|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 5 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

During the year 2017, Ricki, who is not self-employed and does not receive employer reimbursement for business expenses, drove her car 6,800 miles to visit clients, 11,800 miles to get to her office, and 500 miles to attend business-related seminars. All of this mileage was incurred ratably throughout the year. She spent $570 for airfare to another business seminar and $290 for parking at her office. Using the automobile expense rates in effect for 2017, what is her deductible transportation expense? (Do not round your intermediate calculations. Round your final answer to two decimal places.)

Explanation

The commuting miles to her office, as well as the office parking fees, are not deductible; however, the miles from her office to a client location are deductible. Reggie, who is 55, had AGI of $24,400 in 2017. During the year, he paid the following medical expenses:

Reggie received $560 in 2017 for a portion of the doctors’ fees from his insurance. What is Reggie’s medical expense deduction?

Explanation

Even though prescribed by a physician, the cost of the marijuana is not deductible because it cannot be legally procured per federal statute. Over-the-counter drugs are also not a permitted qualifying medical expense. Tyrone and Akira, who are married, incurred and paid the following amounts of interest during 2017:

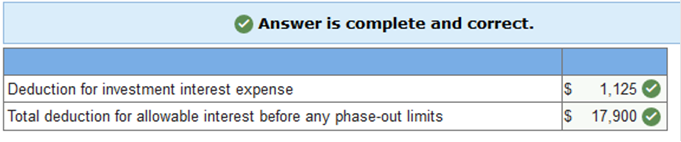

With 2017 net investment income of $1,125, calculate the amount of their allowable deduction for investment interest expense and their total deduction for allowable interest. Home acquisition principal is less than $1,000,000, and the home equity loan principal is less than $100,000.

Explanation Investment interest expense (limited to net investment income): $1,125 Allowable deduction for interest:

Reynaldo and Sonya, a married couple, had flood damage in their home due to a faulty water heater during 2017, which totally ruined the furniture that was stored in their garage. The following items were completely destroyed and not salvageable:

Their homeowner's insurance policy had a $12,025 deductible for the personal property, which was deducted from their insurance reimbursement of $16,825, resulting in a net payment of $4,800. Their AGI for 2017 was $38,500. What is the amount of casualty loss that Reynaldo and Sonya can claim on their joint return for 2017? 16825 – 4800 – 100 – (38500 x .10) = 8075

Explanation

Casualty loss calculations can be broken down into a 4 step process: 1) Determine the allowable loss. 2) Subtract any insurance reimbursement. 3) Deduct the $100 per casualty event. 4) Subtract the AGI threshold amount. Leslie and Jason, who are married filing jointly, paid the following expenses during 2019: Interest on a car loan: $100 Interest on lending institution loan (used to purchase municipal bonds): $3,000 Interest on home mortgage (home mortgage principal is less than $750,000): $2,100 What is the maximum amount that they can use in calculating itemized deductions for 2019? $2,100. Mickey is a 12-year-old dialysis patient. Three times a week for the entire year he and his mother, Sue, drive 20 miles one way to Mickey's dialysis clinic. On the way home, they go 10 miles out of their way to stop at Mickey's favorite restaurant. Their total round trip is 50 miles per day. a. How many of those miles, if any, can Sue use to calculate an itemized deduction for transportation? b. Use the mileage rate in effect for 2019. a. No. of miles to be used: 6,240 b. Itemize deduction: $ 1,248 In 2017, Arturo’s pleasure boat that he purchased in 2012 for $43,300 was destroyed by a hurricane. His loss was not totally covered by his insurance. On what form(s) will Arturo report this loss? Tyrone and Akira, who are married, incurred and paid the following amounts of interest during 2019: Home acquisition debt interest $15,000 Credit card interest $5,000 Home equity loan interest (used for home improvement) $6,500 Investment interest expense $10,000 With 2019 net investment income of $2,000, calculate the amount of their allowable deduction for investment interest expense and their total deduction for allowable interest. Home acquisition principal, and the home equity loan principal combined are less than $750,000. Deduction for investment interest expense $2,000 Total deduction for allowable interest before any phase-out limits $23,500 2000 + 15,000 + 6,500 The for AGI deduction for the self-employment tax is based upon: a total of 7.65% of the employer's share of FICA taxes. Freya, who is single, had a student loan for qualified education expenses on which interest was due. For 2019, the total interest payments were $2,000. Assuming she has AGI under $70,000, how much may she deduct in arriving at adjusted gross income for 2019? $ 2,000 Zach attended Champion University during 2014-2018. He lived at home and was claimed by his parents as a deduction during the entire duration of his education. He incurred education expenses of $10,000 during college of which $2,000 was paid for by scholarships. To finance his education, he borrowed $7,000 through a federal student loan program and borrowed another $3,000 from a local lending institution for educational purposes. After graduation, he married and moved with his spouse to a distant city. In 2019, he incurred $700 of interest on the federal loans and $300 on the lending institution loan. He filed a joint return with his spouse showing modified AGI of $128,000. What amount of student loan interest can Zach and his spouse deduct in 2019, if any? Zach's allowed deduction: $800 Three types of payments are associated with a decree of separation or a divorce, executed on or before December 31, 2018 and not subsequently modified. a. What are those three payments? b. Which one potentially has a tax consequence? c. What is the timing rule regarding the "recapture" period of those payments? a. Alimony, child support, and property settlement b. Alimony c. Till third year payment Under the terms of a divorce decree executed May 1, 2018, Ahmed transferred a house worth $650,000 to his ex-wife, Farah, and was to make alimony payments of $3,000 per month. The property has a tax basis to Ahmed of $300,000. Required: a. How much of this must be reported on Farah's 2019 tax return? b. Of that amount, how much is taxable gain or loss that Farah must recognize related to the transfer of the house? a. $3,000 per month b. $0 Deductible education expenses include all of the following except: Room and board. If property is converted from personal-use property to business property, the depreciable cost basis is which of the following? The lower of the cost or FMV at the date of conversion. Meals and entertainment expenses are limited to 50%. False What form is filed to report the self-employment tax? Schedule SE. Which of the following is not a "trade or business" expense? Mortgage interest on a personal residence. Which expenses incurred in a trade or business are deductible? Supplies expenses. The cost of all personal property is recovered using a 200% declining-balance rate under MACRS. True Charles, a self-employed real estate agent, attended a conference on the impact of some new building codes on real estate investments. His unreimbursed expenses were as follows: Airfare $480 Lodging 290 Meals 100 Tuition and fees 650 How much can Charles deduct on his return? Since he is self-employed, the expenses are deducted on Schedule C as follows: Airfare 100% deductible $480 Lodging 100% deductible $290 Meals 50% deductible $50 Tuition and fees 100% deductible $650 Janet purchased her personal residence in 2009 for $250,000. In January 2019, she converted it to rental property. The fair market value at the time of conversion was $210,000. a. Determine the amount of cost recovery that can be taken in 2019. b. Determine the amount of cost recovery that could be taken in 2019 if the fair market value of the property were $350,000. a. $7,318.50 210,000 × 0.03485 = 7,318.50 b. $8,712.50 250,000 × 0.03485 = 8,712.50 Under MACRS, the straight-line method is required for all depreciable real property. True Rental activities by definition, are passive activities. True If a taxpayer materially participates in his/her rental activity as a real estate professional, the activity is considered a trade or business and not a passive activity. True In which of the following situations would a taxpayer be better off to take the foreign taxes paid as an itemized deduction rather than as a foreign tax credit? The foreign tax paid was a property tax. Warren and Erika paid $9,300 in qualified expenses for their son, Cash, to attend the University of Washington. Cash is in his first year of college and attended full-time. How much is Warren and Erika's American opportunity tax credit, without regard to any AGI limitation? $2,500. Kevin paid $2,550 in qualifying expenses for his daughter, Jasmine, who attended a community college. What is Kevin's lifetime learning credit without regard to AGI limitations or other credits? $510. Conner and Matsuko paid $1,000 and $2,000, in qualifying expenses for their two sons, Jason and Justin, respectively, to attend Idaho State University. Jason is a sophomore and Justin is a freshman. Conner and Matsuko's AGI is $195,000. What is their allowable American opportunity tax credit? $0. The AOTC phases out completely for AGI greater than $180,000 for MFJ taxpayers. Sandra is single and her son Julius is 12 years old. If her AGI is $79,000, what amount of child tax credit can Sandra claim? $2,000. Kim paid the following expenses during November 2019 for her son Joshua's spring 2020 expenses, which begins in January 2020: Tuition $14,000 Housing 8,000 Meal plan 2,500 In addition, Kim's sister paid $800 for college fees on behalf of Joshua directly to the college. Joshua is claimed as Kim's dependent on her tax return. How much of the paid expenses qualify for purposes of the education credit deduction for Kim in 2019? $14,800. Depreciation is allowed for every tangible asset (except land) used either in a trade or business or for the production of income. True Under MACRS, 5-year property includes: Automobiles and light trucks used in a trade or business. The self-employment tax is calculated on: Form SE For the deduction of self-employment taxes, which of the following statements is correct? They are 50% deductible as a for AGI deduction. Sam paid the following expenses during October 2019 for his son Aaron's spring 2020 college expenses: Spring 2020 semester begins in January 2020: Tuition $18,000 Housing 8,000 Meal plan 3,500 In addition, Aaron's uncle paid $500 for college fees on behalf of Aaron directly to the college. Aaron is claimed as Sam's dependent on his tax return. How much of the paid expenses qualify for purposes of the education credit deduction for Sam in 2019? $18,500. Lupe paid the following expenses during December 2019 for her son David's spring 2020 college expenses. The semester begins in February 2020. Tuition $16,000 Housing 6,000 Meal plan 2,500 David is claimed as a dependent on Lupe's tax return. How much of the above expenses qualify for purposes of Lupe's education credit deduction in 2019? $16,000. Jaylen made a charitable contribution to his church in the current year. He donated common stock valued at $33,000 (acquired as an investment in 2005 for $13,000). Jaylen's AGI in the current year is $75,000. Required: a. What is his allowable charitable contribution deduction? b. How are any excess amounts treated? a. Charitable contribution deduction: $22,500 b. Carryover: $10,500 If a family member of a taxpayer uses the rental property and pays full rental value, then those days rented are considered rental days False The deduction for self-employment taxes in 2019 is deductible as an above-the-line deduction at a rate of 7.65% based on the employer's portion of the taxes. True Jonathan and Sandy rented their cabin for 123 days and used the cabin for personal use for 55 days. The cabin is considered personal/rental property. True A property rented for less than 15 days should report its rental income on Schedule E. False Mindy and Xavier have a total tax liability of $475 before EIC. Their EIC for the current year is $2,578. What is their total tax refund or tax owed for the current year (assume they have no other credits or additional tax liability)? $2,103 tax refund. Maria and Vincent, whose modified AGI is $169,000, adopted a little girl from Mexico which was finalized in 2019. They incurred a total of $16,000 in qualified adoption expenses. What is the amount of adoption credit they can claim in 2019? $14,080. Julia and Omar are married and file a joint tax return. They have two dependent daughters, ages 14 and 18. If their AGI is $98,000, what amount of child or other qualifying dependents tax credit can they claim? $4,000. Which of the following is not a qualifying child for purposes of calculating the EIC? Son or daughter. Grandson or granddaughter. Eligible foster child. All of these qualify. A royalty is a payment for the right to use intangible property. True Casey and Lupe have AGI of $425,000. They have twin daughters, Ashley and Alley, ages 5. What amount of child tax credit can they claim? $2,750. 425,000 − 400,000 = 25,000) / 1,000] = 25 4,000 − (50 × 25) = 2,750. When royalties are paid, the amount paid is sent to the recipient by the payer on a Schedule K-1 False Generally, a taxpayer uses Schedule C to report royalty income. False Royalties resulting from a non-trade or non-business activity should be reported on a Schedule E. True Flow-through entities are named as such because they are taxed continuously. False Flow-through entities file "informational returns." True Income from a partnership to its partner is considered self-employment income. True Caroline, who files as head of household, received $9,000 of social security benefits. Her AGI before the social security benefits was $27,000. She also received $200 of tax- exempt interest. What is the amount of taxable social security benefits? $3,350 Which type of interest received is taxable and must be reported on the tax return? Interest on a savings account. When filing their tax returns, almost all individuals use: The cash receipts and disbursements method. Employer-paid premiums on life insurance are not taxable to the employees, unless the coverage is in excess of: $50,000 Provisional income is calculated by starting with Adjusted Gross Income (AGI) before social security benefits and adding back specific items. One of these items is: Deducted interest on educational loans. Corporate distributions to shareholders that represent a nontaxable return of capital are those that are: made from the excess over earnings and profits of the corporation When an individual's taxable income tax rate is less than $39,475, the tax rate on qualified dividends is: 0% Which of the following statements is incorrect concerning rental properties? Capital improvements may be deducted as an expense in the year the improvements are made. Rental income is generally reported on Schedule C. False In general, losses from passive activities may be deducted only to the extent that there is passive income. True Flow-through entities supply each owner at the end of the year with a Schedule E, indicating his/her income and expenses to report. False Each owner is supplied a K-1 indicating the owner's share of income, expenses, or losses. A primarily rental property must report its income and expenses on a Schedule E. True Joey and Susan rented their house for 2 weeks and used it for personal use for the remainder of the year. The house is considered personal/rental property. False A security deposit for a rental property is not reported as income. True There are two methods available to taxpayers to allocate expenses between personal and rental use of properties. True Royalties cannot be earned from which of the following: STOCKS In the case of personal/rental property, a taxpayer can deduct expenses only to the extent that there is rental income. True Life insurance proceeds because of the death of the insured are fully excludable from the gross income of the recipient if the payment is made: As a lump sum. A property rented for less than 15 days and used for personal use the remainder of the year, should have the rental income reported on Schedule E. False When royalties are paid, the amount paid is reported to the recipient by the payer at the end of the year on a Schedule K-1. False Flow-through entities are named as such because they are taxed continuously. False A taxpayer with a rental activity may be allowed up to $25,000 of rental losses against other (active or portfolio) income. TRUE Which of the following statements is incorrect concerning rental properties? Capital improvements may be deducted as an expense in the year the improvements are made. Rental income is generally reported on Schedule C. False In general, losses from passive activities may be deducted only to the extent that there is passive income. True Flow-through entities supply each owner at the end of the year with a Schedule E, indicating his/her income and expenses to report. False A primarily rental property must report its income and expenses on a Schedule E. True Joey and Susan rented their house for 2 weeks and used it for personal use for the remainder of the year. The house is considered personal/rental property. False If a divorce agreement executed specifies that a portion of the amount of an alimony payment is contingent upon the age or status of a child, that portion is considered to be a child support payment True The self-employed health insurance deduction is also available to a partner in a partnership and to a shareholder in a Subchapter S corporation who owns more than 2% of the stock in the corporation. True Distributions from Health Savings Accounts (HSAs) are subject to tax, if they are used to pay for qualified medical expenses. False Self-employed persons are allowed a for AGI deduction equal to one-half of the self-employment tax imposed True The cost of self-employed health insurance premiums are deductible above-the line at a rate of 80% of the cost. False Itemized deductions are first reported on: Schedule A. The adjusted basis of an asset is: The cost basis less any accumulated depreciation. Which of the following statements is False with respect to the standard mileage rate? The taxpayer can have an unlimited number of autos and use the mileage rate. Marion drives 20 miles a day from his first job to his second job. He worked 125 days during 2019 on both jobs. What is Marion's mileage deduction rounded to the nearest dollar assuming he uses the standard mileage rate and mileage is incurred ratably throughout the year? $1,450 Byron took a business trip from Philadelphia to Rome. He was away 16 days of which he spent 9 days on business (including two travel days) and 7 days vacationing. His expenses are as follows: Airfare $1,100 Lodging 2,240 Meals 1,840 Byron's total travel (including meals and lodging) expense deduction rounded to the nearest dollar is: $2,396 Cole purchased a car for business and personal use. In 2019, he used the car 60% for business (13,000 total use miles) and used the standard mileage rate to calculate his vehicle expenses. He also paid $1,500 in interest and $360 in county property tax on the car. What is the total business deduction related to business use of the car rounded to the nearest dollar? $5,640 Which of the following properties is not eligible for the §179 expense election when purchased? Rental real estate The standard mileage rate encompasses all of the following auto costs except for: Auto property taxes. Della purchased a warehouse on February 25, 2019, for $350,000. $45,000 of the price was for the land. What is her cost recovery deduction for 2019 rounded to the nearest dollar? $6,853 Marcus has two jobs. He works as a night auditor at the Midnight Motel. When his shift at the motel is over, he works as a short order cook at the Break-An-Egg Restaurant. On a typical day, he drives the following distances: Home to Midnight Motel 4 miles Midnight Motel to restaurant 12 miles Restaurant to home 8 miles How many miles per day would qualify as transportation expenses for tax purposes? 12 miles The following are not taxable to shareholders: Stock split Personal casualty losses in a Federally declared disaster area that result from termite damage are deductible. False Which of the following interest expenses incurred by Trent is treated as personal interest expense and, therefore, not deductible as an itemized deduction? Interest expense on personal credit cards. Which of the following types of taxes are deductible on Schedule A in 2019? Both personal property taxes and local real estate taxes. Loan fees that are not "points", or prepaid interest, are deductible as interest on Schedule A. False A property that has been rented for 120 days and used for personal use for 13 days should be categorized as: Primarily rental Taxes assessed for local benefits, such as a new sidewalk, are deductible as real property taxes. False Taxpayers must itemize their deductions to be allowed a charitable contribution deduction. True The adjusted gross income limitation on permitted casualty losses is 7.5 percent. False Taxes assessed for local benefits, such as repair of an existing sidewalk, are deductible as real property taxes. True What is generally the maximum amount of eligible home equity indebtedness on which interest is fully deductible? $ 100,000 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |