|

Principals Of Managerial Accounting: Homework Chapter 10 Part 1

Exercise 10-15 Product

pricing using variable costs LO P1

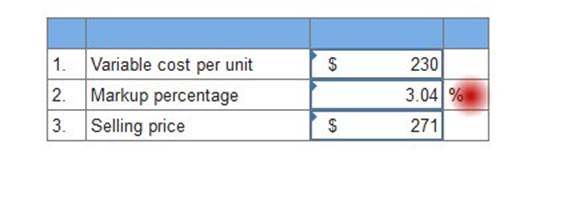

Rios Co. makes drones and

uses the variable cost approach in setting product prices. Its costs for producing

40,000 units follow.

The company targets a

profit of $320,000 on this product.

|

Variable

Costs per Unit

|

|

Fixed Costs

|

|

|

Direct materials

|

$

|

90

|

|

Overhead

|

$

|

690,000

|

|

|

Direct labor

|

|

60

|

|

Selling

|

|

325,000

|

|

|

Overhead

|

|

45

|

|

Administrative

|

|

305,000

|

|

|

Selling

|

|

35

|

|

|

|

|

|

|

|

1. Compute the variable cost per unit.

2. Compute the markup percentage on variable cost. (Round

percentage answer to 2 decimal places.)

3. Compute the product’s selling price using the variable cost method.

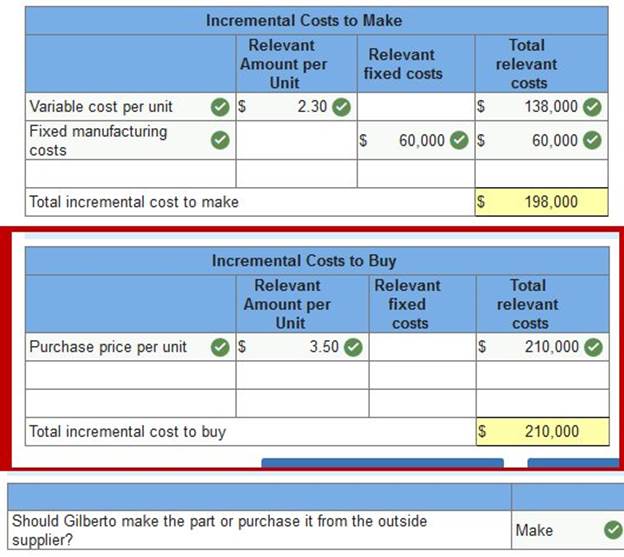

Exercise 10-4 Make or buy

decision LO A1

Gilberto Company currently

manufactures 60,000 units per year of one of its crucial parts.

Variable costs are $2.30

per unit, fixed costs related to making this part are $60,000 per year,

and allocated fixed costs

are $45,000 per year. Allocated fixed costs are unavoidable whether

the company makes or buys

the part. Gilberto is considering buying the part from a supplier

for a quoted price of

$3.50 per unit guaranteed for a three-year period.

Calculate the total incremental cost of making 60,000 and buying 60,000 units.

Should the company

continue to manufacture the part, or should it buy the part from the outside

supplier?

Costs to Make

Costs to Buy

Outside Supplier

Calculate the total

incremental cost of making 60,000 units. (Round

cost per unit answer to 2 decimal places.)

Calculate the total

incremental cost of buying 60,000 units. (Round

cost per unit answer to 2 decimal places.)

Should the company

continue to manufacture the part, or should it buy the part from the outside

supplier?

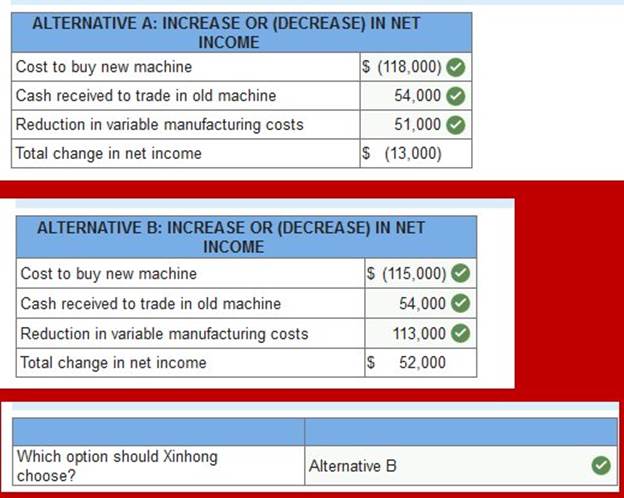

Exercise 10-12 Keep or

replace LO A1

Xinhong Company is

considering replacing one of its manufacturing machines.

The machine has a book

value of $44,000 and a remaining useful life of 5 years, at which time its

salvage value will be zero.

It has a current market

value of $54,000. Variable manufacturing costs are $33,200 per year for this

machine.

Information on two

alternative replacement machines follows.

|

|

Alternative

A

|

|

Alternative

B

|

|

Cost

|

$

|

118,000

|

|

|

$

|

115,000

|

|

|

Variable

manufacturing costs per year

|

|

23,000

|

|

|

|

10,600

|

|

|

|

Calculate the total change in net income if Alternative A, B is adopted. Should

Xinhong keep or replace its manufacturing machine?

If the machine should be

replaced, which alternative new machine should Xinhong purchase?

Alternative A

Alternative B

Xinhong Purchase

Calculate the total change

in net income if Alternative A is adopted. (Cash

outflows should be indicated by a minus sign.)

Calculate the total change

in net income if Alternative B is adopted. (Cash

outflows should be indicated by a minus sign.

Should Xinhong keep or

replace its manufacturing machine? If the machine should be replaced, which

alternative new machine should Xinhong purchase?

|

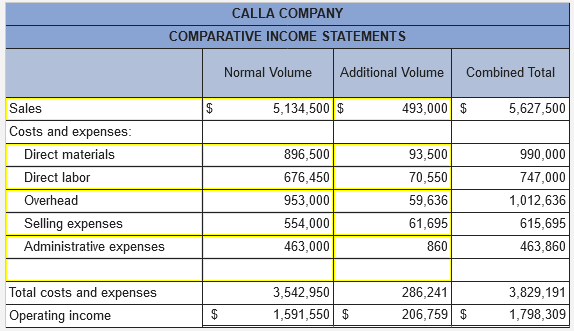

Calla Company produces

skateboards that sell for $63 per unit. The company currently has the

capacity to produce 90,000 skateboards per year, but is selling 81,500

skateboards per year. Annual costs for 81,500 skateboards follow.

|

|

|

|

|

Direct

materials

|

$

|

896,500

|

|

Direct

labor

|

|

676,450

|

|

Overhead

|

|

953,000

|

|

Selling

expenses

|

|

554,000

|

|

Administrative

expenses

|

|

463,000

|

|

|

|

|

Total costs

and expenses

|

$

|

3,542,950

|

|

|

|

|

|

|

A new retail store has

offered to buy 8,500 of its skateboards for $58 per unit. The store is in a

different market from Calla's regular customers and it would not affect

regular sales. A study of its costs in anticipation of this additional

business reveals the following:

|

·

Direct materials and direct labor

are 100% variable.

·

40 percent of overhead is fixed at

any production level from 81,500 units to 90,000 units; the remaining 60% of

annual

overhead costs are variable with respect to volume.

·

Selling expenses are 70% variable

with respect to number of units sold, and the other 30% of selling expenses are

fixed.

·

There will be an additional $2.5

per unit selling expense for this order.

·

Administrative expenses would

increase by a $860 fixed amount.

|

Required:

|

|

Prepare a three-column

comparative income statement that reports the following:

|

|

a.

|

Annual income without

the special order.

|

|

b.

|

Annual income from the

special order.

|

|

c.

|

Combined annual income

from normal business and the new business.

|

|

(Do not round

intermediate calculations and round your answers to the nearest whole

dollar.)

|

|

|

|

Farrow Co.

expects to sell 150,000 units of its product in the next period with the

following results.

|

|

|

|

|

|

|

Sales

(150,000 units)

|

|

$

|

2,250,000

|

|

|

Costs

and expenses

|

|

|

|

|

|

Direct

materials

|

|

|

300,000

|

|

|

Direct

labor

|

|

|

600,000

|

|

|

Overhead

|

|

|

150,000

|

|

|

Selling

expenses

|

|

|

225,000

|

|

|

Administrative

expenses

|

|

|

385,500

|

|

|

|

|

|

|

|

|

Total

costs and expenses

|

|

|

1,660,500

|

|

|

|

|

|

|

|

|

Net

income

|

|

$

|

589,500

|

|

|

|

|

|

|

|

|

|

|

The

company has an opportunity to sell 15,000 additional units at $12 per unit.

The additional sales would not affect its current expected sales. Direct

materials and labor costs per unit would be the same for the additional units

as they are for the regular units. However, the additional volume would

create the following incremental costs: (1) total overhead would increase by

15% and (2) administrative expenses would increase by $64,500.

|

Calculate

the combined total net income if the company accepts the offer to sell

additional units at the reduced price of $12 per unit.

|

|

|

|

|

Normal

Volume

|

Additional

Volume

|

Combined

Total

|

|

Sales

|

$2,250,000

|

$180,000

|

$2,430,000

|

|

Costs

and expenses:

|

|

|

|

|

Direct

materials

|

300,000

|

30,000

|

330,000

|

|

Direct

labor

|

600,000

|

60,000

|

660,000

|

|

Overhead

|

150,000

|

22,500

|

172,500

|

|

Selling

expenses

|

225,000

|

|

225,000

|

|

Administrative

expenses

|

385,500

|

64,500

|

450,000

|

|

Total

costs and expenses

|

1,660,500

|

177,000

|

1,837,500

|

|

Incremental

income (loss) from new business

|

$589,500

|

$3,000

|

$592,500

|

|

Should the

company accept or reject the offer?

|

The

company should accept the offer

|

A company

must decide between scrapping or reworking units that do not pass inspection.

The company has 22,000 defective units that cost $6 per unit to manufacture.

The units can be sold as is for $2.50 each, or they can be reworked for $4.50

each and then sold for the full price of $8.50 each. If the units are sold as

is, the company will be able to build 22,000 replacement units at a cost of

$6 each, and sell them at the full price of $8.50 each.

|

What is

the incremental income from selling the units as scrap and reworking and

selling the units? Should the company sell the units as scrap or rework

them? (Enter costs

and losses as negative values.)

|

|

|

|

|

Sale as

Scrap

|

Rework

|

|

Sales of

scrap units

|

$55,000

|

|

|

Sales of

reworked units

|

|

$187,000

|

|

Cost to

rework units

|

|

(99,000)

|

|

Opportunity

cost of not making new units

|

|

(55,000)

|

|

Incremental

income (loss)

|

$55,000

|

$33,000

|

|

|

The

company should:

|

sell as

is

|

|

|

Cobe

Company has already manufactured 28,000 units of Product A at a cost of $28 per

unit. The 28,000 units can be sold at this stage for $700,000. Alternatively,

the units can be further processed at a $420,000 total additional cost and be

converted into 5,600 units of Product B and 11,200 units of Product C. Per

unit selling price for Product B is $105 and for Product C is $70.

|

|

1.

|

Prepare an

analysis that shows whether the 28,000 units of Product A should be processed

further or not.

|

|

|

|

|

Sell as

is

|

Process

Further

|

|

|

Sales

|

$700,000

|

$1,372,000

|

|

|

Relevant

costs

|

|

|

|

Costs

to process further

|

|

420,000

|

|

Total

relevant costs

|

|

420,000

|

|

Income

(loss)

|

$700,000

|

$952,000

|

|

|

Incremental

net income (or loss) if processed further

|

$252,000

|

Incremental

income

|

|

|

The

company should

|

process

further

|

|

-----------------------------------------------------------------------------------------------------------------------------------

5.

|

Xinhong

Company is considering replacing one of its manufacturing machines. The

machine has a book value of $45,000 and a remaining useful life of 5 years,

at which time its salvage value will be zero. It has a current market value

of $52,000. Variable manufacturing costs are $36,000 per year for this

machine. Information on two alternative replacement machines follows.

|

|

Alternative

A

|

Alternative

B

|

|

Cost

|

$

|

115,000

|

|

$

|

125,000

|

|

|

Variable

manufacturing costs per year

|

|

19,000

|

|

|

15,000

|

|

|

|

|

Calculate

the total change in net income if Alternative A is adopted.

(Cash outflows

should be indicated by a minus sign.)

|

|

|

|

|

ALTERNATIVE

A: INCREASE OR (DECREASE) IN NET INCOME

|

|

Cost to

buy new machine

|

$(115,000)

|

|

Cash

received to trade in old machine

|

52,000

|

|

Reduction

in variable manufacturing costs

|

85,000

|

|

Total

change in net income

|

$22,000

|

|

Calculate the total change in net income if

Alternative B is adopted.

(Cash outflows

should be indicated by a minus sign.)

|

|

|

|

ALTERNATIVE

B: INCREASE OR (DECREASE) IN NET INCOME

|

|

Cost to

buy new machine

|

$(125,000)

|

|

Cash

received to trade in old machine

|

52,000

|

|

Reduction

in variable manufacturing costs

|

105,000

|

|

Total

change in net income

|

$32,000

|

|

|

Should

Xinhong keep or replace its manufacturing machine? If the machine should be

replaced, which alternative new machine should Xinhong purchase?

|

Alternative

B

[The

following information applies to the questions displayed below.]

|

Suresh Co.

expects its five departments to yield the following income for next year.

|

|

Dept. M

|

Dept. N

|

Dept. O

|

Dept. P

|

Dept. T

|

Total

|

|

|

Sales

|

|

$

|

63,000

|

|

|

$

|

35,000

|

|

|

|

$

|

56,000

|

|

|

$

|

42,000

|

|

|

|

$

|

28,000

|

|

|

$

|

224,000

|

|

|

Expenses

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Avoidable

|

|

|

9,800

|

|

|

|

36,400

|

|

|

|

|

22,400

|

|

|

|

14,000

|

|

|

|

|

37,800

|

|

|

$

|

120,400

|

|

|

Unavoidable

|

|

|

51,800

|

|

|

|

12,600

|

|

|

|

|

4,200

|

|

|

|

29,400

|

|

|

|

|

9,800

|

|

|

$

|

107,800

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

expenses

|

|

|

61,600

|

|

|

|

49,000

|

|

|

|

|

26,600

|

|

|

|

43,400

|

|

|

|

|

47,600

|

|

|

|

228,200

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net

income (loss)

|

|

$

|

1,400

|

|

|

$

|

(14,000

|

)

|

|

|

$

|

29,400

|

|

|

$

|

(1,400

|

)

|

|

|

$

|

(19,600

|

)

|

|

$

|

(4,200

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recompute

and prepare the departmental income statements (including a combined total

column) for the company under each of the following separate scenarios.

|

|

(1)

|

Management

eliminates departments with expected net losses.

|

|

|

|

|

DEPARTMENTS

WITH EXPECTED NET LOSSES ELIMINATED

|

|

Dept. M

|

Dept. N

|

Dept. O

|

Dept. P

|

Dept. T

|

Total

|

|

Sales

|

$63,000

|

|

$56,000

|

|

|

$119,000

|

|

Expenses:

|

|

|

|

|

|

0

|

|

Avoidable

|

9,800

|

|

22,400

|

|

|

32,200

|

|

Unavoidable

|

51,800

|

12,600

|

4,200

|

29,400

|

9,800

|

107,800

|

|

Total

expenses

|

61,600

|

12,600

|

26,600

|

29,400

|

9,800

|

140,000

|

|

Net

income (loss)

|

$1,400

|

$(12,600)

|

$29,400

|

$(29,400)

|

$(9,800)

|

$(21,000)

|

|

|

|

|

|

DEPARTMENTS

WITH LESS SALES THAN AVOIDABLE EXPENSES ELIMINATED

|

|

Dept. M

|

Dept. N

|

Dept. O

|

Dept. P

|

Dept. T

|

Total

|

|

Sales

|

$63,000

|

|

$56,000

|

$42,000

|

|

$161,000

|

|

Expenses:

|

|

|

|

|

|

|

|

Avoidable

|

9,800

|

|

22,400

|

14,000

|

|

46,200

|

|

Unavoidable

|

51,800

|

12,600

|

4,200

|

29,400

|

9,800

|

107,800

|

|

Total

expenses

|

61,600

|

12,600

|

26,600

|

43,400

|

9,800

|

154,000

|

|

Net

income (loss)

|

$1,400

|

$(12,600)

|

$29,400

|

$(1,400)

|

$(9,800)

|

$7,000

|

|

Childress Company produces three products, K1, S5,

and G9. Each product uses the same type of direct material.

K1 uses 4

pounds of the material, S5 uses 3 pounds of the material, and G9 uses 6 pounds

of the material.

Demand for

all products is strong, but only 50,000 pounds of material are available.

Information

about the selling price per unit and variable cost per unit of each product

follows.

|

K1

|

S5

|

G9

|

|

Selling

price

|

$

|

160

|

$

|

112

|

$

|

210

|

|

Variable

costs

|

|

96

|

|

85

|

|

144

|

|

|

|

1.

|

Calculate

the contribution margin per pound for each of the three products.

|

|

|

|

|

Contribution

margin per pound

|

|

Product

K1

|

Product

S5

|

Product

G9

|

|

Contribution

margin per unit

|

$64.00

|

$27.00

|

$66.00

|

|

Pounds

per unit

|

4

|

3

|

6

|

|

Contribution

margin per pound

|

$16.00

|

$9.00

|

$11.00

|

|

|

Order in

which products should be produced and filled:

|

First

|

Third

|

Second

|

|

9.

|

Edgerron

Company is able to produce two products, G and B, with the same machine in

its factory. The following information is available.

|

|

Product G

|

Product B

|

|

Selling

price per unit

|

|

|

$

|

120

|

|

|

|

|

$

|

160

|

|

|

|

Variable

costs per unit

|

|

|

|

40

|

|

|

|

|

|

90

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contribution

margin per unit

|

|

|

$

|

80

|

|

|

|

|

$

|

70

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Machine

hours to produce 1 unit

|

|

0.4

|

hours

|

|

|

|

1.0

|

hours

|

|

|

|

Maximum

unit sales per month

|

|

600

|

units

|

|

|

|

200

|

units

|

|

|

|

|

|

The

company presently operates the machine for a single eight-hour shift for 22

working days each month. Management is thinking about operating the machine

for two shifts, which will increase its productivity by another eight hours

per day for 22 days per month. This change would require $15,000 additional

fixed costs per month.

(Round hours

per unit answers to 1 decimal place. Enter operating losses, if any, as

negative values.)

|

|

|

|

|

1.

Determine the contribution margin per machine hour that each product

generates.

|

|

Product

G

|

Product

B

|

|

|

Contribution

margin per unit

|

$80.00

|

$70.00

|

|

|

Machine

hours per unit

|

0.4

|

1.0

|

|

Contribution

margin per machine hour

|

$200.00

|

$70.00

|

|

Product

G

|

Product

B

|

Total

|

|

Maximum

number of units to be sold

|

600

|

200

|

|

|

Hours

required to produce maximum units

|

240

|

200

|

440

|

|

|

2. How

many units of Product G and Product B should the company produce if it

continues to operate with only one shift?

How much

total contribution margin does this mix produce each month?

|

|

Product

G

|

Product

B

|

Total

|

|

Hours

dedicated to the production of each product

|

176

|

|

176

|

|

Units

produced for most profitable sales mix

|

440

|

|

|

|

Contribution

margin per unit

|

$80.00

|

|

|

Total

contribution margin - one shift

|

$35,200

|

|

$35,200

|

|

|

3. If

the company adds another shift, how many units of Product G and Product B

should it produce?

How much

total contribution margin would this mix produce each month?

|

|

Product

G

|

Product

B

|

Total

|

|

Hours

dedicated to the production of each product

|

240

|

112

|

352

|

|

Units

produced for most profitable sales mix

|

600

|

112

|

|

|

Contribution

margin per unit

|

$80.00

|

$70.00

|

|

Total

contribution margin - two shifts

|

$48,000

|

$7,840

|

$55,840

|

|

Total

contribution margin - one shift

|

|

|

35,200

|

|

Change

in contribution margin

|

|

|

20,640

|

|

Change

in fixed costs

|

|

|

15,000

|

|

Change

in operating income(loss)

|

|

|

$5,640

|

|

Should

the company add another shift?

|

Yes

|

|

|

|

|

4.

Suppose that the company determines that it can increase Product G’s

maximum sales to 700 units per

month

by spending $12,000 per month in marketing efforts. Should the company

pursue this strategy and the double shift?

|

|

Product

G

|

Product

B

|

Total

|

|

Hours

dedicated to the production of each product

|

280

|

72

|

352

|

|

Units

produced for most profitable sales mix

|

700

|

72

|

|

|

Contribution

margin per unit

|

$80.00

|

$70.00

|

|

Total

contribution margin - two shifts and marketing campaign

|

$56,000

|

$5,040

|

$61,040

|

|

Contribution

margin - two shifts without marketing campaign

|

|

|

55,840

|

|

Change

in contribution margin

|

|

|

5,200

|

|

Additional

marketing costs

|

|

|

12,000

|

|

Change

in fixed costs

|

|

|

15,000

|

|

Change

in operating income(loss)

|

|

|

$(21,800)

|

|

Should

the company pursue the marketing campaign?

|

No

|

|

|

|

Another name for relevant cost is unavoidable

cost.

False

An opportunity cost is the

potential benefit lost by taking a specific action when two or more alternative

choices are available.

True

An opportunity cost:

Is the potential benefit lost by choosing a specific alternative course of

action among two or more.

Elliot Company can sell

all of its products A and Z that it can produce, but it has limited production

capacity.

It can produce 8 units of

A per hour or 10 units of Z per hour, and it has 20,000 production hours

available.

Contribution margin per

unit is $12 for A and $10 for Z. What is the most profitable sales mix for

Elliot Company?

0 units of A and 200,000 units of Z.

Bannister Co. is thinking about having one of its products manufactured by a

subcontractor.

Currently, the cost of manufacturing 1,000 units follows:

|

Direct material

|

$45,000

|

|

Direct labor

|

30,000

|

|

Factory overhead (30% is

variable)

|

98,000

|

If Bannister can buy 1,000

units from a subcontractor for $100,000, it should:

Buy the product because the total incremental costs of manufacturing are

greater than $100,000.

Additional costs incurred if a company pursues a certain course of action are

sunk costs.

False

A cost that requires a future outlay of cash, and is relevant for current and

future decision making, is a(n):

Out-of-pocket cost.

If accepting additional business would cause existing sales to decline, the

offer should always be declined.

False

A cost that cannot be avoided or changed because it arises from a past

decision, and is irrelevant to future decisions, is called a(n):

Sunk cost.

Costs already incurred in manufacturing the units of a product that do not meet

quality standards are relevant costs in a scrap or rework decision.

False

The Mad Hatter Company owns a machine that

manufactures two types of chimney caps.

Production time is .20

hours for cap A and .40 hours for cap B. The machine's capacity is 2,000 hours

per year.

Both products are sold to

a single customer who has agreed to buy all of the company's output up to a

maximum

of 1,000 units of cap A

and 6,000 units of cap B. Selling prices and variable costs per unit are shown

below.

Based on this information,

what is the Mad Hatter's most profitable sales mix?

|

Cap A

|

Cap B

|

|

Selling price per unit

|

$80

|

$60

|

|

Variable costs per unit

|

53

|

42

|

1,000 units of cap A

and 4,500 units of cap B.

Part of the decision to accept additional business should be based on a

comparison of the incremental (differential)

costs of the added

production with the additional revenues to be received.

True

Product A requires 5 machine hours per unit to be produced, Product B requires

only 3 machine hours per unit, and

the company's productive

capacity is limited to 240,000 machine hours. Product A sells for $16 per unit

and has variable

costs of $6 per unit.

Product B sells for $12 per unit and has variable costs of $5 per unit.

Assuming the company can

sell as many units of either product as it produces, the company should:

Produce only Product B.

If a company has the capacity to produce either 10,000 units of Product A or

10,000 units of Product B;

assuming fixed costs are

the same, production restrictions are the same for both products, and the

markets for both

products are unlimited;

the company should commit 100% of its capacity to the product that has the

higher contribution margin.

True

Benjamin Company had the following results of operations for the past year:

|

Sales (16,000 units at

$10)

|

|

$160,000

|

|

Direct materials and

direct labor

|

$96,000

|

|

|

Overhead (20% variable)

|

16,000

|

|

|

Selling and

administrative expenses (all fixed)

|

32,000

|

(144,000)

|

|

Operating income

|

|

$16,000

|

A foreign company (whose

sales will not affect Benjamin's market) offers to buy 4,000 units at $7.50 per

unit.

In addition to variable

manufacturing costs, selling these units would increase fixed overhead by $600

and selling

and administrative costs

by $300. If Benjamin accepts the offer, its profits will:

Increase by $4,300.

Additional power for operating machines, extra supplies, and added cleanup

costs are examples of incremental overhead costs.

True

Chang Industries has 2,000 defective units of product that have already cost

$14 each to produce.

A salvage company will

purchase the defective units as they are for $5 each. Chang's production

manager reports that the defects

can be corrected for $6

per unit, enabling them to be sold at their regular market price of $21.

The incremental income or

loss on reworking the units is:

$20,000 income.

To determine a product selling price based on the total cost method, management

should include:

Total production and nonproduction costs plus a markup.

Markson Company had the following results of operations for the past year:

|

Sales (8,000 units at

$20)

|

|

$160,000

|

|

Variable manufacturing

costs

|

$86,000

|

|

|

Fixed manufacturing

costs

|

15,000

|

|

|

Variable selling and

administrative expenses

|

12,000

|

|

|

Fixed selling and

administrative expenses

|

20,000

|

(133,000)

|

|

Operating income

|

|

$27,000

|

A foreign company whose

sales will not affect Markson's market offers to buy 2,000 units at $14 per

unit.

In addition to variable

manufacturing costs, selling these units would increase fixed overhead by

$1,600 for the purchase of special tools.

If Markson accepts this

additional business, its profits will:

Increase by $1,900.

Beta Inc. can produce a unit of Zed for the following costs:

|

Direct material

|

$10

|

|

Direct labor

|

20

|

|

Overhead

|

50

|

|

Total costs per unit

|

$80

|

An outside supplier offers

to provide Beta with all the Zed units it needs at $58 per unit. If Beta buys

from the supplier,

it will still incur 40% of

its overhead. Beta should:

Buy Zed since the relevant cost to make it is $60.

Bluebird Mfg. has received a special one-time order for 15,000 bird feeders at

$3 per unit. Bluebird currently produces and

sells 75,000 units at

$7.00 each. This level represents 80% of its capacity. Production costs for

these units are $3.50 per unit,

which includes $2.25

variable cost and $1.25 fixed cost. If Bluebird accepts this additional

business, the effect on net income will be:

$11,250 increase.

|

Gilberto Company

currently manufactures 65,000 units per year of one of its crucial parts.

Variable costs are $1.95 per unit, fixed costs related to making this part

are $75,000 per year, and allocated fixed costs are $62,000 per year.

Allocated fixed costs are unavoidable whether the company makes or buys the

part. Gilberto is considering buying the part from a supplier for a quoted

price of $3.25 per unit guaranteed for a three-year period.

|

Calculate the total

incremental cost of making 65,000 units. (Round cost per

unit answer to 2 decimal places.)

|

|

|

|

|

Incremental

Costs to Make

|

|

Relevant

Amount per Unit

|

Relevant

Fixed Costs

|

Total

Relevant Costs

|

|

Variable cost per unit

|

$1.95

|

|

$126,750

|

|

Fixed manufacturing

costs

|

|

$75,000

|

$75,000

|

|

|

|

|

|

Total incremental cost

to make

|

$201,750

|

|

Calculate the total

incremental cost of buying 65,000 units. (Round cost per

unit answer to 2 decimal places.)

|

|

|

|

|

Incremental

Costs to Buy

|

|

Relevant

Amount per Unit

|

Relevant

Fixed Costs

|

Total

Relevant Costs

|

|

Purchase price per

unit

|

$3.25

|

|

$211,250

|

|

|

|

|

|

|

|

|

|

Total incremental cost

to buy

|

$211,250

|

|

Should the company continue to manufacture the part, or should it buy the part

from the outside supplier?

Make

|

Haver Company currently

produces component RX5 for its sole product. The current cost per unit to

manufacture the required 52,000 units of RX5 follows.

|

|

|

|

|

Direct

materials

|

$

|

5.00

|

|

|

Direct

labor

|

|

9.00

|

|

|

Overhead

|

|

10.00

|

|

|

|

|

|

|

Total costs

per unit

|

$

|

24.00

|

|

|

|

|

|

|

|

Direct materials and

direct labor are 100% variable. Overhead is 70% fixed. An outside supplier

has offered to supply the 52,000 units of RX5 for $20.00 per unit.

|

|

1.

|

Calculate the per unit

incremental costs of making and buying component RX5.

|

|

|

|

|

|

|

Total

incremental costs of:

|

Making the

units

|

Buying the

units

|

|

Total direct materials

|

$260,000

|

|

|

Total direct labor

|

468,000

|

|

|

Variable overhead

costs

|

156,000

|

|

|

Cost to buy the units

|

|

1,040,000

|

|

|

|

|

Total costs

|

$884,000

|

$1,040,000

|

|

Should the company

continue to manufacture the part, or should it buy the part from the

outside supplier?

|

Make the

units

|

|

-----------------------------------------------------------------------------------------------------------------------------------

3.

Harold Manufacturing

produces denim clothing. This year, it produced 5,110 denim jackets at a

manufacturing cost of $41.00 each. These jackets were damaged in the

warehouse during storage. Management investigated the matter and identified

three alternatives for these jackets.

|

|

1.

|

Jackets can be sold to a

second-hand clothing shop for $7.00 each.

|

|

2.

|

Jackets can be

disassembled at a cost of $31,900 and sold to a recycler for $11.00 each.

|

|

3.

|

Jackets can be reworked

and turned into good jackets. However, with the damage, management estimates

it will be able to assemble the good parts of the 5,110 jackets into only

2,920 jackets. The remaining pieces of fabric will be discarded. The cost of

reworking the jackets will be $101,500, but the jackets can then be sold for

their regular price of $44.00 each.

|

|

Required:

|

|

|

1.

|

Calculate the

incremental income.

|

|

|

|

|

|

Alternative

1 Sell as is

|

Alternative

2 Disassemble and sell to a recycler

|

Alternative

3 Rework and turn into good jackets

|

|

Incremental revenue

|

$35,770

|

$56,210

|

$128,480

|

|

Incremental costs

|

0

|

31,900

|

101,500

|

|

Incremental income

|

$35,770

|

$24,310

|

$26,980

|

|

|

The company should

choose:

|

Alternative

1

|

|

|

|

|

-----------------------------------------------------------------------------------------------------------------------------------

4.

|

Edgerron Company is able

to produce two products, G and B, with the same machine in its factory. The

following information is available.

|

|

Product G

|

Product B

|

|

Selling

price per unit

|

|

|

$

|

230

|

|

|

|

|

$

|

260

|

|

|

|

Variable

costs per unit

|

|

|

|

100

|

|

|

|

|

|

156

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contribution

margin per unit

|

|

|

$

|

130

|

|

|

|

|

$

|

104

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Machine

hours to produce 1 unit

|

|

0.4

|

hours

|

|

|

|

1

|

hours

|

|

|

|

Maximum unit

sales per month

|

|

650

|

units

|

|

|

|

250

|

units

|

|

|

|

|

|

|

|

|

|

|

The company presently

operates the machine for a single eight-hour shift for 22 working days each

month. Management is thinking about operating the machine for two shifts,

which will increase its productivity by another eight hours per day for 22

days per month. This change would require $13,000 additional fixed costs per

month. =

(Round hours per unit

answers to 1 decimal place.)

|

|

Elegant

Decor Company’s management is trying to decide whether to eliminate

Department 200, which has produced losses or low profits for several years.

The company’s 2013 departmental income statement shows the following.

|

|

ELEGANT

DECOR COMPANY

Departmental Income Statements

For Year Ended December 31, 2013

|

|

Dept. 100

|

Dept. 200

|

Combined

|

|

Sales

|

|

$

|

438,000

|

|

|

|

$

|

309,539

|

|

|

|

$

|

747,539

|

|

|

Cost

of goods sold

|

|

|

265,000

|

|

|

|

|

214,000

|

|

|

|

|

479,000

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross

profit

|

|

|

173,000

|

|

|

|

|

95,539

|

|

|

|

|

268,539

|

|

|

Operating

expenses

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct

expenses

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Advertising

|

|

|

15,000

|

|

|

|

|

12,000

|

|

|

|

|

27,000

|

|

|

Store

supplies used

|

|

|

6,000

|

|

|

|

|

5,500

|

|

|

|

|

11,500

|

|

|

Depreciation

Store equip.

|

|

|

5,000

|

|

|

|

|

3,800

|

|

|

|

|

8,800

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

direct expenses

|

|

|

26,000

|

|

|

|

|

21,300

|

|

|

|

|

47,300

|

|

|

Allocated

expenses

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales

salaries

|

|

|

78,000

|

|

|

|

|

46,800

|

|

|

|

|

124,800

|

|

|

Rent

expense

|

|

|

9,440

|

|

|

|

|

4,740

|

|

|

|

|

14,180

|

|

|

Bad

debts expense

|

|

|

10,100

|

|

|

|

|

8,100

|

|

|

|

|

18,200

|

|

|

Office

salary

|

|

|

18,720

|

|

|

|

|

12,480

|

|

|

|

|

31,200

|

|

|

Insurance

expense

|

|

|

1,900

|

|

|

|

|

1,100

|

|

|

|

|

3,000

|

|

|

Misc.

office expenses

|

|

|

2,700

|

|

|

|

|

2,100

|

|

|

|

|

4,800

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

allocated expenses

|

|

|

120,860

|

|

|

|

|

75,320

|

|

|

|

|

196,180

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

expenses

|

|

|

146,860

|

|

|

|

|

96,620

|

|

|

|

|

243,480

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net

income (loss)

|

|

$

|

26,140

|

|

|

|

$

|

(1,081)

|

|

|

|

$

|

25,059

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In analyzing whether to eliminate Department 200, management considers

the following:

a.The company has one office worker who earns $600 per week, or

$31,200 per year, and four sales clerks who each earn $600 per week,

or $31,200 per year for each salesclerk.

b. The full salaries of two salesclerks are charged to Department 100.

The full salary of one salesclerk is charged to Department 200.

The salary of the fourth clerk, who works half-time in both

departments, is divided evenly between the two departments.

c. Eliminating Department 200 would avoid the sales salaries and the

office salary currently allocated to it. However, management prefers

another plan. Two salesclerks have indicated that they will be

quitting soon. Management believes that their work can be done by the other

two clerks if the one office worker works in sales half-time.

Eliminating Department 200 will allow this shift of duties. If this change is

implemented, half the office worker’s salary would be reported as

sales salaries and half would be reported as office salary.

d. The store building is rented under a long-term lease that cannot be

changed. Therefore, Department 100 will use the space and

equipment currently used by Department 200.

e. Closing Department 200 will eliminate its expenses for advertising,

bad debts, and store supplies; 68% of the insurance expense

allocated to it to cover its merchandise inventory; and 21% of the

miscellaneous office expenses presently allocated to it.

Required:

Complete the three-column report that lists items and amounts for (a)

the company’s total expenses (including cost of goods sold)

—in column 1, (b) the expenses that would be eliminated by closing

Department 200

—in column 2, and (c) the expenses that will continue

—in column 3. The statement should reflect the reassignment of the

office worker to one-half time as salesclerk.

|

|

ELEGANT

DECOR COMPANY

|

|

Analysis

of Expenses under Elimination of Department 200

|

|

Total

Expenses

|

Eliminated

Expenses

|

Continuing

Expenses

|

|

Cost of goods sold

|

$479,000

|

$214,000

|

$265,000

|

|

Direct expenses

|

|

|

|

|

Advertising

|

27,000

|

12,000

|

15,000

|

|

Store supplies used

|

11,500

|

5,500

|

6,000

|

|

Depreciation—Store

equipment

|

8,800

|

|

8,800

|

|

Allocated expenses

|

|

|

|

|

Sales salaries

|

124,800

|

46,800

|

78,000

|

|

Rent expense

|

14,180

|

|

14,180

|

|

Bad debts expense

|

18,200

|

8,100

|

10,100

|

|

Office salary

|

31,200

|

15,600

|

15,600

|

|

Insurance expense

|

3,000

|

748

|

2,252

|

|

Miscellaneous office

expenses

|

4,800

|

441

|

4,359

|

|

Total expenses

|

$722,480

|

$303,189

|

$419,291

|

|

|

Factor Company is

planning to add a new product to its line. To manufacture this product, the

company needs to buy a new machine at a $495,000 cost with an expected

four-year life and a $26,000 salvage value. All sales are for cash, and all

costs are out of pocket except for depreciation on the new machine.

Additional information includes the following.

(PV of $1, FV of $1, PVA of $1, and FVA of $1)

(Use appropriate

factor(s) from the tables provided.)

|

|

|

|

|

|

|

Expected

annual sales of new product

|

$

|

1,870,000

|

|

|

Expected

annual costs of new product

|

|

|

|

|

Direct

materials

|

|

495,000

|

|

|

Direct

labor

|

|

675,000

|

|

|

Overhead

excluding straight-line depreciation on new machine

|

|

339,000

|

|

|

Selling

and administrative expenses

|

|

163,000

|

|

|

Income

taxes

|

|

30

|

%

|

|

Required:

|

|

1.

|

Compute straight-line

depreciation for each year of this new machine’s life.

|

|

|

|

|

Straight-line

depreciation

|

$117,250

|

|

$495,000

− $26,000 / 4 = $117,250

|

2.

|

Determine expected net

income and net cash flow for each year of this machine’s life.

|

|

|

|

|

Expected

net income

|

|

Revenues

|

|

|

|

Sales

|

$1,870,000

|

|

Expenses

|

|

|

|

Direct materials

|

$495,000

|

|

|

Direct labor

|

675,000

|

|

|

Overhead excluding straight-line

depreciation on new machine

|

339,000

|

|

|

Straight-line

depreciation on new machine

|

117,250

|

|

|

Selling and

administrative expenses

|

163,000

|

|

|

|

|

|

|

|

|

Total expenses

|

|

1,789,250

|

|

Income before taxes

|

|

80,750

|

|

Income tax expense

|

|

24,225

|

|

Net income

|

|

$56,525

|

|

Expected

net cash flow

|

|

|

Net income

|

|

$56,525

|

|

|

Straight-line

depreciation on new machine

|

|

117,250

|

|

|

Net cash flow

|

|

$173,775

|

|

|

|

3.

|

Compute this machine’s

payback period, assuming that cash flows occur evenly throughout each year.

|

|

|

|

|

Payback

period

|

|

Choose

Numerator:

|

/

|

Choose

Denominator:

|

=

|

Payback

period

|

|

Cost of investment

|

/

|

Annual net cash flow

|

=

|

Payback period

|

|

$495,000

|

/

|

$173,775

|

=

|

2.85

|

years

|

|

|

4.

|

Compute this machine’s

accounting rate of return, assuming that income is earned evenly throughout

each year.

|

|

|

Accounting

rate of return

|

|

Choose

Numerator:

|

/

|

Choose

Denominator:

|

=

|

Accounting

rate of return

|

|

Annual after-tax net

income

|

/

|

Annual average investment

|

=

|

Accounting rate of

return

|

|

$56,525

|

/

|

$260,500

|

=

|

21.70

|

%

|

|

5.

|

Compute the net

present value for this machine using a discount rate of 7% and assuming

that cash flows occur at each year-end. (Hint: Salvage value is a cash

inflow at the end of the asset’s life.)

|

|

|

|

|

Chart

values are based on:

|

|

|

|

|

|

|

n =

|

4

|

|

|

i =

|

7%

|

|

Cash

flow

|

Select

chart

|

Amount

|

x

|

Table

factor

|

=

|

Present

Value

|

|

Annual cash flow

|

Present Value of an

Annuity of 1

|

$173,775

|

x

|

3.3872

|

=

|

$588,611

|

|

Salvage value

|

Present Value of 1

|

$26,000

|

x

|

0.7629

|

=

|

19,835

|

|

Present value of

cash inflows

|

|

$608,446

|

|

Present value of

cash outflows

|

|

(495,000)

|

|

Net present value

|

|

$113,446

|

|

|

|

Sentinel Company is

considering an investment in technology to improve its operations. The

investment will require an initial outlay of $257,000 and will yield the

following expected cash flows. Management requires investments to have a

payback period of 3 years, and it requires a 9% return on investments. (PV of $1,FV of $1, PVA of $1, and FVA of $1) (Use appropriate factor(s) from the table

provided.)

|

|

Period

|

Cash Flow

|

|

1

|

$ 47,000

|

|

2

|

53,900

|

|

3

|

75,600

|

|

4

|

94,700

|

|

5

|

125,400

|

|

|

|

Required:

|

|

1.

|

Determine the payback

period for this investment.

(Enter

cash outflows with a minus sign. Round your answer to 1 decimal place.)

|

|

|

|

|

Year

|

Cash

inflow (outflow)

|

Cumulative

Net Cash Inflow (outflow)

|

|

|

|

0

|

$(257,000)

|

$(257,000)

|

|

|

1

|

47,000

|

(210,000)

|

|

2

|

53,900

|

(156,100)

|

|

3

|

75,600

|

(80,500)

|

|

4

|

94,700

|

14,200

|

|

5

|

125,400

|

139,600

|

|

$139,600

|

|

|

Calculate

the payback period:

|

|

Payback occurs between

year:

|

3

|

and year:

|

4

|

|

Calculate the portion

of the year:

|

|

Numerator for

partial year

|

$80,500

|

0.9

|

years

|

|

Denominator for

partial year

|

$94,700

|

|

|

|

|

Payback period =

|

3.9

|

years

|

|

|

2.

|

Determine the break-even

time for this investment. (Enter cash outflows with a minus

sign. Round your answer to 1 decimal place.)

|

|

|

|

|

Year

|

Cash

inflow (outflow)

|

Table

factor

|

Present

Value of Cash Flows

|

Cumulative

Present Value of Cash Flows

|

|

|

0

|

$(257,000)

|

1.0000

|

$(257,000)

|

$(257,000)

|

|

|

1

|

47,000

|

0.9174

|

$43,118

|

(213,882)

|

|

|

2

|

53,900

|

0.8417

|

$45,368

|

(168,514)

|

|

|

3

|

75,600

|

0.7722

|

$58,378

|

(110,136)

|

|

|

4

|

94,700

|

0.7084

|

$67,085

|

(43,051)

|

|

|

5

|

125,400

|

0.6499

|

$81,497

|

38,446

|

|

|

$139,600

|

|

|

|

|

|

Calculate

the break even time:

|

|

Break-even time occurs

between year:

|

4

|

and year:

|

5

|

|

|

Calculate the portion

of the year:

|

|

Numerator for

partial year

|

$43,051

|

0.5

|

years

|

|

|

Denominator for

partial year

|

$81,497

|

|

|

|

|

|

|

Break-even time =

|

4.5

|

years

|

|

|

|

3.

|

Determine the net

present value for this investment.

|

|

|

|

Net

present value

|

$38,446

|

|

|

Forten Company, a merchandiser,

recently completed its calendar-year 2013 operations. For the year, (1) all

sales are credit sales, (2) all credits to Accounts Receivable reflect cash

receipts from customers, (3) all purchases of inventory are on credit, (4)

all debits to Accounts Payable reflect cash payments for inventory, and (5)

Other Expenses are paid in advance and are initially debited to Prepaid

Expenses. The company’s balance sheets and income statement follow.

|

|

FORTEN

COMPANY

Comparative Balance Sheets

December 31, 2013 and 2012

|

|

2013

|

|

2012

|

|

Assets

|

|

|

|

|

|

|

Cash

|

$

|

50,404

|

|

$

|

68,000

|

|

Accounts

receivable

|

|

73,525

|

|

|

57,125

|

|

Merchandise

inventory

|

|

265,906

|

|

|

238,800

|

|

Prepaid

expenses

|

|

1,440

|

|

|

1,900

|

|

Equipment

|

|

154,300

|

|

|

112,000

|

|

Accum.

depreciation—Equipment

|

|

(45,400)

|

|

|

(52,000)

|

|

|

|

|

|

|

|

|

Total assets

|

$

|

500,175

|

|

$

|

425,825

|

|

|

|

|

|

|

|

|

Liabilities

and Equity

|

|

|

|

|

|

|

Accounts

payable

|

$

|

58,875

|

|

$

|

110,000

|

|

Short-term

notes payable

|

|

8,400

|

|

|

5,200

|

|

Long-term

notes payable

|

|

33,575

|

|

|

39,000

|

|

Common

stock, $5 par value

|

|

161,500

|

|

|

148,000

|

|

Paid-in

capital in excess of par, common stock

|

|

40,500

|

|

|

0

|

|

Retained

earnings

|

|

197,325

|

|

|

123,625

|

|

|

|

|

|

|

|

|

Total

liabilities and equity

|

$

|

500,175

|

|

$

|

425,825

|

|

|

|

|

|

|

|

|

|

|

FORTEN

COMPANY

Income Statement

For Year Ended December 31, 2013

|

|

Sales

|

|

|

|

$

|

615,000

|

|

Cost

of goods sold

|

|

|

|

|

298,000

|

|

|

|

|

|

|

|

|

Gross

profit

|

|

|

|

|

317,000

|

|

Operating

expenses

|

|

|

|

|

|

|

Depreciation

expense

|

$

|

19,200

|

|

|

|

|

Other

expenses

|

|

141,000

|

|

|

160,200

|

|

|

|

|

|

|

|

|

Other gains

(losses)

|

|

|

|

|

|

|

Loss

on sale of equipment

|

|

|

|

|

(4,300)

|

|

|

|

|

|

|

|

|

Income

before taxes

|

|

|

|

|

152,500

|

|

Income taxes

expense

|

|

|

|

|

29,000

|

|

|

|

|

|

|

|

|

Net income

|

|

|

|

$

|

123,500

|

|

|

|

|

|

|

|

|

|

|

Additional Information

on Year 2013 Transactions

|

|

a.

|

The loss on the cash

sale of equipment was $4,300 (details in b).

|

|

b.

|

Sold equipment costing

$44,800, with accumulated depreciation of $25,800, for $14,700 cash.

|

|

c.

|

Purchased equipment

costing $87,100 by paying $50,000 cash and signing a long-term note payable

for the balance.

|

|

d.

|

Borrowed $3,200 cash by

signing a short-term note payable.

|

|

e.

|

Paid $42,525 cash to

reduce the long-term notes payable.

|

|

f.

|

Issued 2,700 shares of

common stock for $20 cash per share.

|

|

g.

|

Declared and paid cash

dividends of $49,800.

|

|

Required:

|

|

1.

|

Prepare a complete

statement of cash flows; report its operating activities using the indirect

method. (Amounts to be deducted should be indicated with a minus sign.)

|

|

|

|

|

FORTEN

COMPANY

|

|

|

Statement

of Cash Flows

|

|

|

For Year

Ended December 31, 2013

|

|

|

Cash flows from

operating activities

|

|

|

|

|

Net Income

|

$123,500

|

|

|

|

Adjustments to

reconcile net income to net cash provided by operations:

|

|

|

Depreciation expense

|

19,200

|

|

|

|

Accounts receivable

increase

|

(16,400)

|

|

|

|

Inventory increase

|

(27,106)

|

|

|

|

Prepaid expense

decrease

|

460

|

|

|

|

Accounts payable

decrease

|

(51,125)

|

|

|

|

Loss on disposal of

equipment

|

4,300

|

|

|

|

|

|

|

|

Net cash provided by

operating activities

|

|

$52,829

|

|

|

Cash flows from

investing activities

|

|

|

|

Cash paid for

equipment

|

(50,000)

|

|

|

|

Cash received from

sale of equipment

|

14,700

|

|

|

|

|

|

|

|

Net cash used in

investing activities

|

|

(35,300)

|

|

|

Cash flows from

financing activities:

|

|

|

|

Cash borrowed on

short-term note

|

3,200

|

|

|

|

Cash paid on long-term

note

|

(42,525)

|

|

|

|

Cash received from issuing

stock

|

54,000

|

|

|

|

Cash paid for

dividends

|

(49,800)

|

|

|

|

|

|

|

|

Net cash used in

financing activities

|

|

(35,125)

|

|

|

Net increase

(decrease) in cash

|

$(17,596)

|

|

|

Cash balance at

beginning of year

|

68,000

|

|

|

Cash balance at end of

year

|

$50,404

|

|

|

Golden Corp., a

merchandiser, recently completed its 2013 operations. For the year,

(1) all sales are credit

sales,

(2) all credits to

Accounts Receivable reflect cash receipts from customers,

(3) all purchases of

inventory are on credit,

(4) all debits to Accounts

Payable reflect cash payments for inventory,

(5) Other Expenses are all

cash expenses, and

(6) any change in Income

Taxes Payable reflects the accrual and cash payment of taxes.

The company’s balance

sheets and income statement follow.

|

GOLDEN

CORPORATION

Comparative Balance Sheets

December 31, 2013 and 2012

|

|

2013

|

|

2012

|

|

Assets

|

|

|

|

|

|

|

|

Cash

|

$

|

229,000

|

|

$

|

159,000

|

|

|

Accounts

receivable

|

|

95,000

|

|

|

79,000

|

|

|

Merchandise

inventory

|

|

631,000

|

|

|

541,000

|

|

|

Equipment

|

|

373,000

|

|

|

329,000

|

|

|

Accum.

depreciation—Equipment

|

|

(183,000

|

)

|

|

(119,000

|

)

|

|

|

|

|

|

|

|

|

Total

assets

|

$

|

1,145,000

|

|

$

|

989,000

|

|

|

|

|

|

|

|

|

|

Liabilities

and Equity

|

|

|

|

|

|

|

|

Accounts

payable

|

$

|

97,000

|

|

$

|

86,000

|

|

|

Income

taxes payable

|

|

46,000

|

|

|

40,000

|

|

|

Common

stock, $2 par value

|

|

626,000

|

|

|

598,000

|

|

|

Paid-in

capital in excess of par value, common stock

|

|

217,000

|

|

|

175,000

|

|

|

Retained

earnings

|

|

159,000

|

|

|

90,000

|

|

|

|

|

|

|

|

|

|

Total

liabilities and equity

|

$

|

1,145,000

|

|

$

|

989,000

|

|

|

|

|

|

|

|

|

|

|

|

GOLDEN

CORPORATION

Income Statement

For Year Ended December 31, 2013

|

|

Sales

|

|

|

|

$

|

1,867,000

|

|

Cost

of goods sold

|

|

|

|

|

1,101,000

|

|

|

|

|

|

|

|

Gross

profit

|

|

|

|

|

766,000

|

|

Operating

expenses

|

|

|

|

|

|

|

Depreciation

expense

|

$

|

64,000

|

|

|

|

|

Other

expenses

|

|

509,000

|

|

|

573,000

|

|

|

|

|

|

|

|

Income

before taxes

|

|

|

|

|

193,000

|

|

Income

taxes expense

|

|

|

|

|

25,000

|

|

|

|

|

|

|

|

Net

income

|

|

|

|

$

|

168,000

|

|

|

|

|

|

|

|

|

Additional Information

on Year 2013 Transactions

|

|

a.

|

Purchased equipment for

$44,000 cash.

|

|

b.

|

Issued 14,000 shares of

common stock for $5 cash per share.

|

|

c.

|

Declared and paid

$99,000 in cash dividends.

|

|

Required:

|

|

Prepare a complete

statement of cash flows; report its cash inflows and cash outflows from

operating activities according to the indirect method. (Amounts to be deducted should be indicated with a

minus sign.)

|

|

|

|

|

GOLDEN

CORPORATION

|

|

Statement

of Cash Flows

|

|

For Year

Ended December 31, 2013

|

|

Cash flows from

operating activities

|

|

|

|

Net Income

|

$168,000

|

|

|

Adjustments to

reconcile net income to net cash provided by operations:

|

|

Accounts receivable

increase

|

(16,000)

|

|

|

Inventory increase

|

(90,000)

|

|

|

Accounts payable

increase

|

11,000

|

|

|

Income taxes payable

increase

|

6,000

|

|

|

Depreciation expense

|

64,000

|

|

|

|

|

|

Net cash provided by

operating activities

|

|

$143,000

|

|

Cash flows from

investing activities:

|

|

|

Cash paid for

equipment

|

(44,000)

|

|

|

|

|

|

Net cash used in

investing activities

|

|

(44,000)

|

|

Cash flows from

financing activities:

|

|

|

Cash received from

stock issuance

|

70,000

|

|

|

Cash paid for cash

dividends

|

(99,000)

|

|

|

|

|

|

Net cash used in

financing activities

|

|

(29,000)

|

|

Net increase

(decrease) in cash

|

$70,000

|

|

Cash balance at beginning

of year

|

159,000

|

|

Cash balance at end of

year

|

$229,000

|

|

|