|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Principles Of Fianance: Homework Chapter 11 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 | Final Exam 1 2

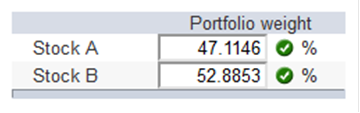

What are the portfolio

weights for a portfolio that has 185 shares of

Stock A that sell for $94 per share and 160 shares of Stock B that sell for $122 per share? (Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.1616.) Calculation of Weight of Stock A and Stock B

Explanation: The portfolio weight of an asset is the total investment in that asset divided by the total portfolio value. First, we will find the portfolio value, which is: Total value = 185($94) + 160($122) Total value = $36,910 The portfolio weight for each stock is: xA = 185($94) / $36,910 xA = .4711 or 47.11 xB = 160($122) / $36,910 xB = .5289 or 52.89 A portfolio is invested 27 percent in Stock G, 42 percent in Stock J, and 31 percent in Stock K. The expected returns on these stocks are 9.5 percent, 12 percent, and 17.4 percent, respectively. What is the portfolio’s expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

Expected return = [(27%*9.5) + (42%*12) + (31%*17.4)] which is equal to = 12.999 (13.00% Explanation: The portfolio's expected return is the sum of the weight (position) in each stock times the rate of return of each stock. The expected portfolio's return is: E(R) = .27(.095) + .42(.120) + .31(.174) E(R) = .1300, or 13.00% Consider the following information:

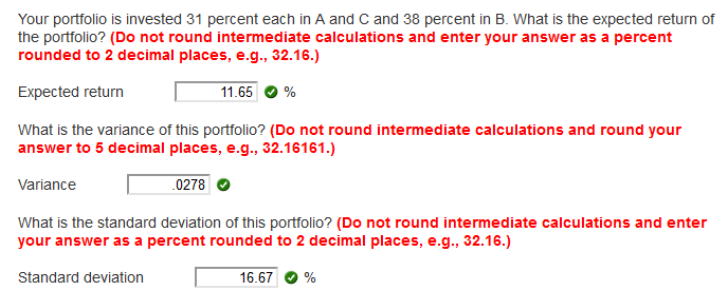

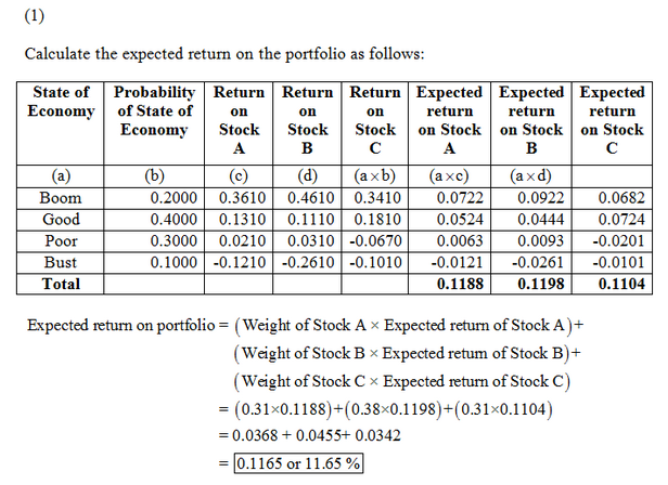

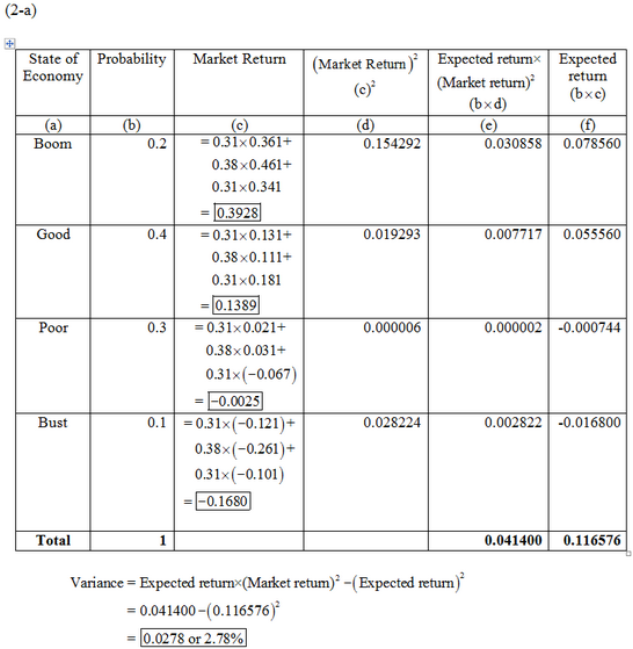

Your portfolio is invested 31 percent each in A and C and 38 percent in B. What is the expected return of the portfolio? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) What is the variance of this portfolio? (Do not round intermediate calculations and round your answer to 5 decimal places, e.g., 32.16161.) What is the standard deviation of this portfolio? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

Explanation

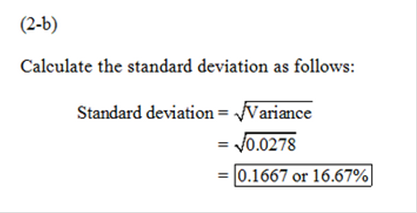

.041400 – (.116576) ^2 = .0278100362 (.0278)

Explanation: This portfolio does not have an equal weight in each asset. We first need to find the return of the portfolio in each state of the economy. To do this, we will multiply the return of each asset by its portfolio weight and then sum the products to get the portfolio return in each state of the economy. Doing so, we get:

And the expected return of the portfolio is: E(Rp) = .20(.3928) + .40(.1389) + .30(–.0025) + .10(–.1680) E(Rp) = .1166, or 11.66% To calculate the standard deviation, we first need to calculate the variance. To find the variance, we find the squared deviations from the expected return. We then multiply each possible squared deviation by its probability, and then sum. The result is the variance. So, the variance and standard deviation of the portfolio is: σp2 = .20(.3928 – .1166)2 + .40(.1389 – .1166)2 + .30(–.0025 – .1166)2 + .10(–.1680 – .1166)2 σp2 = .02781 σp = .027811/2 σp = .1668, or 16.68% A stock has a beta of 1.14, the expected return on the market is 10.8 percent, and the risk-free rate is 4.55 percent. What must the expected return on this stock be? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Expected return %

4.55 + 1.14 (10.8 - 4.55) = 11.68 % Explanation: The CAPM states the relationship between the risk of an asset and its expected return. The CAPM is: E(Ri) = Rf + [E(RM) – Rf] × βi Substituting the values we are given, we find: E(Ri) = .0455 + (.1080 – .0455)(1.14) E(Ri) = .1168, or 11.68% Consider the following information on a portfolio of three stocks:

a. If your portfolio is invested 40 percent each in A and B and 20 percent in C, what is the portfolio’s expected return, the variance, and the standard deviation? (Do not round intermediate calculations. Round your variance answer to 5 decimal places, e.g., 32.16161. Enter your other answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. If the expected T-bill rate is 4.5 percent, what is the expected risk premium on the portfolio? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) Expected risk premium

Explanation: a. We need to find the return of the portfolio in each state of the economy. To do this, we will multiply the return of each asset by its portfolio weight and then sum the products to get the portfolio return in each state of the economy. Doing so, we get:

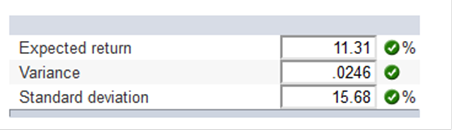

And the expected return of the portfolio is: E(Rp) = .12(.2460) + .55(.2180) + .33(–.1100) E(Rp) = .1131, or 11.31% To calculate the standard deviation, we first need to calculate the variance. To find the variance, we find the squared deviations from the expected return. We then multiply each possible squared deviation by its probability, and then sum. The result is the variance. So, the variance and standard deviation of the portfolio are: σ2p = .12(.2460 – .1131)2 + .55(.2180 – .1131)2 + .33(–.1100 – .1131)2 σ2p = .02460 σp = .024601/2 σp = .1568, or 15.68% b. The risk premium is the return of a risky asset, minus the risk-free rate. T-bills are often used as the risk-free rate, so: RPi = E(Rp) – Rf RPi = .1131 – .0450 RPi = .0681, or 6.81% What is the beta of the following portfolio?

.99 1.11 1.15 1.08 1.04

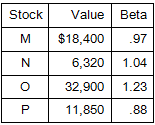

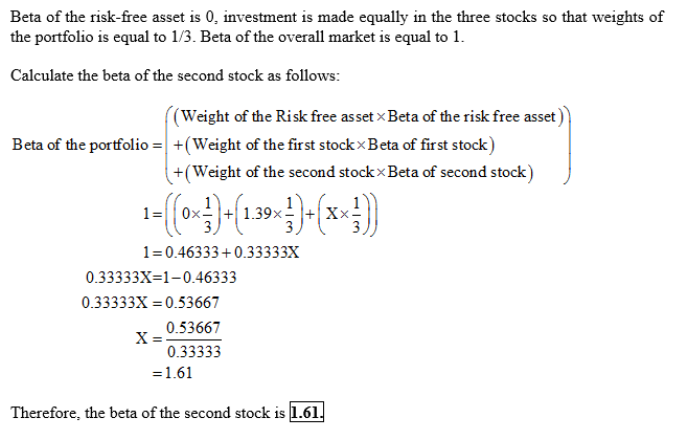

Now, Multiply each beta with its equivalent weight in the portfolio and sum it up. Portfolio beta = 0.97 x 26% + 1.04 x 9% + 1.23 x 47% + 0.88 x 17% = 1.084 A stock has a beta of 1.48 and an expected return of 17.3 percent. A risk-free asset currently earns 4.6 percent. If a portfolio of the two assets has a beta of .98, then the weight of the stock must be ___ and the risk-free weight must be___. .72; .28 .56; .44 .66; .34 .34; .66 .44; .56 Calculation of weight of the stock and weight of the risk free asset stock expected return = 17.3% stock beta value = 1.48 risk free asset beta value is = 0 risk free asset return = 4.6 portfolio beta is = 0.98 let taken weight of the stock is X so weight of the risk free asset is = 1-X portfolio beta = stock weight*beta+riskfree weight*beta 0.98 = X*1.48+(1-X)*0 0.98= 1.48X+0 1.48X= 0.98 X = 0.66 66% weight of the risk free asset is = 1-0.66 = 0.34 = 34% You would like to create a portfolio that is equally invested in a risk-free asset and two stocks. One stock has a beta of 1.39. What does the beta of the second stock have to be if you want the portfolio to be equally as risky as the overall market? 1.23 1.61 1.55 .97 .72

You own a $58,600 portfolio comprised of four stocks. The values of Stocks A, B, and C are $11,200, $17,400, and $20,400, respectively. What is the portfolio weight of Stock D? 12.58 percent 16.38 percent 10.33 percent 12.10 percent 15.39 percent

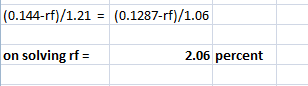

Stock A has an expected return of 14.4 percent and a beta of 1.21. Stock B has an expected return of 12.87 percent and a beta of 1.06. Both stocks have the same reward-to-risk ratio. What is the risk-free rate? 1.79 percent 2.28 percent 3.35 percent 2.06 percent 1.92 percent

A stock has a beta of 1.32 and an expected return of 12.8 percent. The risk-free rate is 3.6 percent. What is the slope of the security market line? 6.97 percent Slope = (.128 -.036)/1.32 = .0697, or 6.97 percent Stock J has a beta of 1.52 and an expected return of 15.76percent. Stock K has a beta of .98 and an expected return of 11.44 percent. What is the risk-free rate if these securities both plot on the security market line? 3.60 percent (.1576-Rf)/1.52 = (.1144 -Rf)/.98 Rf = .0360, or 3.60 percent Bama Entertainment has common stock with a beta of 1.22. The market risk premium is 8.1 percent and the risk-free rate is 3.9 percent. What is the expected return on this stock? 13.78 percent E(R) = .039 + 1.22(.081) = .1378, or 13.78 percent BJB stock has an expected return of 17.82 percent. The risk-free rate is 4.6 percent and the market risk premium is 8.2 percent. What is the stock's beta? 1.61 E(R) = .1782 = .046 + β(.082) β = 1.61 You own a stock that has an expected return of 15.72 percent and a beta of 1.33. The U.S. Treasury bill is yielding 3.82 percent and the inflation rate is 2.95 percent. What is the expected rate of return on the market? 12.77 percent E(R) = .1572 = .0382 + 1.33 (Rm -.0382) Rm = .1277, or 12.77 percent A stock has a beta of 1.10, an expected return of 12.11 percent, and lies on the security market line. A risk-free asset is yielding 3.2 percent. You want to create a portfolio valued at $12,000 consisting of Stock A and the risk-free security such that the portfolio beta is .80. What rate of return should you expect to earn on your portfolio? 9.68 percent E(R) = .1211= .032 + 1.10(MRP) MRP = .0810 E(RP) = .032 + .80(.0810) = .0968, or 9.68 percent You own a portfolio that has $2,200 invested in Stock A and $1,300 invested in Stock B. If the expected returns on these stocks are 11 percent and 17 percent, respectively, what is the expected return on the portfolio? 13.23 percent E(R) = [$2,200 / ($2,200 + 1,300)] ×.11 + [$1,300 / ($2,200 + 1,300)] ×.17 = .1323, or 13.23 percent You own a portfolio equally invested in a risk-free asset and two stocks. If one of the stocks has a beta of 1.86 and the total portfolio is equally as risky as the market, what must the beta be for the other stock in your portfolio? 1.14 βP = 1 = (1 / 3)(0) + (1 / 3) (1.86) + (1 / 3) (x) x = 1.14 A stock has a beta of 1.32, the expected return on the market is 12.72, and the risk-free rate is 4.05. What must the expected return on this stock be? 15.49 percent E(R) = .0405 + 1.32(.1272 -.0405) = .1549, or 15.49 percent A stock has an expected return of 14.3 percent, the risk-free rate is 3.9 percent, and the market risk premium is 7.8 percent. What must the beta of this stock be? 1.33 E(R) = .143 = .039 + β (.078) β = 1.33 A stock has a beta of 1.48 and an expected return of 17.3 percent. A risk-free asset currently earns 4.6 percent. If a portfolio of the two assets has a beta of .98, then the weight of the stock must be ___ and the risk-free weight must be___. .66; .34 βP = .98 = x(1.48) + (1 -x)(0) x = .66 Stock weight is .66 and the risk-free weight is .34 Stock Y has a beta of 1.28 and an expected return of 13.7 percent. Stock Z has a beta of 1.02 and an expected return of 11.4 percent. What would the risk-free rate have to be for the two stocks to be correctly priced relative to each other? 2.38 percent (.137 -Rf)/1.28 = (.114 -Rf)/1.02 Rf = .0238, or 2.38 percent Stock J has a beta of 1.06 and an expected return of 12.3 percent, while Stock K has a beta of .74 and an expected return of 6.7 percent. If you create portfolio with the same risk as the market, what rate of return should you expect to earn? 11.25 percent βP = 1.0 = 1.06x+ .74 (1 -x) x = .8125 E(RP) = .8125 (.123) + (1 -.8125) (.067) = .1125, or 11.25 percent Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 | Final Exam 1 2

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |