|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Principals Of Managerial Accounting: Homework Chapter 11 Part 1 Homework 1.1 1.2 2.1 2.2 3.1 3.2 4.1 4.2 5.1 5.2 6.1 6.2 7.1 7.2 8.1 8.2 9.1 9.2 10.1 10.2 11.1 11.2 12.1 12.2 13.1 13.2 14.1 14.2 15.1 15.2

Learnsmart 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Final Exam 1 2 Homework Help?

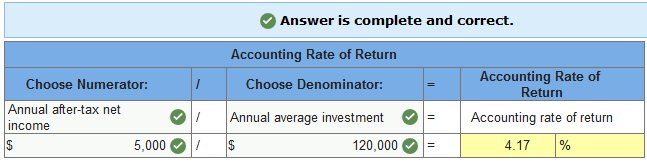

Exercise 11-7 Accounting rate of return LO P2

A machine costs $200,000 and is expected to yield an after-tax net income of $5,000 each year. Management predicts this machine has a 8-year service life and a $40,000 salvage value, and it uses straight-line depreciation. Compute this machine’s accounting rate of return.

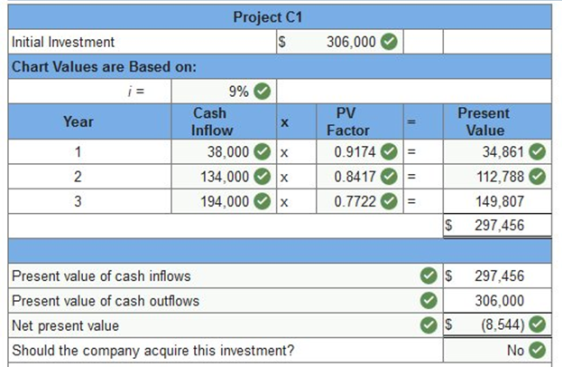

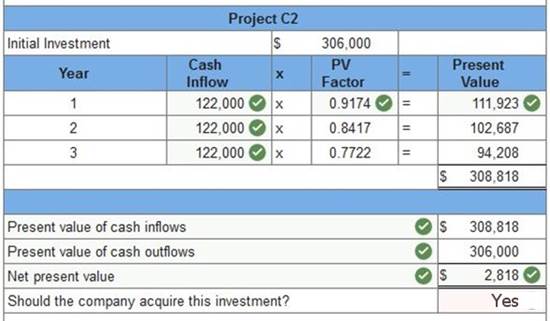

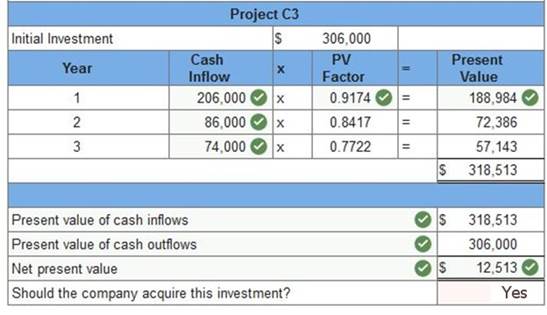

Exercise 11-14 Computation and interpretation of net present value and internal rate of return LO P3, P4 Phoenix Company can invest in each of three cheese-making projects: C1, C2, and C3. Each project requires an initial investment of $306,000 and would yield the following annual cash flows. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.)

(1) Assume that the company requires a 9% return from its investments. Using net present value, determine which projects, if any, should be acquired. (Negative net present values should be indicated with a minus sign. Round your answers to the nearest whole dollar.)

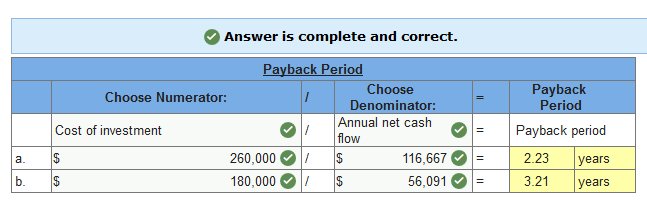

Exercise 11-5 Payback period computation; even cash flows LO P1 Compute the payback period for each of these two separate investments: A new operating system for an existing machine is expected to cost $260,000 and have a useful life of six years. The system yields an incremental after-tax income of $75,000 each year after deducting its straight-line depreciation. The predicted salvage value of the system is $10,000. A machine costs $180,000, has a $14,000 salvage value, is expected to last eleven years, and will generate an after-tax income of $41,000 per year after straight-line depreciation.

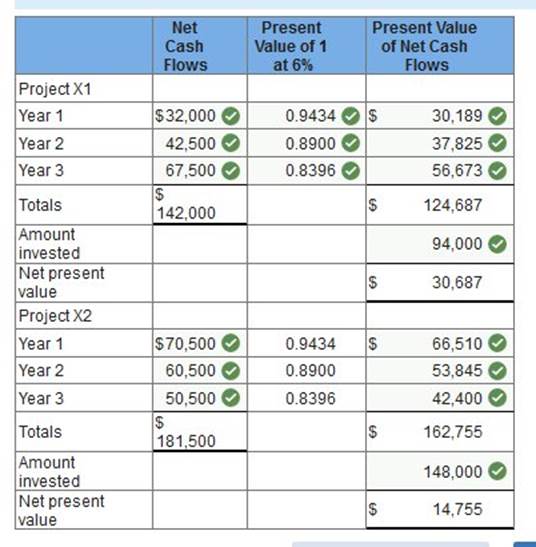

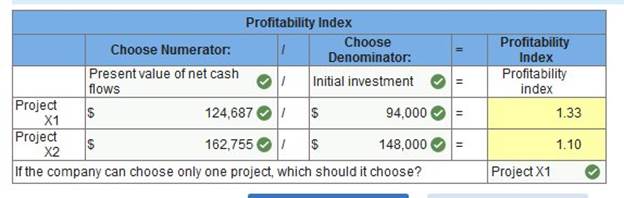

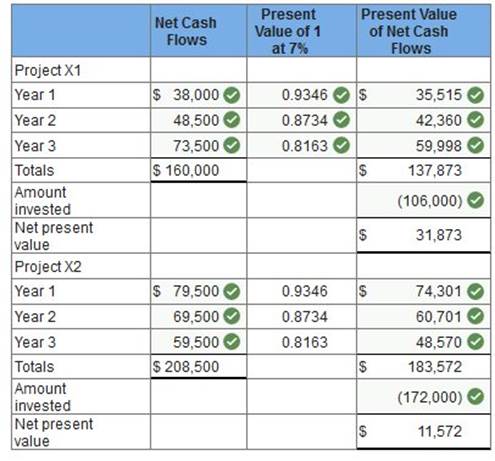

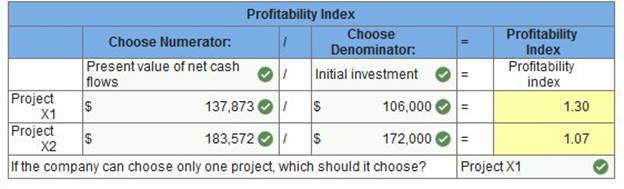

Exercise 11-12 Net present value, profitability index LO P3 Following is information on two alternative investments being considered by Tiger Co. The company requires a 6% return from its investments. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.)

a. Compute each project’s net present value. b. Compute each project’s profitability index. If the company can choose only one project, which should it choose?

Compute each project’s profitability index. If the company can choose only one project, which should it choose?

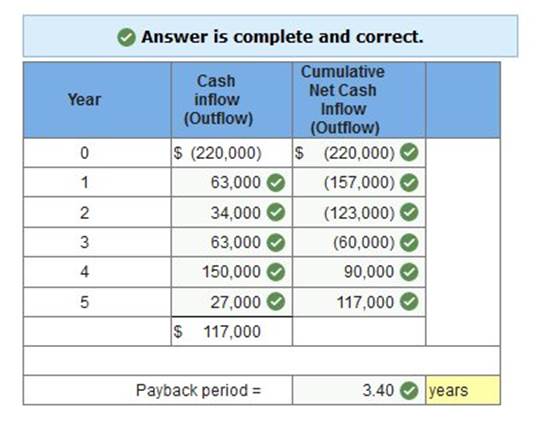

Beyer Company is considering the purchase of an asset for $220,000. It is expected to produce the following net cash flows. The cash flows occur evenly within each year.

Compute the payback period for this investment. (Cumulative net cash outflows must be entered with a minus sign. Round your Payback Period answer to 2 decimal place.)

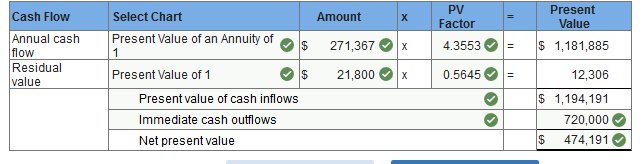

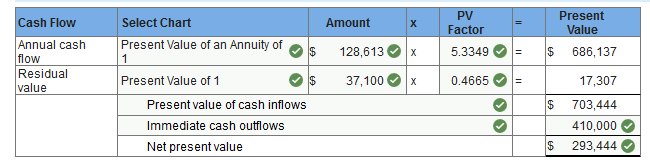

Exercise 11-6 Net present value LO P3 A new operating system for an existing machine is expected to cost $720,000 and have a useful life of six years. The system yields an incremental after-tax income of $155,000 each year after deducting its straight-line depreciation. The predicted salvage value of the system is $21,800. A machine costs $410,000, has a $37,100 salvage value, is expected to last eight years, and will generate an after-tax income of $82,000 per year after straight-line depreciation. Assume the company requires a 10% rate of return on its investments. Compute the net present value of each potential investment. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.) A new operating system for an existing machine is expected to cost $720,000 and have a useful life of six years. The system yields an incremental after-tax income of $155,000 each year after deducting its straight-line depreciation. The predicted salvage value of the system is $21,800. (Round your answers to the nearest whole dollar.) Required A

Required B A machine costs $410,000, has a $37,100 salvage value, is expected to last eight years, and will generate an after-tax income of $82,000 per year after straight-line depreciation. (Round your answers to the nearest whole dollar.)

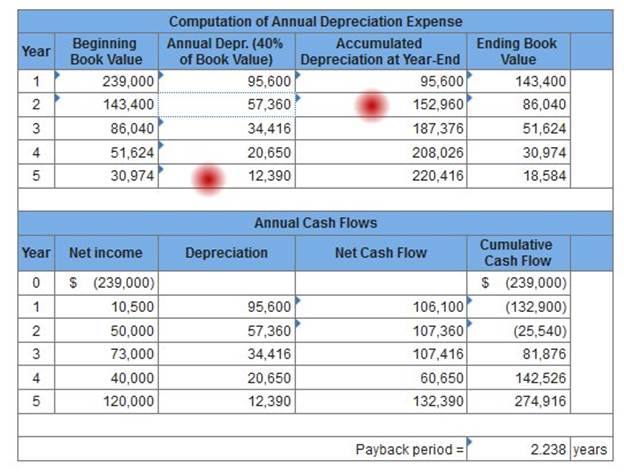

Exercise 11-4 Payback period; accelerated depreciation LO P1 A machine can be purchased for $239,000 and used for five years, yielding the following net incomes. In projecting net incomes, double-declining depreciation is applied, using a five-year life and a zero salvage value.

Compute the machine’s payback period (ignore taxes). (Round payback period answer to 3 decimal places.)

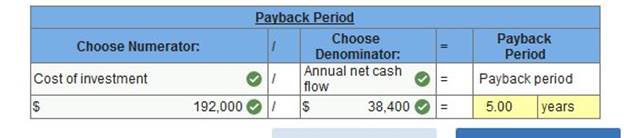

Exercise 11-8 Payback period and accounting rate of return on investment LO P1, P2 B2B Co. is considering the purchase of equipment that would allow the company to add a new product to its line. The equipment is expected to cost $192,000 with a 12-year life and no salvage value. It will be depreciated on a straight-line basis. The company expects to sell 76,800 units of the equipment’s product each year. The expected annual income related to this equipment follows.

1. Compute the payback period.

2. Compute the accounting rate of return for this equipment.

Exercise 11-11 Net present value, profitability index LO P3 Following is information on two alternative investments being considered by Tiger Co. The company requires a 7% return from its investments. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.)

a. Compute each project’s net present value. b. Compute each project’s profitability index. If the company can choose only one project, which should it choose Required A Compute each project’s net present value. (Round your final answers to the nearest dollar.)

Required B Compute each project’s profitability index. If the company can choose only one project, which should it choose?

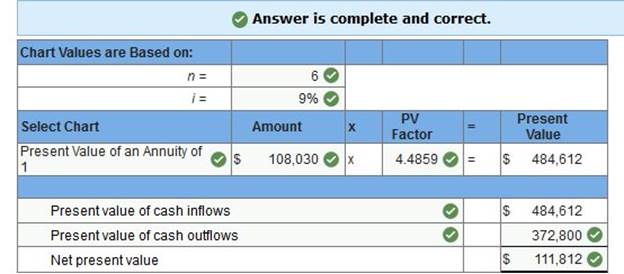

Exercise 11-9 Computing net present value LO P3 B2B Co. is considering the purchase of equipment that would allow the company to add a new product to its line. The equipment is expected to cost $372,800 with a 6-year life and no salvage value. It will be depreciated on a straight-line basis. The company expects to sell 149,120 units of the equipment’s product each year. The expected annual income related to this equipment follows.

If at least an 9% return on this investment must be earned, compute the net present value of this investment. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.)

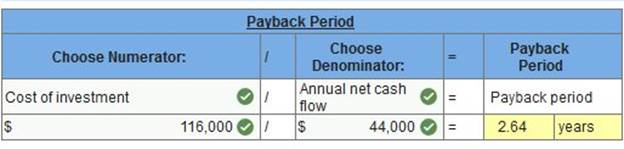

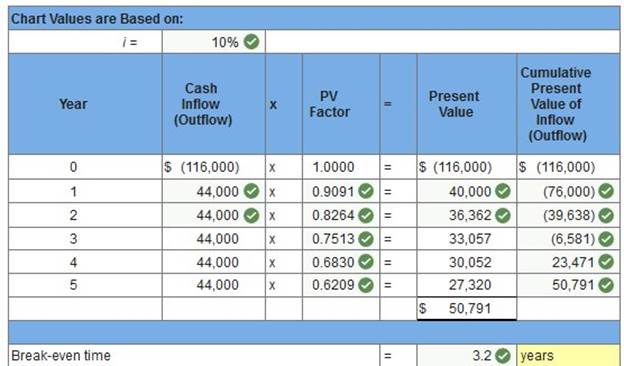

Exercise 11-16 Comparison of payback and BET LO P1, A1 Heels, a shoe manufacturer, is evaluating the costs and benefits of new equipment that would custom fit each pair of athletic shoes. The customer would have his or her foot scanned by digital computer equipment; this information would be used to cut the raw materials to provide the customer a perfect fit. The new equipment costs $116,000 and is expected to generate an additional $44,000 in cash flows for 5 years. A bank will make a $116,000 loan to the company at a 10% interest rate for this equipment’s purchase and compute the recovery time for both the payback period and break-even time. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.) Payback Period Compute the recovery time for the break-even time. (Cumulative net cash outflows must be entered with a minus sign. Round your Break-even time answer to 1 decimal place.)

Break even time Compute the recovery time for the break-even time. (Cumulative net cash outflows must be entered with a minus sign. Round your Break-even time answer to 1 decimal place.)

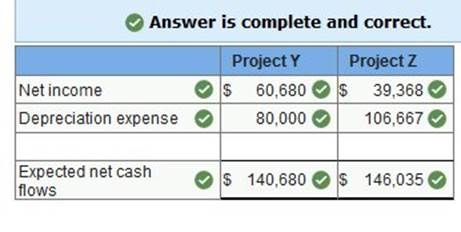

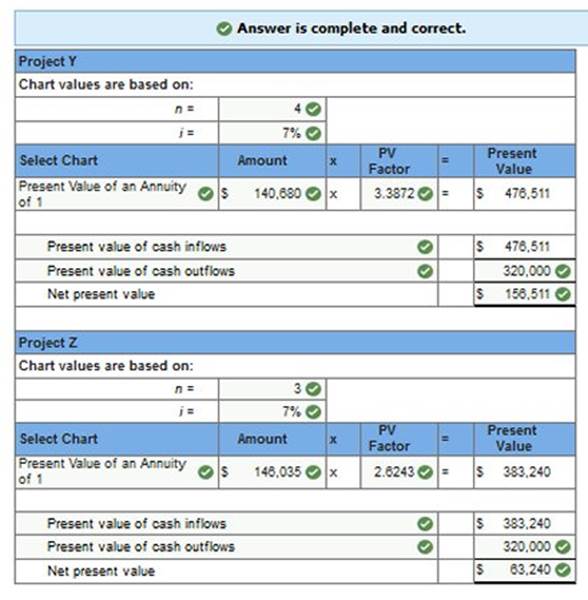

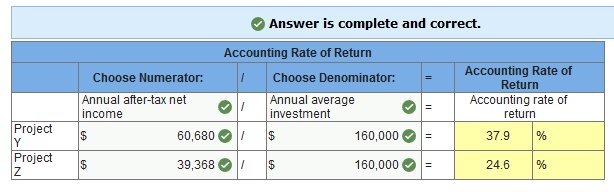

Required information Problem 11-2A Analysis and computation of payback period, accounting rate of return, and net present value LO P1, P2, P3 [The following information applies to the questions displayed below.] Most Company has an opportunity to invest in one of two new projects. Project Y requires a $320,000 investment for new machinery with a four-year life and no salvage value. Project Z requires a $320,000 investment for new machinery with a three-year life and no salvage value. The two projects yield the following predicted annual results. The company uses straight-line depreciation, and cash flows occur evenly throughout each year. (PV of $1, FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the tables provided.)

Required: 1. Compute each project’s annual expected net cash flows.

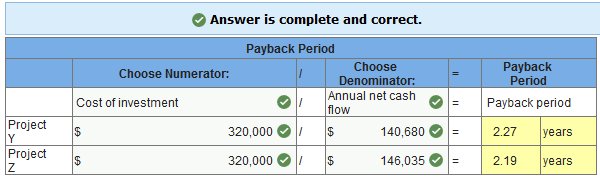

Problem 11-2A Part 2 2. Determine each project’s payback period.

Problem 11-2A Part 3 3. Compute each project’s accounting rate of return.

Exercise 25-12 Scrap or rework LO A1

value: 4.00 points Exercise 25-13 Decision to accept additional business or not LO A1

Exercise 25-14 Make or buy decision LO A1

Exercise 25-15 Sell or process decision LO A1

Dept. M Dept. N Dept. O Dept. P Dept. T Sales $ 42,500 $16,100 $ 34,500 $ 35,500 $ 14,200 Expenses Avoidable 4,500 13,100 13,700 7,000 19,900 Unavoidable 19,000 6,600 2,800 16,000 4,600 ________________________________________ ________________________________________ Total expenses 23,500 19,700 16,500 23,000 24,500 ________________________________________ ________________________________________ Net income (loss) $ 19,000 $ (3,600 ) $ 18,000 $ 12,500 $ (10,300 )

Exercise 25-16 Part 1

Exercise 25-16 Part 2

Exercise 25-16 Part 3

value: 3.00 points Exercise 25-17 Sales mix determination and analysis LO A1

Homework 1.1 1.2 2.1 2.2 3.1 3.2 4.1 4.2 5.1 5.2 6.1 6.2 7.1 7.2 8.1 8.2 9.1 9.2 10.1 10.2 11.1 11.2 12.1 12.2 13.1 13.2 14.1 14.2 15.1 15.2

Learnsmart 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 | Final Exam 1 2 Homework Help? |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |