|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 7 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

Davidson Industries, a

sole proprietorship, sold the following assets in 2017:

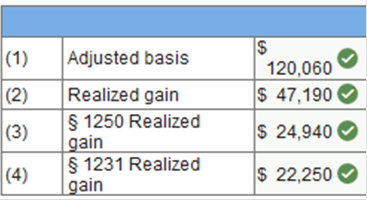

The following questions relate to the sale of the warehouse: (1) What is the adjusted basis of the warehouse? (2) What is the realized gain on the warehouse? (3) What amount of the gain is taxed according to § 1250 rules? (4) What amount is considered a § 1231 gain before netting? The following questions relate to the sale of the truck: (1) What is the adjusted basis of the truck? (2) What is the realized gain on the truck? (3) What amount of the gain is taxed according to § 1245 rules? (4) What amount of the gain is taxed as ordinary income? The following questions relate to the sale of the computer: (1) What is the adjusted basis of the computer? (2) What is the realized gain or loss on the sale? (3) Which IRC section code applies to this asset? Required a What is the adjusted basis of the warehouse? (2) What is the realized gain on the warehouse? (3) What amount of the gain is taxed according to § 1250 rules? (4) What amount is considered a § 1231 gain before netting?

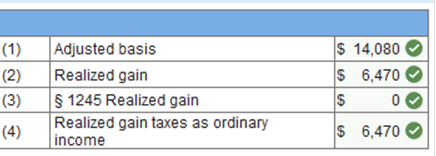

Required b What is the adjusted basis of the truck? (2) What is the realized gain on the truck? (3) What amount of the gain is taxed according to § 1245 rules? (4) What amount of the gain is taxed as ordinary income?

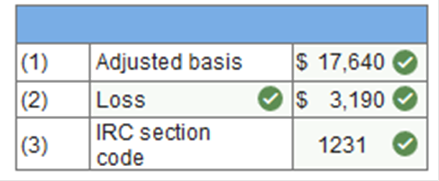

Required c (1) What is the adjusted basis of the computer? (2) What is the realized gain or loss on the sale? (3) Which IRC section code applies to this asset?

Explanation

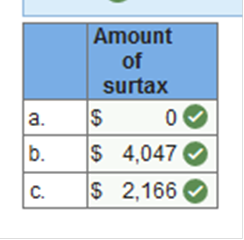

The warehouse is a § 1250 asset. The gain from the sale is treated as a long-term capital gain ($24,940 of the gain would be an unrecaptured § 1250 gain subject to the 25% tax rate, the remaining gain of $22,250 is netted with other § 1231 gains and losses). The truck is a § 1245 asset subject to recapture to the extent of depreciation taken, but because the asset was held for less than one year it is considered an ordinary income asset and the $6,470 gain is treated as ordinary income. The computer is a § 1231 loss and therefore is netted with § 1231 gains. Respond to the following independent situations: Masa and Haiming, husband and wife, filing jointly, earn $275,500 in salaries and do not have any net investment income. Masa and Haiming, husband and wife, filing jointly, earn $214,000 in salaries and $57,000 in capital gains, $57,000 in dividends, and $28,500 in savings interest for a total MAGI of $356,500. Masa and Haiming, husband and wife, filing jointly, earn $345,000 in salaries and $57,000 in capital gains for a total MAGI of $402,000. How much in surtax will Masa and Haiming be assessed on their Form 1040 for 2017?

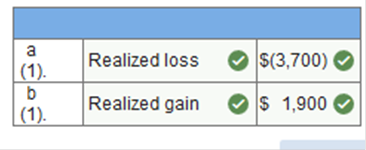

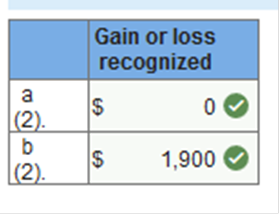

Explanation The taxpayers do not have any net investment income. The taxpayers met the threshold of $250,000. The surtax is assessed on the lesser of the net investment income of $142,500 or the amount by which they are over the threshold, which is $106,500. The taxpayers met the threshold of $250,000. The surtax is assessed on the lesser of the net investment income of $57,000 or the amount by which they are over the threshold, which is $152,000. Brantley owns an automobile for personal use. The adjusted basis is $15,500, and the FMV is $11,800. Assume Brantley has owned the automobile for two years. Respond to the following if Brantley sells the vehicle for $11,800. (1) What is the amount of realized gain or loss on the sale? (2) What is the amount Brantley will recognize on his Form 1040? Respond to the following if Brantley sells the vehicle for $17,400. (1) What is the amount of realized gain or loss on the sale? (2) What is the amount Brantley will recognize on his Form 1040? Req a1 and b1 a(1). Respond to the following if Brantley sells the vehicle for $11,800. What is the amount of realized gain or loss on the sale?

(1). Respond to the following if Brantley sells the vehicle for $17,400. What is the amount of realized gain or loss on the sale?

Explanation a. (1)

(2) Since this is a personal asset, the loss on the sale would not be deductible. b. (1)

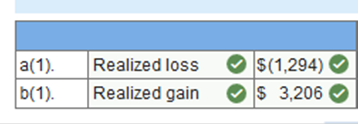

The $1,900 realized gain would also be recognized. Umair sold some equipment he used in his business on August 29, 2017, that was originally purchased for $46,000 on November 21, 2016. The equipment was depreciated using the 7-year MACRS method for a total of $12,206. Assume there is no additional netting of gains and losses for this taxpayer. Assume Umair sold the equipment for $32,500: (1) What is the amount of realized gain or loss on the sale of the equipment? (2) Is the nature of the gain or loss considered ordinary or long-term? Assume Umair sold the equipment for $37,000: (1) What is the amount of realized gain or loss on the sale of the equipment? (2) Is the nature of the gain or loss considered ordinary or long-term? Req a1 and b1 a(1). Assume Umair sold the equipment for $32,500. What is the amount of realized gain or loss on the sale of the equipment? b(1). Assume Umair sold the equipment for $37,000. What is the amount of realized gain or loss on the sale of the equipment?

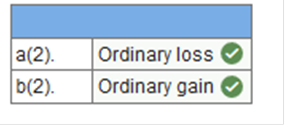

Req a2 and b2 a(2). Assume Umair sold the equipment for $32,500. Is the nature of the gain or loss considered ordinary or long-term? b(2). Assume Umair sold the equipment for $37,000. Is the nature of the gain or loss considered ordinary or long-term?

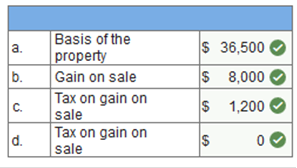

Explanation a. (1) $32,500 − $33,794 = ($1,294) loss (2) This is an ordinary loss and initially is recorded on Form 4797; if there is no other netting, this amount will go on the front of Form 1040 as a loss. b. (1) $37,000 − $33,794 = $3,206 gain (2) This is § 1245 property and will be initially recorded on Form 4797. The gain of $3,206 is taxed at regular rates up to the amount of depreciation taken. Using the following independent situations, answer the following questions: Situation 1 Clara received from her Aunt Sona, property with a FMV at the date of the gift of $43,000. Aunt Sona purchased the property five years ago for $36,500. Clara sold the property for $44,500. Assume Aunt Sona does not have MAGI of over $200,000. a. What is the basis to Clara? b. What is Clara’s gain on the sale? c. If Clara is in the 33% tax bracket, what is the tax on the gain (assuming she has no other gains/losses to be netted)? d. If Clara is in the 15% tax bracket, what is the tax on the gain (assuming she has no other gains/losses to be netted)?

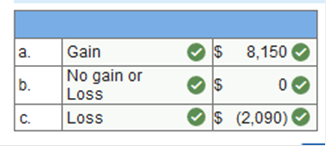

Situation 2 Clara received from her Aunt Sona, property with a FMV at the date of the gift of $29,000. Aunt Sona purchased the property five years ago for $35,500. a. If Clara sold the property for $43,650, what is her gain or loss on the sale? b. If Clara sold the property for $33,410, what is her gain or loss on the sale? c. If Clara sold the property for $26,910, what is her gain or loss on the sale?

Explanation Situation #1 Basis to Clara is $36,500 since it is less than FMV at date of gift and the property is sold for more than the basis. $44,500 – $36,500 = $8,000 $8,000 × 15% = $1,200 Rule applies where taxpayer is in <=25% tax bracket, no tax on gain. Situation #2 ($43,650 – $35,500). The basis is used to calculate a gain when FMV is lower than basis at the date of the gift. No gain or loss. When the FMV is lower than the basis at the date of the gift, any sales between the FMV and basis generate no gain or loss. ($26,910 – $29,000). The FMV is used to calculate a loss when the FMV is lower than the basis at the date of the gift. Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |