|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 4 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

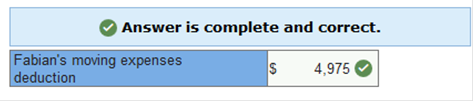

Fabian, a single account executive, was employed and resided in New Mexico. On July 1, 2017, his company transferred him to Florida. Fabian worked full time for the entire year. During 2017, he incurred and paid the following expenses related to the move:

He did not receive reimbursement for any of these expenses from his employer; his AGI for the year was $80,500. What amount can Fabian deduct as moving expenses on his 2017 return?

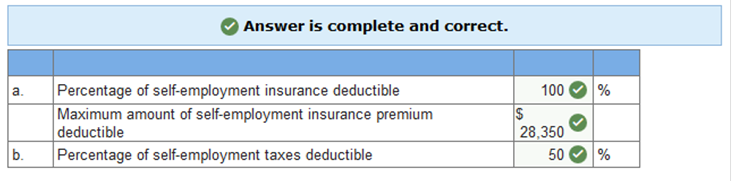

2100 + 2875 = 4,975 Juan, who is single, is a self-employed carpenter as well as an employee of Frame It, Inc. His self-employment net income is $28,350, and he received a W-2 from Frame It for wages of $20,500. He is covered by his employer’s pension plan, but his employer does not offer a health plan in which he could participate. Up to how much of his self-employed health insurance premiums could he deduct for this year, if any? How much of Juan’s self-employment taxes would be deductible?

Zach attended Champion University during 2012-2016. He lived at home and was claimed by his parents as a deduction during the entire duration of his education. He incurred education expenses of $10,000 during college of which $1,800 was paid for by scholarships. To finance his education, he borrowed $7,000 through a federal student loan program and borrowed another $3,000 from a local lending institution for educational purposes. After graduation, he married and moved with his spouse to a distant city. In 2017, he incurred $700 of interest on the federal loans and $300 on the lending institution loan. He filed a joint return with his spouse showing modified AGI of $106,000. What amount of student loan interest can Zach and his spouse deduct in 2017, if any?

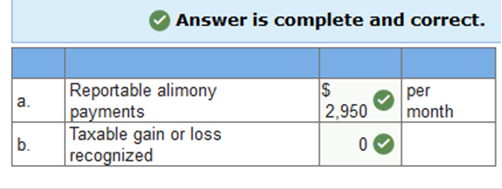

Under the terms of a divorce decree executed May 1, 2017, Ahmed transferred a house worth $540,000 to his ex-wife, Farah, and was to make alimony payments of $2,950 per month. The property has a tax basis to Ahmed of $245,000. How much of this must be reported on Farah’s tax return? Of that amount, how much is taxable gain or loss that Farah must recognize related to the transfer of the house?

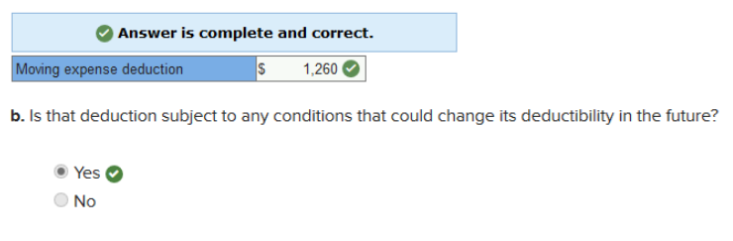

In May 2017, Regina graduated from USC with a degree in accounting and moved to Portland, OR, to look for work. Shortly after arriving in Portland, she obtained work as a staff accountant in a local CPA firm. In her move to Portland, Regina incurred the following costs: $315 in gasoline. $274 for renting a truck from UPAYME rentals. $116 for a tow trailer for her car. $101 in food. $33 in double espressos from Starbucks. $348 for motel lodging on the way to Portland. $461 for a previous plane trip to Portland to look for an apartment. $207 in temporary storage costs for her collection of crystal figurines. a. How much, if any, may Regina take as a moving expense deduction on her 2017 tax return? b. Is that deduction subject to any conditions that could change its deductibility in the future?

All of the following assets are capital assets, except: a. Personal furniture. b. A child's bicycle. c. A personal automobile. d. Used car inventory held by a car dealer. e. IBM stock. Julie, a single taxpayer, has completed her 2020 Schedule C and her net loss is $40,000. Her only other income is wages of $30,000. Julie takes the standard deduction of $12,400 in 2020. a. Calculate Julie's taxable income or loss. $_______ (Gain/Loss) b. Calculate the business and nonbusiness portions of her taxable income or loss. Business: $_____ (Gain/Loss) Nonbusiness: $______ (Gain/Loss) c. Determine Julie's 2020 NOL. a. $22,400 Loss b. Business: $10,000 Loss / Nonbusiness: $12,400 Loss c. $10,000 Yasmeen purchases stock on January 30, 2019. If she wishes to achieve a long-term holding period, what is the first date that she can sell the stock as a long-term gain? January 31, 2020 Which of the following is not classified as portfolio income for tax purposes? Net rental income from real estate partnership Which of the following types of income is passive income? Net rental income from real estate limited partnership investments Which of the following is classified as active income? Choose the answer that best answers the question. Self-employment income from a small business Nancy has active modified adjusted gross income before passive losses of $75,000. She has a loss of $5,000 on a rental property she actively manages. How much of the loss is she allowed to take against the $75,000 of other income? $5,000 Charlene has self-only coverage in a qualifying high-deductible health insurance plan. She is 57 years old and wishes to contribute the maximum amount to her HSA. How much is she allowed to contribute and deduct in 2015? $4,350 $3,350 + $1,000 = $4,350 Books purchased for courses at the campus bookstore, independent of tuition charges, are eligible expenses for the tuition and fees deduction. Related expenses for books, supplies, and equipment are qualified expenses if the school requires the payment of those items as a condition of enrollment. False Tuition, fees, books, supplies, room, board, and other necessary expenses of attendance are qualified education expenses for purposes of the student loan interest deduction. True Student loan interest is deductible only by the person who actually attended the educational institution. Only the person legally obligated to make the interest payments can take the deduction. False The cost of self-employed health insurance premiums are deductible above-the line at a rate of 80% of the cost. 100% of self-employed health insurance premiums are deductible if certain conditions are met. False Deductible moving expenses may include moving household goods and personal effects from the old residence to the new residence. Moving expenses of persons other than the taxpayer are permitted if the other persons are members of the taxpayer's household and both the old and new residences are the persons' principal place of abode. True The student loan interest deduction may be limited based on the modified AGI of the taxpayer. The deduction for interest on qualified education loans may be limited based on the modified Adjusted Gross Income of the taxpayer. There is a both a "floor" and a "ceiling" with this phase-out. True The self-employed health insurance deduction is also available to a partner in a partnership and to a shareholder in a Subchapter S corporation who owns more than 2% of the stock in the corporation. True In order to be eligible for the qualified tuition and related expense deduction, a qualifying student must be enrolled: Taxpayers must attach Form 8917 to their return when claiming this deduction. For at least one course The determination for the deduction of the self-employment tax is based upon the: net earnings of the business In 2011 through 2015, Shannon borrowed a total of $35,000 for higher education expenses on qualified education loans while supporting herself with a full-time job. In 2015, she had modified adjusted gross income of $50,000. The first year interest on the loan was $850. The amount that Shannon can claim on her tax return is: With AGI less than 65K, she is under the phase-out floor; therefore the full amount is deductible. $850.00 At the beginning of 2015, Melissa was permanently transferred from her office in New York City to New Jersey. Her office in NYC was 15 miles from her old NY home. For Melissa to meet the distance test for qualifying moving expense deductions, how many miles must the office in New Jersey be from her old home? The new job location must be at least 50 miles farther from the taxpayer's old residence than was the old job location. 65 Rick and Lenora were granted a divorce in 2014. In accordance with the decree, Rick made the following payments to Lenora in 2015: Child support payments contingent on the age of the child $4,000 Annual cash payments other than child support 6,000 How much should Lenora include in her 2015 taxable income as alimony? Child support is not considered alimony and therefore is not income to the recipient. $6000.00 Jena is a self-employed fitness trainer who had net earnings from self-employment of $23,500. She paid $525 per month for health insurance over the entire last year. Jena is entitled to a for AGI deduction for health insurance of: $6,300.00 $525 × 12 = $6,300 Self-employment tax is calculated on: Form SE Rena had the following moving expenses during 2015: Cost of packing and transporting her household goods $1,500 Lodging for travel between the old home and new home $600 Meals incurred during the trip $175 Rena moved to start a new job and met all the required tests for moving expense deductibility. What is the total amount of moving expenses that can be deducted on her 2015 return? $2,100.00 $1,500 + 600 = $2,100 In 2014, Robert, who is single, received his Bachelor's degree and started working. In 2015, he began paying interest on qualified education loans and had modified AGI of $70,000. He paid interest of $1,200 in 2015. Which of the following statements is correct? With AGI greater than 65K, but less than 80K, he is within the phase-out range; therefore a prorated amount of the total interest is deductible. $1,200.00 Self-employed persons are allowed a for AGI deduction equal to one-half of the self-employment tax imposed. True The Oroscos were granted a decree of divorce effective January 1, 2015. In accordance with the decree, César Orosco is to pay his wife $24,000 a year until their only child, Ricardo now 11, turns 18, and then the payments will decrease by $11,000 per year. For 2015, how much can César deduct as alimony? $13,000.00 24,000 – 11,000 = 13,000 Child support is not considered alimony and therefore is not deductible. ade, who is single and self-employed as a graphic artist, had net earnings from self-employment of $7,250 for the year. She paid $285 a month for health insurance premiums over the last year. Sade is entitled to a for AGI deduction for health insurance of: $3,420.00 285 × 12 = 3,420 In 2011 through 2016, Korey, who is single, borrowed a total of $25,000 for higher education expenses on qualified education loans. In 2017, while still living at home and being claimed by his parents as a dependent, he began making payments on the loan. The first year's interest on the loan was reported as $550 and his AGI for the year was less than $65,000. The amount that Korey can claim on his tax return is: 0 As a for AGI deduction, self-employed health insurance premiums are deductible at: 100% Rick is a self-employed carpenter who had net earnings from self-employment of $3,500. He paid $325 per month for health insurance over the last year. Rick is entitled to a for AGI deduction for health insurance of: $3,500 The Renfros were granted a decree of divorce in 2016. In accordance with the decree, Josh Renfro is to pay his ex-wife $24,000 a year until their only child, Evelyn, now 10, turns 18, and then the payments will decrease to $14,000 per year. For 2017, much can Josh deduct as alimony in total? $14,000 Fabian, a single account executive, was employed and resided in New Mexico. On July 1, 2017, his company transferred him to Florida. Fabian worked full-time for the entire year. During 2017, he incurred and paid the following expenses related to the move: Pre-move house hunting costs $1,500 Lodging and travel expenses (not meals) while moving 1,800 Cost of moving furniture and personal belongings 2,700 He did not receive reimbursement for any of these expenses from his employer; his AGI for the year was $85,500. What amount can Fabian deduct as moving expenses on his 2017 return? $4,500.00 2700 + 1800 = 4,500 John owns a second home in Palm Springs, CA. During the year, he rented the house for $5,000 for 42 days and used the house for 14 days during the summer. The house remained vacant during the remainder of the year. The expenses for the home included $5,000 in mortgage interest, $600 in property taxes, $900 for utilities and maintenance, and $3,500 of depreciation. What is John's deductible rental loss, before considering the passive loss limitations? $2,500 Helen, a single taxpayer, has modified adjusted gross income (before passive losses) of $124,000. During the tax year, Helen's rental house generated a loss of $15,000. Assuming Helen is actively involved in the management of the property, what is the amount of Helen's passive loss deduction from the rental house? $13,000 Which of the following is not classified as portfolio income for tax purposes? Net rental income from real estate partnership Which of the following types of income is passive income? Net rental income from real estate limited partnership investments Which of the following is classified as active income? Choose the answer that best answers the question. Self-employment income from a small business Nancy has active modified adjusted gross income before passive losses of $75,000. She has a loss of $5,000 on a rental property she actively manages. How much of the loss is she allowed to take against the $75,000 of other income? $5,000 Norm is a real estate professional with a real estate trade or business as defined in the tax law. He has $80,000 of business income and $40,000 of losses from actively managed real estate rentals. How much of the $40,000 in losses is he allowed to claim on his tax return? $40,000 Which of the following type of insurance is not deductible as self-employed health insurance? Disability insurance Which of the following is false about the self-employed health insurance deduction? The self-employed health insurance deduction is an itemized deduction. Which of the following is a false statement about health savings accounts (HSAs)? HSAs are available to any taxpayer using a health plan purchased through the state or federal exchange under the Affordable Care Act. Charlene has self-only coverage in a qualifying high-deductible health insurance plan. She is 47 years old and wishes to contribute the maximum amount to her HSA. How much is she allowed to contribute and deduct in 2016? $3,350 Lyndon, age 24, has a nonworking spouse and earns wages of $36,000 for 2016. He also received rental income of $5,000 and dividend income of $900 for the year. What is the maximum amount Lyndon can deduct for contributions to his and his wife's individual retirement accounts for the 2016 tax year? You may assume that neither taxpayer is an active participant in another qualified retirement plan. $11,000 Which of the following is true regarding real estate activities? A) Real estate activities are always passive. B) An individual investor in rental real estate can always consider their real estate activities as active businesses. C) Closely held C corporations that participate in real estate activities will always be considered active businesses. D) Real estate professionals may be allowed to consider their real estate activities as active in some circumstances. D) Real estate professionals may be allowed to consider their real estate activities as active in some circumstances. Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |