|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 8 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

Ramone is a tax attorney

and he owns an office building that he rents for $8,600/month.

He is responsible for paying all taxes and expenses relating to the building’s operation and maintenance. Is Ramone engaged in the trade or business of renting real estate? No Explanation No, the office building would be treated as rental property and not a trade or business. The general rule is that Ramone must materially participate in the rental activity and provide substantial services to the rental property. Additionally, Ramone must be considered a real estate professional if the activity is to be treated as a trade or business. Mabel, Loretta, and Margaret are equal partners in a local restaurant. The restaurant reports the following items for the current year:

Each partner receives a Schedule K-1 with one-third of the preceding items reported to her. How must each individual report these results on her Form 1040? (Do not round any division. Round your final answer to the nearest whole dollar value. Negative amounts should be indicated by a minus sign.) Schedule A

Explanation

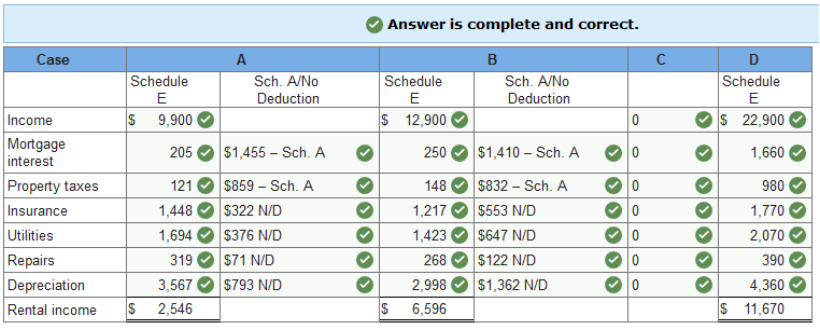

Janet owns a home at the lake. She incurs the following expenses:

Use the Tax Court allocation method, if applicable. (Round your intermediate computations to 5 decimal places and final answers to nearest whole dollar value).

Explanation Income = $9,900 Mortgage interest = (45/365):($205) Property taxes = (45/365):($121) Insurance = (45/55):($1,448) Utilities = (45/55):($1,694) Repairs = (45/55):($319) Depreciation = (45/55):($3,567) Rental Income = $2,546 For less than 15 days rental, there is no income or rental expense reported. Interest and taxes are deducted on Schedule A. Randolph and Tammy own a second home. They spent 45 days there and rented it for 88 days at $166 per day during the year. The total costs relating to the home include the following: (Round your intermediate computations to 5 decimal places and final answers to nearest whole dollar value).

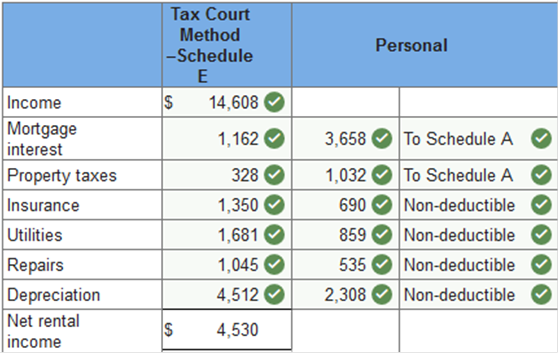

What is the tax treatment of these items relating to second home under Tax Court allocation method? What is the tax treatment of these items relating to second home under IRS allocation method? Which of the methods is preferred? Required a What is the tax treatment of these items relating to second home under Tax Court allocation method?

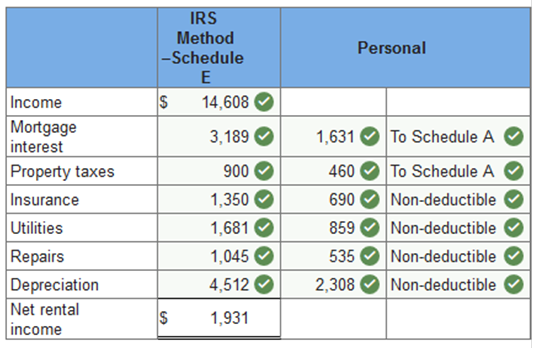

Required b What is the tax treatment of these items relating to second home under IRS allocation method?

Required c Which of the methods is preferred?

Explanation a.

b.

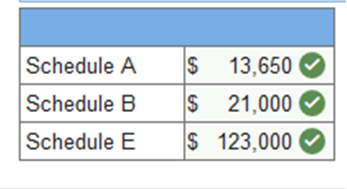

c. The IRS method produces the least amount of net rental income for Randolph and Tammy and would be the preferable allocation of expenses for them. Net rental income reported using the Tax Court method is $2,599 greater than they are under the IRS method. Itemized deductions however, are $2,599 greater under the Tax Court method. Nicole and Mohammad (married taxpayers filing jointly) are equal owners in an S corporation. The company reported sales revenue of $410,000 and expenses of $287,000. The corporation also earned $21,000 in taxable interest and dividend income and had $13,650 investment interest expense. How are these amounts reported for tax purposes in the following schedules?

Explanation

Interest and dividends of $21,000 are reported as interest and dividends separately on Schedule B, Form 1040. The investment interest expense is an itemized deduction on Schedule A.

Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |