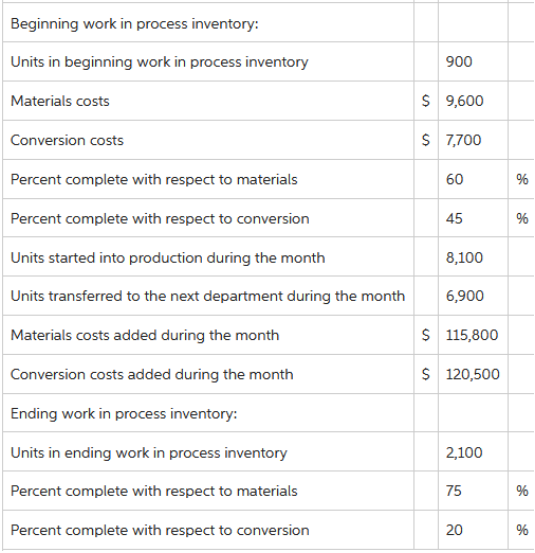

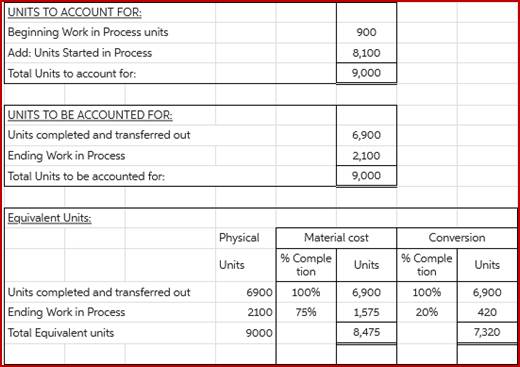

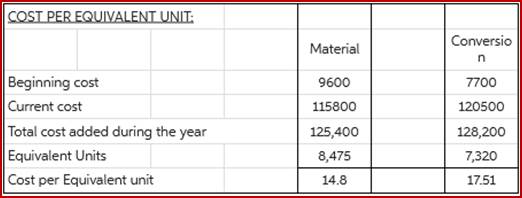

What were the equivalent units for conversion costs in the painting department for april? A) 93,760 B) 92,800 C) 91,360 D) 88,000 90,400 units - 1,600 units = 88,800 4,000 + 88,800 units + (1,600 × 0.60) = 4,000 + 88,800 + 960 = 93,760 Nabais Corporation uses the weighted‐average method in its process costing system. Operating data for the Lubricating Department for the month of October appear below: Beginning work in process inventory 3,300 80 % Transferred in from the prior department during October 30,700 Completed and transferred to the next department during October 32,200 Ending work in process inventory 1,800 60 % What were the equivalent units for conversion costs in the Lubrication Department for October? A) 31,780 B) 33,280 C) 32,200 D) 29,200 32,200 + (1,800 x 0.60) = 33,280 units Lap Corporation uses the weighted‐average method in its process costing system. The beginning work in process inventory in a particular department consisted of 80,000 units, 100% complete with respect to materials and 25% complete with respect to conversion costs. The total dollar value of this inventory was $226,000. During the month, 150,000 units were transferred out of the department. The costs per equivalent unit for the month were $2.00 for materials and $3.50 for conversion costs. The cost of the units completed and transferred out of the department was: A) $681,000 B) $765,000 C) $821,000 D) $825,000 (150,000 x 2) + (150,000 x 3.50) Jublot Corporation uses the weighted average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 900 Materials costs $ 11,200 Conversion costs $ 9,800 Percent complete with respect to materials 60% Percent complete with respect to conversion 40% Units started into production during the month 7,100 Units transferred to the next department during the month 6,000 Materials costs added during the month $ 115,800 Conversion costs added during the month $ 145,800 Ending work in process inventory: Units in ending work in process inventory 2,000 Percent complete with respect to materials 55% Percent complete with respect to conversion 35%: A) $21.76 B) $19.45 C) $34.73 D) $24.38 6,000 + (2,000 x 0.35) = 6,700 9,800 + 145,800 = 155,600 155,600 / 6,700 = 34.73 Lucas Corporation uses the weighted‐average method in its process costing system. Data concerning the first processing department for the most recent month are listed below:

The cost per equivalent unit for conversion costs for the first department for the month is closest to: A) $18.39 B) $16.46 C) $17.51 D) $14.24

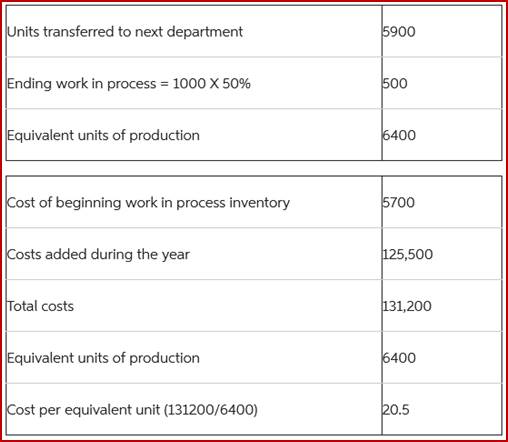

Sumter Corporation uses the weighted‐average method in its process costing system. The following data pertain to operations in the first processing department for a recent month: Work in process, beginning: Units in process 6,000 Percent complete with respect to materials ....... 60% Percent complete with respect to conversion 20% Costs in the beginning inventory: Materials cost............................................ $ 78,200 Conversion cost $ 3,600 Units started during the month ..................................... ? Units completed and transferred out during the month 70,000 Costs added to production during the month: Materials cost ............................................ $ 286,600 Conversion cost ....................................... 216,000 Work in process, ending: Units in process ......................................... 8,000 Percent complete with respect to materials ....... . .... 75% Percent complete with respect to conversion................ 25% What was the cost per equivalent unit for conversion during the month? A) $5.45 B) $6.95 C) $4.00 D) $3.05 70,000 + 8,000 – 6,000 = 72,000 3600 + 216,000 = 219,600 219,600 / 72,000 = 3.05 Annenbaum Corporation uses the weighted‐average method in its process costing system. This month, the beginning inventory in the first processing department consisted of 400 units. The costs and percentage completion of these units in beginning inventory were: Cost % complete Materials costs $5,700 65% Conversion costs $6,800 45% A total of 6,500 units were started and 5,900 units were transferred to the second processing department during the month. The following costs were incurred in the first processing department during the month: Cost Materials costs $125,500 Conversion costs $207,000 The ending inventory was 50% complete with respect to materials and 35% complete with respect to conversion costs. What are the equivalent units for conversion costs for the month in the first processing department? A) 6,250 B) 5,900 C) 350 D) 6,900

Equivalent units of Production Material Conversion Units % Units % Units Units Completed and transferred out 5,900 100% 5,900 100% 5,900 Ending work in process inventory 1,000 50% 500 35% 350 Equivalent units 6,900 6,400 6,250 Annenbaum Corporation uses the weighted‐average method in its process costing system. This month, the beginning inventory in the first processing department consisted of 400 units. The costs and percentage completion of these units in beginning inventory were: Cost Percent Complete Materials costs $ 5,700 65% Conversion costs $ 6,800 45% A total of 6,500 units were started and 5,900 units were transferred to the second processing department during the month. The following costs were incurred in the first processing department during the month: Cost Materials costs $ 125,500 Conversion costs $ 207,000 The ending inventory was 50% complete with respect to materials and 35% complete with respect to conversion costs. The cost of ending work in process inventory in the first processing department according to the company’s cost system is closest to: (Round "Cost per equivalent unit" to 3 decimal places.) A) $19.01 B) $19.61 C) $20.50 D) $18.19 400 + 6500 = Units in ending work in process inventory + 5900 Units in ending work in process inventory = 1000 units

Haffner Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 2,100 Materials costs $ 9,400 Conversion costs $ 10,700 Percent complete with respect to materials 85 % Percent complete with respect to conversion 55 % Units started into production during the month 8,600 Units transferred to the next department during the month 7,700 Materials costs added during the month $ 104,300 Conversion costs added during the month $ 186,000 Ending work in process inventory: Units in ending work in process inventory 3,000 Percent complete with respect to materials 60 % Percent complete with respect to conversion 50 % The cost of ending work in process inventory in the first processing department according to the company's cost system is closest to: (Round "Cost per equivalent unit" to 3 decimal places.) $53,612 Materials Conversion Units transferred to the next department 7,700 Ending work in process: Materials: 3,000 units × .60 = 1,800 Conversion: 3,000 units × .50 1,500 Equivalent units of production 9,500 9,200 Materials Conversion Cost of beginning work in process inventory $ 9,400 $ 10,700 Costs added during the period 104,300 186,000 Total cost (a) $ 113,700 $ 196,700 Equivalent units of production (b) 9,500 9,200 Cost per equivalent unit (a) ÷ (b) $ 11.968 $ 21.380 Materials Conversion Total Ending work in process inventory: Equivalent units of production (a) 1,800 / 1,500 Cost per equivalent unit (b) $ 11.968 / $21.380 Cost of ending work in process inventory (a) × (b) $21,542.400 / $32,070.000 / $53,612 Which of the following statements is correct with regard to a CVP graph? A) A CVP graph shows the maximum possible profit. B) A CVP graph shows the break‐even point as the intersection of the total sales revenue line and the total expense line. C) A CVP graph assumes that total expense varies in direct proportion to unit sales. D) A CVP graph shows the operating leverage as the gap between total sales revenue and total expense at the actual level of sales. Break‐even analysis assumes that: A) Total revenue is constant. B) Unit variable expense is constant. C) Unit fixed expense is constant. D) Selling prices must fall in order to generate more revenue. To obtain the dollar sales volume necessary to attain a given target profit, which of the following formulas should be used? A) (Fixed expenses + Target net profit)/Total contribution margin B) (Fixed expenses + Target net profit)/Contribution margin ratio C) Fixed expenses/Contribution margin per unit D) Target net profit/Contribution margin ratio All of the following statements are correct when referring to process costing except: A) Process costing would be appropriate for a jeweler who makes custom jewelry to order. B) A process costing system has the same basic purposes as a job‐order costing system. C) Units produced are indistinguishable from each other. D) Costs are accumulated by department Jared Beverage Corporation uses a process costing system to collect costs related to the production of its celery flavored cola. The cola is first processed in a Mixing Department and is then transferred out and finished up in the Bottling Department. The finished cases of cola are then transferred to Finished Goods Inventory. The following information relates to the company's two departments for the month of Jan.:

How many cases of cola were completed and transferred to Finished Goods Inventory during January? A) 70,000 B) 63,000 C) 58,000 D) 77,000 5,000 + 65,000 - 7,000 = 63,000 Janner Corp uses the weighted average method in its process costing system. Operating data for the painting department for the month of April appear below:

What were the equivalent units for conversion costs in the painting department for april? A) 93,760 B) 92,800 C) 91,360 D) 88,000 90,400 units - 1,600 units = 88,800 4,000 + 88,800 units + (1,600 × 0.60) = 4,000 + 88,800 + 960 = 93,760 Nabais Corporation uses the weighted‐average method in its process costing system. Operating data for the Lubricating Department for the month of October appear below: Beginning work in process inventory 3,300 80 % Transferred in from the prior department during October 30,700 Completed and transferred to the next department during October 32,200 Ending work in process inventory 1,800 60 % What were the equivalent units for conversion costs in the Lubrication Department for October? A) 31,780 B) 33,280 C) 32,200 D) 29,200 32,200 + (1,800 x 0.60) = 33,280 units Lap Corporation uses the weighted‐average method in its process costing system. The beginning work in process inventory in a particular department consisted of 80,000 units, 100% complete with respect to materials and 25% complete with respect to conversion costs. The total dollar value of this inventory was $226,000. During the month, 150,000 units were transferred out of the department. The costs per equivalent unit for the month were $2.00 for materials and $3.50 for conversion costs. The cost of the units completed and transferred out of the department was: A) $681,000 B) $765,000 C) $821,000 D) $825,000 (150,000 x 2) + (150,000 x 3.50) Jublot Corporation uses the weighted average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 900 Materials costs $ 11,200 Conversion costs $ 9,800 Percent complete with respect to materials 60% Percent complete with respect to conversion 40% Units started into production during the month 7,100 Units transferred to the next department during the month 6,000 Materials costs added during the month $ 115,800 Conversion costs added during the month $ 145,800 Ending work in process inventory: Units in ending work in process inventory 2,000 Percent complete with respect to materials 55% Percent complete with respect to conversion 35%: A) $21.76 B) $19.45 C) $34.73 D) $24.38 6,000 + (2,000 x 0.35) = 6,700 9,800 + 145,800 = 155,600 155,600 / 6,700 = 34.73 Lucas Corporation uses the weighted‐average method in its process costing system. Data concerning the first processing department for the most recent month are listed below:

The cost per equivalent unit for conversion costs for the first department for the month is closest to: A) $18.39 B) $16.46 C) $17.51 D) $14.24

Sumter Corporation uses the weighted‐average method in its process costing system. The following data pertain to operations in the first processing department for a recent month: Work in process, beginning: Units in process 6,000 Percent complete with respect to materials ....... 60% Percent complete with respect to conversion 20% Costs in the beginning inventory: Materials cost............................................ $ 78,200 Conversion cost $ 3,600 Units started during the month ..................................... ? Units completed and transferred out during the month 70,000 Costs added to production during the month: Materials cost ............................................ $ 286,600 Conversion cost ....................................... 216,000 Work in process, ending: Units in process ......................................... 8,000 Percent complete with respect to materials ....... . .... 75% Percent complete with respect to conversion................ 25% What was the cost per equivalent unit for conversion during the month? A) $5.45 B) $6.95 C) $4.00 D) $3.05 70,000 + 8,000 – 6,000 = 72,000 3600 + 216,000 = 219,600 219,600 / 72,000 = 3.05 Annenbaum Corporation uses the weighted‐average method in its process costing system. This month, the beginning inventory in the first processing department consisted of 400 units. The costs and percentage completion of these units in beginning inventory were: Cost % complete Materials costs $5,700 65% Conversion costs $6,800 45% A total of 6,500 units were started and 5,900 units were transferred to the second processing department during the month. The following costs were incurred in the first processing department during the month: Cost Materials costs $125,500 Conversion costs $207,000 The ending inventory was 50% complete with respect to materials and 35% complete with respect to conversion costs. What are the equivalent units for conversion costs for the month in the first processing department? A) 6,250 B) 5,900 C) 350 D) 6,900

Equivalent units of Production Material Conversion Units % Units % Units Units Completed and transferred out 5,900 100% 5,900 100% 5,900 Ending work in process inventory 1,000 50% 500 35% 350 Equivalent units 6,900 6,400 6,250 Annenbaum Corporation uses the weighted‐average method in its process costing system. This month, the beginning inventory in the first processing department consisted of 400 units. The costs and percentage completion of these units in beginning inventory were: Cost Percent Complete Materials costs $ 5,700 65% Conversion costs $ 6,800 45% A total of 6,500 units were started and 5,900 units were transferred to the second processing department during the month. The following costs were incurred in the first processing department during the month: Cost Materials costs $ 125,500 Conversion costs $ 207,000 The ending inventory was 50% complete with respect to materials and 35% complete with respect to conversion costs. The cost of ending work in process inventory in the first processing department according to the company’s cost system is closest to: (Round "Cost per equivalent unit" to 3 decimal places.) A) $19.01 B) $19.61 C) $20.50 D) $18.19 400 + 6500 = Units in ending work in process inventory + 5900 Units in ending work in process inventory = 1000 units

Haffner Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 2,100 Materials costs $ 9,400 Conversion costs $ 10,700 Percent complete with respect to materials 85 % Percent complete with respect to conversion 55 % Units started into production during the month 8,600 Units transferred to the next department during the month 7,700 Materials costs added during the month $ 104,300 Conversion costs added during the month $ 186,000 Ending work in process inventory: Units in ending work in process inventory 3,000 Percent complete with respect to materials 60 % Percent complete with respect to conversion 50 % The cost of ending work in process inventory in the first processing department according to the company's cost system is closest to: (Round "Cost per equivalent unit" to 3 decimal places.) $53,612 Materials Conversion Units transferred to the next department 7,700 Ending work in process: Materials: 3,000 units × .60 = 1,800 Conversion: 3,000 units × .50 1,500 Equivalent units of production 9,500 9,200 Materials Conversion Cost of beginning work in process inventory $ 9,400 $ 10,700 Costs added during the period 104,300 186,000 Total cost (a) $ 113,700 $ 196,700 Equivalent units of production (b) 9,500 9,200 Cost per equivalent unit (a) ÷ (b) $ 11.968 $ 21.380 Materials Conversion Total Ending work in process inventory: Equivalent units of production (a) 1,800 / 1,500 Cost per equivalent unit (b) $ 11.968 / $21.380 Cost of ending work in process inventory (a) × (b) $21,542.400 / $32,070.000 / $53,612 Which of the following statements is correct with regard to a CVP graph? A) A CVP graph shows the maximum possible profit. B) A CVP graph shows the break‐even point as the intersection of the total sales revenue line and the total expense line. C) A CVP graph assumes that total expense varies in direct proportion to unit sales. D) A CVP graph shows the operating leverage as the gap between total sales revenue and total expense at the actual level of sales. Break‐even analysis assumes that: A) Total revenue is constant. B) Unit variable expense is constant. C) Unit fixed expense is constant. D) Selling prices must fall in order to generate more revenue. To obtain the dollar sales volume necessary to attain a given target profit, which of the following formulas should be used? A) (Fixed expenses + Target net profit)/Total contribution margin B) (Fixed expenses + Target net profit)/Contribution margin ratio C) Fixed expenses/Contribution margin per unit D) Target net profit/Contribution margin ratio Homework 1.1 1.2 2.1 2.2 3.1 3.2 4.1 4.2 5.1 5.2 6.1 6.2 7.1 7.2 8.1 8.2 9.1 9.2 10.1 10.2 11.1 11.2 12.1 12.2 13.1 13.2 14.1 14.2 15.1 15.2

Learnsmart 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Final Exam 1 2 Homework Help? |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |