|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 9 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

Determine the retirement

savings contributions credit in each of the following cases. Use Table 9-2.

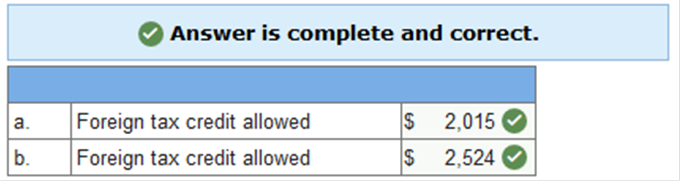

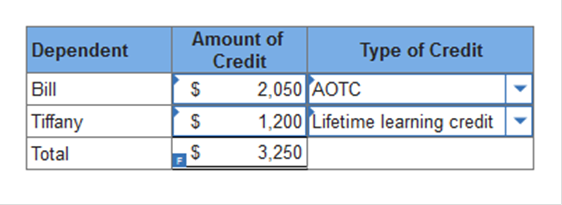

Explanation $344 = ($1,720 × 0.2) $174 = ($1,740 × 0.1) $191 = ($1,910 × 0.1) $1,000 = ($2,000 × 0.5); maximum contribution for the credit is $2,000. Jenna paid foreign income tax of $2,015 on foreign income of $10,076. Her worldwide taxable income was $99,800, and her U.S. tax liability was $25,000. What is the amount of foreign tax credit (FTC) allowed? What would be the allowed FTC if Jenna had paid foreign income tax of $3,400 instead? (Do not round intermediate calculations. Round your final answer to the nearest whole dollar amount.)

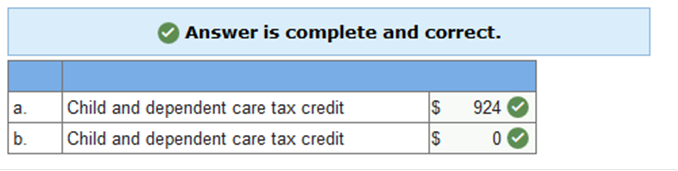

Explanation The amount of foreign tax credit is limited to the lesser of foreign tax paid or [(Foreign-source taxable income / worldwide taxable income) × U.S. tax liability] In this case, the limitation calculation is ($10,076 / $99,800) × $25,000 = $2,524. Thus, the amount of foreign tax credit is equal to the $2,015 foreign tax paid, since it is less. If the amount of foreign income tax paid had changed to $3,400, the limitation calculation above would be less than the tax paid and thus, the allowed foreign tax credit would be limited to $2,524. 10076 / 9980 x 25000 = 2524.04 (Foreign Credit of 2,015 is used because it is equal or less) (2) = 2,524 because it is limited Tim and Martha paid $6,600 in qualified employment-related expenses for their three young children, who live with them in their household. Martha received $1,800 of dependent care assistance from her employer, which was properly excluded from gross income. The couple had $39,800 of AGI earned equally. Use Child and Dependent Care Credit AGI schedule. What amount of child and dependent care tax credit can they claim on their Form 1040? How would your answer differ (if at all) if the couple had AGI of $37,300 that was earned entirely by Tim? Part 1: The amount of employment-related expense is limited to $6,000 for two or more children. This amount must be reduced by the $1,800 that Martha receives from employer. Thus, their allowed expenses are $4,200. Since their AGI was between 39001 & 41000, Tim and Martha are entitled to a credit to 22 % of their expenses, 924.00. Part: is ZERO because the COUPLE has to be gainfully employed

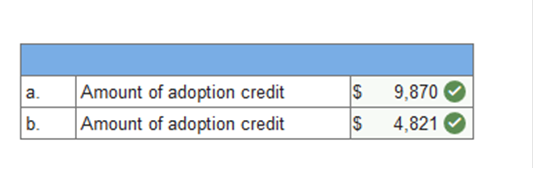

Explanation The amount of employment-related expenses is limited to $6,000 for two or more children. This amount must be reduced by the $1,800 that Martha received from her employer. Thus, their allowed expenses are $4,200. Since their AGI was over $39,000, Tim and Martha are entitled to a credit equal to 22% of their expenses, or $924. If the couple had AGI of $37,300 earned solely by Tim, the credit would be zero. The credit is permitted if you have child care expenses incurred to be gainfully employed. Since Martha was not employed, no credit is permitted. Allowed expenses are limited to the earned income of the taxpayer or the taxpayer’s spouse, whichever is smaller. Niles and Marsha adopted an infant boy (a U.S. citizen). They paid $18,000 in 2016 for adoption-related expenses. The adoption was finalized in early 2017. Marsha received $3,700 of employer-provided adoption benefits. For question (a), assume that any adoption credit is not limited by modified AGI or by the amount of tax liability. What amount of adoption credit, if any, can Niles and Marsha take in 2017? Using the information in question (a), assume that their modified AGI was $224,000 in 2017. What amount of adoption credit is permitted in 2017? (Do not round intermediate calculations. Round your final answer to the nearest whole dollar amount.)

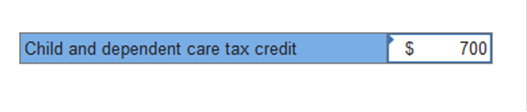

Explanation In general, a credit is allowed for 100% of adoption expenses (minus any reimbursements) up to a maximum of $13,570 per child. In this case, all of the expenses are incurred in the year before the adoption became final. Pre-final expenses are deductible in the year following payment. In addition, the total adoption expenses are $18,000, which exceeds the maximum. Therefore, the maximum allowed amount of $13,570 should be used to calculate the credit in 2017, the year the adoption was finalized. $9,870 of credit is allowed for year 2017 – the maximum amount allowed of $13,570 minus the $3,700 reimbursement from Marsha’s employer. The year 2017 preliminary credit of $9,870 would be further limited to $4,821 as follows: [($243,540 – $224,000 / $40,000] × $9,870 = $4,821. Adrienne is a single mother with a 6-year-old daughter who lived with her during the entire year. Adrienne paid $2,500 in child care expenses so that she would be able to work. Of this amount, $500 was paid to Adrienne’s mother, whom Adrienne cannot claim as a dependent. Adrienne had net earnings of $2,000 from her jewelry business. In addition she received child support payments of $21,100 from her ex-husband. Use Child and Dependent Care Credit AGI schedule. What amount, if any, of child and dependent care tax credit can Adrienne claim?

Explanation The payment to Adrienne’s mother is a permitted child-care expense. The amount of employment-related expense is limited to the lesser of $3,000 (in the case of one qualifying child) or the amount of earned income. Here, Adrienne’s expense amount is limited to $2,000 – the amount of her earned income from her business. Child support received, for the purposes of the child care credit, is not considered earned income nor is it used to determine the amount of AGI for this credit. Therefore, Adrienne is entitled to a credit percentage of 35% based on her AGI of $2,000. Thus, Adrienne is entitled to a child and dependent care tax credit of $700 ($2,000 × .35). New HW

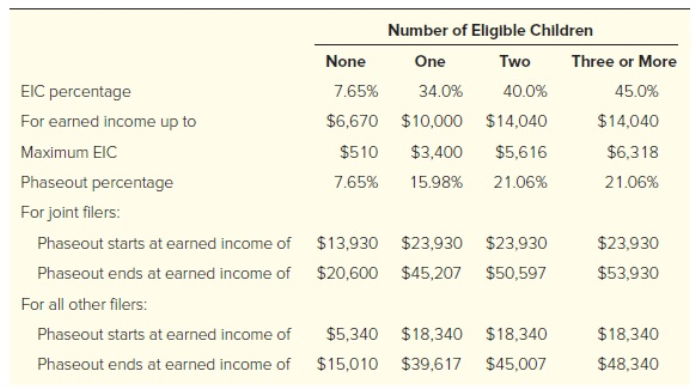

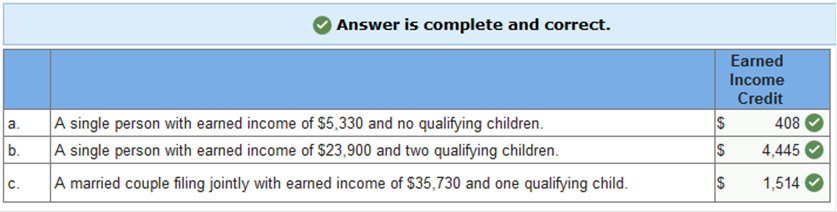

Determine the amount of Earned Income Credit in each of the following cases. Assume that the person or persons is/are eligible to take the credit. Calculate the credit using the formulas. (Do not round intermediate calculations. Round your final answers to the nearest whole dollar amount.) Use Table 9-3.

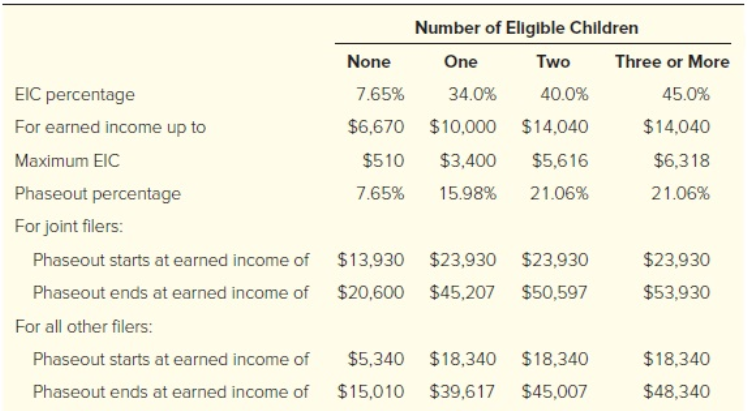

rev: 04_18_2018_QC_CS-125002 Explanation $5,320 × 7.65% = $407 $5,616 – [($24,000-$18,340) × .2106] = $4,424. $3,400 – [($35,840 - $23,930) × .1598] = $1,497. Tim and Martha paid $6,500 in qualified employment-related expenses for their three young children, who live with them in their household. Martha received $1,700 of dependent care assistance from her employer, which was properly excluded from gross income. The couple had $39,700 of AGI earned equally. Use Child and Dependent Care Credit AGI schedule. What amount of child and dependent care tax credit can they claim on their Form 1040? How would your answer differ (if at all) if the couple had AGI of $37,400 that was earned entirely by Tim?  Explanation The amount of employment-related expenses is limited to $6,000 for two or more children. This amount must be reduced by the $1,700 that Martha received from her employer. Thus, their allowed expenses are $4,300. Since their AGI was over $39,000, Tim and Martha are entitled to a credit equal to 22% of their expenses, or $946. If the couple had AGI of $37,400 earned solely by Tim, the credit would be zero. The credit is permitted if you have child care expenses incurred to be gainfully employed. Since Martha was not employed, no credit is permitted. Allowed expenses are limited to the earned income of the taxpayer or the taxpayer’s spouse, whichever is smaller. In 2017, Jeremy and Celeste, who file a joint return, paid the following amounts for their daughter, Alyssa, to attend the University of Colorado, during academic year 2017-2018. Alyssa was in her first year of college and attended full-time.

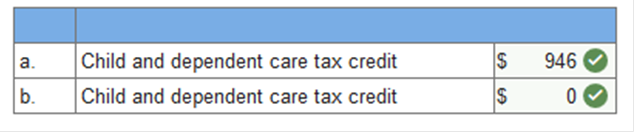

The spring semester at the University of Colorado begins in January. In addition to the above, Alyssa’s uncle Devin sent $300 as payment for her tuition directly to the University. Jeremy and Celeste have modified AGI of $173,000. What is the amount of qualifying expenses for purposes of the American Opportunity Tax credit (AOTC) in tax year 2017? What is the amount of the AOTC that Jeremy and Celeste can claim based on their AGI? (Do not round your intermediate computations.)

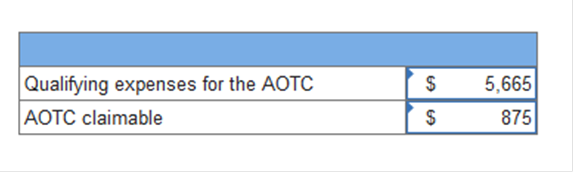

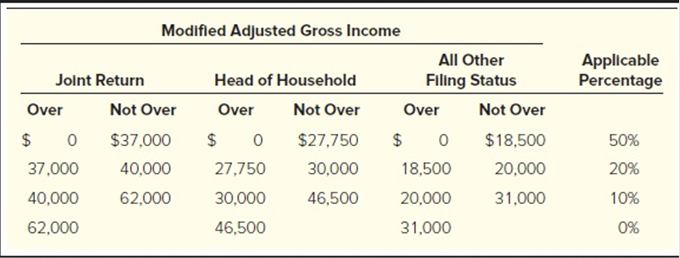

Explanation Qualifying expenses for the AOTC is $5,665 = ($2,450 + $1,315 + $1,600 + $300). Qualifying expenses do not include amounts paid for room and board. Since Jeremy and Celeste’s modified AGI exceeds $160,000, their AOTC is $875.00, calculated as follows: [($180,000 − $173,000)/$20,000 × $2,500] = $875. Walt and Deloris have two dependent children, Bill and Tiffany. Bill is a freshman at State University, and Tiffany is working on her graduate degree. The couple paid qualified expenses of $2,200 for Bill (who is a half-time student) and $6,000 for Tiffany. What are the amount and type of education tax credits that Walt and Deloris can take, assuming they have no modified AGI limitation?

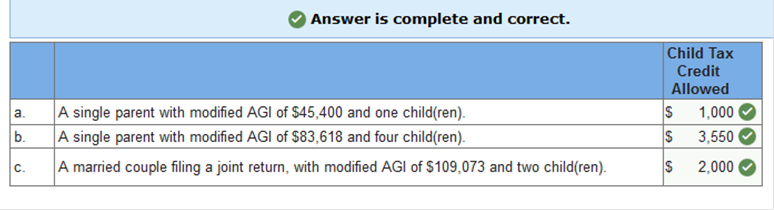

Explanation The American opportunity tax credit (AOTC) is available for students in their first four years of study who are attending at least half-time. Therefore, the expenses for Bill are allowed for the AOTC, resulting in a credit of $2,050 (100% of the first $2,000 plus 25% of the remaining $200). Tiffany is not eligible for the AOTC since she is past her first four years of postsecondary education. The lifetime learning credit is 20% of up to $10,000 of qualified expenses incurred for study at any postsecondary level. Thus, Tiffany's expenses are eligible for a lifetime learning credit of $1,200. Although Bill also qualifies for a lifetime learning credit, the AOTC is greater. Both credits cannot be taken for the same expenses. Thus, Walt and Deloris should claim an AOTC of $2,050 for Bill and a lifetime learning credit of $1,200 for Tiffany, for a total of $3,250. Determine the amount of child tax credit in each of the following cases:

Explanation A taxpayer is entitled to a $1,000 credit for each qualifying child unless limited by modified AGI. The credit is reduced by $50 for each $1,000, or fraction thereof, by which modified AGI exceeds $110,000 (married), $75,000 (single), or $55,000 (married filing separately). $1,000. The modified AGI limits do not apply. $3,550. Without regard to the limitation, the person is entitled to a child tax credit of $4,000. However, modified AGI exceeds the limitation by $8,618 ($83,618 − $75,000). Thus, there are nine $50 reductions. $2,000. The modified AGI limits do not apply. Assuming that an AGI limitation does not apply what amounts of credit for the elderly, or the disabled would be permitted in each of the following instances?

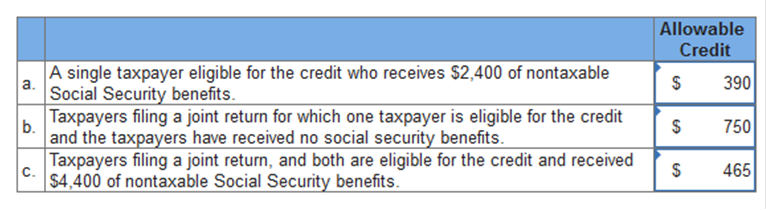

Explanation The credit for the elderly or the disabled is equal to 15% of the allowable base amount. Since the AGI limit is assumed not to apply, the allowable amount for this problem is the base amount ($7,500 joint return where both qualify, $5,000 single return or joint where only one spouse qualifies, or $3,750 for married filing separately), reduced by the amount of nontaxable Social Security benefits. The credit will then be 15% of the resultant allowable amount. Base amount of $5,000 minus $2,400 nontaxable benefits = $2,600 × 0.15 = $390 credit for the elderly or the disabled. Base amount of $5,000 minus $0 nontaxable benefits = $5,000 × 0.15 = $750 credit for the elderly or the disabled. Base amount of $7,500 minus $4,400 nontaxable benefits = $3,100 × 0.15 = $465 credit for the elderly or the disabled. In 2017, Jeremy and Celeste, who file a joint return, paid the following amounts for their daughter, Alyssa, to attend the University of Colorado, during academic year 2017-2018. Alyssa was in her first year of college and attended full-time.

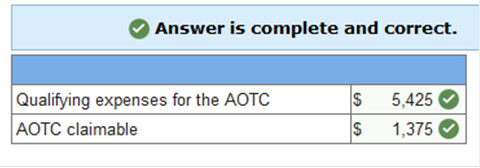

The spring semester at the University of Colorado begins in January. In addition to the above, Alyssa’s uncle Devin sent $200 as payment for her tuition directly to the University. Jeremy and Celeste have modified AGI of $169,000. What is the amount of qualifying expenses for purposes of the American Opportunity Tax credit (AOTC) in tax year 2017? What is the amount of the AOTC that Jeremy and Celeste can claim based on their AGI? (Do not round your intermediate computations.)

Explanation Qualifying expenses for the AOTC is $5,425 = ($2,170 + $1,595 + $1,460 + $200). Qualifying expenses do not include amounts paid for room and board. Since Jeremy and Celeste’s modified AGI exceeds $160,000, their AOTC is $1,375.00, calculated as follows: [($180,000 − $169,000)/$20,000 × $2,500] = $1,375.

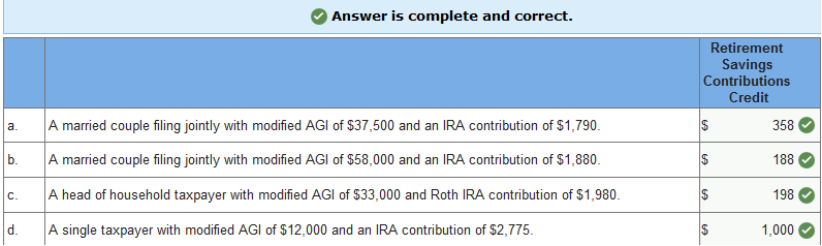

Determine the retirement savings contributions credit in each of the following cases. Use Table 9-2.

Explanation $358 = ($1,790 × 0.2) $188 = ($1,880 × 0.1) $198 = ($1,980 × 0.1) $1,000 = ($2,000 × 0.5); maximum contribution for the credit is $2,000.

Determine the amount of Earned Income Credit in each of the following cases. Assume that the person or persons is/are eligible to take the credit. Calculate the credit using the formulas. (Do not round intermediate calculations. Round your final answers to the nearest whole dollar amount.) Use Table 9-3.

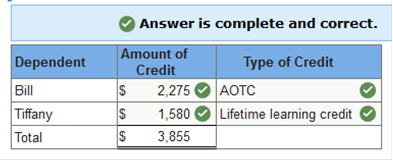

Explanation $5,330 × 7.65% = $408 $5,616 – [($23,900-$18,340) × .2106] = $4,445. $3,400 – [($35,730 - $23,930) × .1598] = $1,514. Walt and Deloris have two dependent children, Bill and Tiffany. Bill is a freshman at State University, and Tiffany is working on her graduate degree. The couple paid qualified expenses of $3,100 for Bill (who is a half-time student) and $7,900 for Tiffany. What are the amount and type of education tax credits that Walt and Deloris can take, assuming they have no modified AGI limitation?

Explanation The American opportunity tax credit (AOTC) is available for students in their first four years of study who are attending at least half-time. Therefore, the expenses for Bill are allowed for the AOTC, resulting in a credit of $2,275 (100% of the first $2,000 plus 25% of the remaining $1,100). Tiffany is not eligible for the AOTC since she is past her first four years of postsecondary education. The lifetime learning credit is 20% of up to $10,000 of qualified expenses incurred for study at any postsecondary level. Thus, Tiffany's expenses are eligible for a lifetime learning credit of $1,580. Although Bill also qualifies for a lifetime learning credit, the AOTC is greater. Both credits cannot be taken for the same expenses. Thus, Walt and Deloris should claim an AOTC of $2,275 for Bill and a lifetime learning credit of $1,580 for Tiffany, for a total of $3,855. Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |