|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 6 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

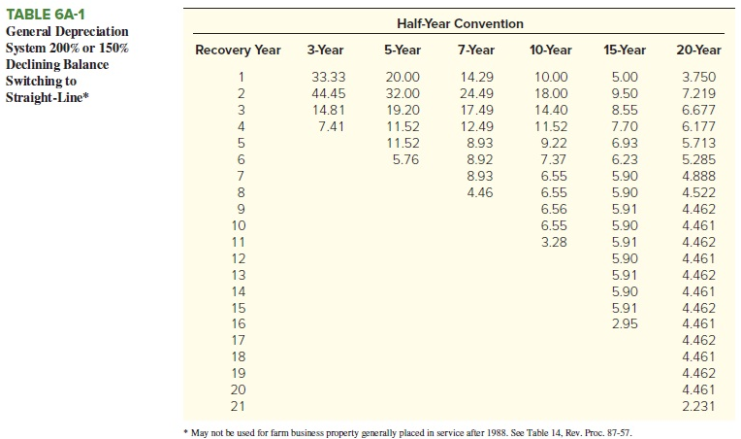

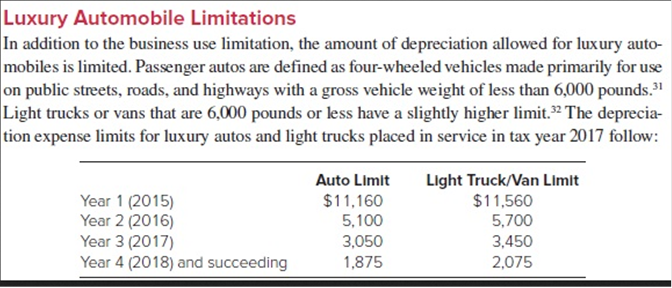

On February 4, 2017, Jackie purchased and placed in service a car she purchased for $21,400. The car was used exclusively for her business. Compute Jackie’s cost recovery deduction in 2017 assuming no §179 expense but the bonus was taken. (Use Table 6A-1 and Luxury Automobile Depreciation)

Explanation

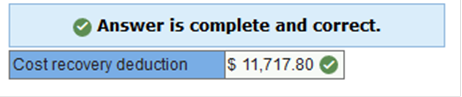

On June 10, 2017, Huron purchased equipment (7-year class property) for $82,000. Determine Huron’s cost recovery deduction for computing 2017 taxable income. Assume that Huron does not make the §179 or bonus elections. (Use Table 6A-1) (Round your answer to 2 decimal places.)

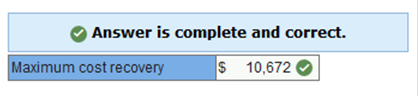

Explanation $82,000 × 14.29% = $11,717.80 Michael is the sole proprietor of a small business. In June 2017, his business income is $8,700 before consideration of any § 179 deduction. He spends $229,500 on furniture and equipment in 2017. If Michael elects to take the § 179 deduction and no bonus on a conference table that cost $22,500 (included in the $229,500 total), determine the maximum cost recovery for 2017 with respect to the conference table: (Use Table 6A-1 and Table 6A-2) (Round your intermediate calculations to the nearest whole dollar amount.)

Explanation Remember, §179 cannot create a NOL. Therefore, the §179 expense is limited to $8,700.

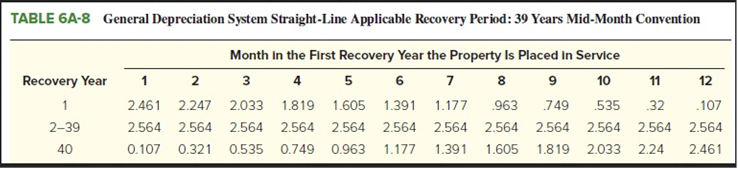

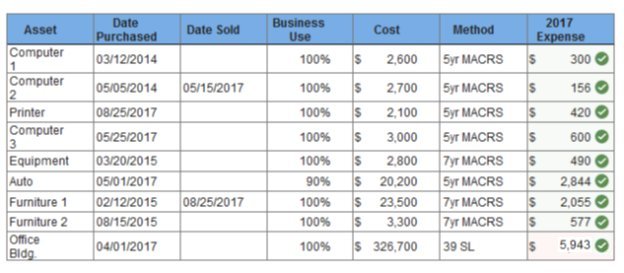

22500 – 8700 = 13800 13800 x .1429 (14.29%) = 1972.02 1972.02 + 8700 = 10672.02 Casper used the following assets in his Schedule C trade or business in the tax year 2017. Casper is a new client and unfortunately does not have a copy of his prior year's tax return. He recalls that all of the assets purchased in prior years used MACRS depreciation (no §179 expense). Casper does not wish to take §179 or bonus depreciation. (Use Table 6A-1 and Table 6A-8) Calculate the current year depreciation allowance for Casper’s business. (Round your final answers to the nearest whole dollar amount.)

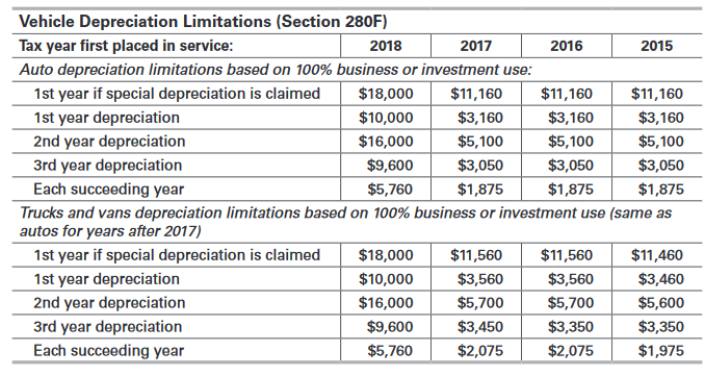

Explanation Auto: The luxury auto limits depreciation to $2,844 ($3,160 year 1 limitation multiplied by the 90% business use). Computer 1 2,600 x 11.52% Computer 2 2,700 x 5.76% Printer 2,100 x 20.00% Computer 3 3,000 x 20.00% Equipment 2,800 x 17.49% Auto 20,200 Limited to (3160 x .9%) Furniture 1 23,500 x 8.745% Furniture 2 3,300 x 17.490% Office bldg.. 326,700 1.82% Jose purchased a vehicle for business and personal use. In 2017, he used the vehicle 10,000 miles for business (80% of total), and calculated his vehicle expenses using the standard mileage rate (mileage was incurred ratably throughout the year). He paid $800 in interest and $80 in property taxes on the car. Calculate the total business deduction related to the car: (Round your final answer to the nearest whole dollar value.)

What are the two components of the self-employment tax? Is either component limited? Self-employment tax consists of two parts, the Social Security tax and the Medicare tax. The tax base for the Social Security tax is limited. In tax year 2020, only the first $137,700 of wage and self-employment income is subject to the Social Security tax. The Medicare tax is not limited Rueben acquires a warehouse on September 1, 2020, for $3 million. On March 1, 2024, he sells the warehouse. Determine Rueben cost recovery for 2020-2024. 2020: 3,000,000 x 0,749% = $ 22,470 2021: 3,000,000 x 2.564% = 76,920 2022: 3,000,000 x 0,749% = 22,470 2023: 3,000,000 x 0,749% = 22,470 2024: 3,000,000 x 2.5/12 = 16,025 On May 5, 2012, Jill purchased equipment for $40,000 to be used in her business. She did not elect to expense the equipment under § 179 or bonus depreciation. On January 1, 2017, she sells the equipment to a scrap metal dealer. What is the cost recovery deduction for 2017? $1,784 40,000 x 0.0892 x 0.50 = 1,784 Kelly is a self-employed tax attorney whose practice primarily involves tax planning. During the year, she attended a three-day seminar regarding new changes to the tax law. She incurred the following expenses. Lodging $400 Meals 95 Course registration 350 Transportation 150 a. How much can Kelly deduct? b. Kelly believes that obtaining a CPA license would improve her skills as a tax attorney. She enrolls as a part-time student at a local college to take CPA review courses. During the current year, she spends $1500 for tuition and $300 for books. How much of these expenses can Kelly deduct? Why? a. Total 947.50 Lodging 400.00 Meals(50%) 47.50 Registration 350.00 Transportation 150.00 b. education expenses are deductible if they are for education that (1) maintains or improves skills required by the taxpayer in his employment or (2) meets the express requirements of an employer or law. However, the education expenses are not deductible if the education qualified the taxpayer for a new trade or business. Since obtaining a CPA qualifies Kelly for a new profession (although related), the expenses are not deductible. In this situation an argument can be made that the education does not qualify Kelly for a new profession because she is already in the tax profession. Janet purchases her personal residence in 2010 for $250,000. In January 2020 she converted it to rental property. The fair market at the time of conversion was $210,000 a. Determine the amount of cost recovery that can be taken in 2020 $7,318.50 b. Determine the amount of cost recovery that could be taken in 2020 if the fair market value of the property were $350,000 $12,197.50 a. 210,000 x .03485 = 7,318.50 b. 350,000 x .03485 = 12,197.50 Trade or business expenses are treated as A deduction for AGI. Atlas, a financial consultant, had the following income and expenses in his business: Fee income $235,000 Expenses: 1. Rent expense 18,000 2. Penalties assessed by the SEC 2,500 3. Office expenses 6,000 4. Supplies 6,000 5. Interest paid on note used to acquire office equipment 2,700 6. Speeding tickets going to see clients 650 How much net income must Atlas report from this business? $202,300 18,000 + 6,000 + 6,000 + 2,700 = 202,300 On April 15, 2015, Andy purchased some furniture and fixtures (7-year property) for $10,000 to be used in his business. He did not elect to expense the equipment under § 179 page 6-52 or bonus depreciation. On June 30, 2017, he sells the equipment. What is the cost recovery deduction for 2017? $875. David is a college professor who does some consulting work on the side. He uses 25% of his home exclusively for the consulting practice. He is single and 63 years old. His AGI is 45,000. Other information follows: Income from consulting business $ 4,000 Consulting expenses 1,500 Total costs related to home: Interest and taxes 6,500 Utilities 1,500 Maintenance and repairs 450 Deprecation (business part only) 1,500 Calculate Davids AGI AGI before business $45,000 Business Proceeds $4,000 Business expenses (1,500) Interest and taxes (25%) (1,625) Utilities (25%) (375) Main. and repaires (25%) (113) Depreciation (25%) limited to (387) Net Business income 0 AGI 45,0000 Lawrence purchased an apartment building on February 10, 2017, for $330,000, $30,000 of which was for the land. What is the cost recovery deduction for 2017? $9,546.00 330,000 – 30,000 = 300,000 x 0.03182 = 9,546.00 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project2

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |