|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 13 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

William is not married,

nor does he have any dependents. He does not itemize deductions.

His taxable income for 2017 was $87,000. His AMT adjustments totaled $133,000 (with the exception of the standard deduction and personal exemption). What is William’s AMT for 2017? Compute regular tax using the tax tables. Use Appendix D. (Round your intermediate computations to the nearest whole dollar amount.) William is not married, nor does he have any dependents. He does not itemize deductions. His taxable income for 2017 was $87,000. His AMT adjustments totaled $133,000 (with the exception of the standard deduction and personal exemption). What is William's AMT for 2017? Compute regular tax using the tax tables.

Explanation

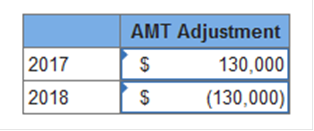

Clay Company uses the completed contract method on a contract that requires 14 months to complete. The contract is for $660,000, and has estimated costs of $363,000. At the end of 2017, $159,720 of the costs had been incurred. The contract is completed on schedule; however, total costs equal $373,000. What is the amount of AMT adjustments for 2017 and 2018? (Round completion ratio to 3 decimal places. Negative amounts should be indicated by a minus sign. Round down 2017 answer to the nearest thousand. Use this value in subsequent computations.)

Explanation

$159,720 Completed / $363,000 = 0.440 Complete

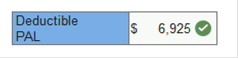

Christine died owning an interest in a passive activity property. The property had an adjusted basis of $228,500, a fair market value of $237,000, and suspended losses of $15,425. What can be deducted on her final income tax return?

Explanation The basis of the passive activity to the beneficiary would be the FMV of $237,000.

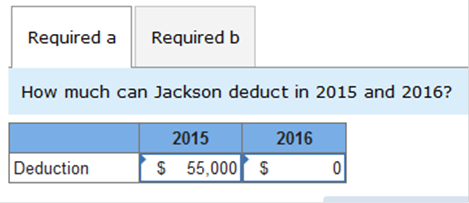

To the extent any passive activity losses exceed the step-up in basis to the beneficiary, the suspended PALs can be deducted on the decedent’s final tax return. Thus, $6,925 ($15,425 – $8,500) of the $15,425 suspended PAL would be deductible on Christine’s final tax return. Jackson invested $230,000 in a passive activity five years ago. On January 1, 2015, his at-risk amount in the activity was $55,000. His share of the income and losses in the activity were $65,000 loss in 2015, $27,000 loss in 2016, and $95,000 gain in 2017. How much can Jackson deduct in 2015 and 2016? What is his taxable income from the activity in 2017? Keep in mind the at-risk rules as well as the passive loss rules.

What is his taxable income from the activity in 2017? Keep in mind the at-risk rules as well as the passive rules.

Explanation

$55,000 is allowed under the at-risk rules. $10,000 is not allowed under the at-risk rules. Since Jackson did not have any passive income in 2015, the $55,000 loss is suspended under the PAL rules as well.

In 2017, all of the at-risk losses and suspended passive activity losses are allowed.

During the current year, Joshua worked 1,360 hours as a tax consultant and 425 hours as a real estate agent. His one other employee (his wife) worked 324 hours in the real estate business. Joshua earned $28,500 as a tax consultant, and together the couple lost $15,000 in the real estate business. How should Joshua treat the loss on his federal income tax return?

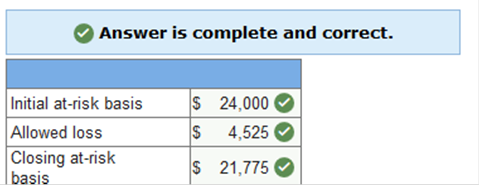

Explanation Since Joshua worked 425 hours and not less than any other individual (test 3 of the §469 regulations), then Joshua would be considered a material participant and the activity would be considered an active activity (not passive). Thus, the $15,000 loss is deductible against the tax consultant income. In 2017, Andrew contributed equipment with an adjusted basis of $24,000 and an FMV of $22,000 to Construction Limited Partnership (CLP) in return for a 3% limited partnership interest. Andrew’s share of CLP income and losses for the year were as follows:

CLP had no liabilities. What are Andrew’s initial basis, allowed losses, and ending at-risk amount?

Explanation

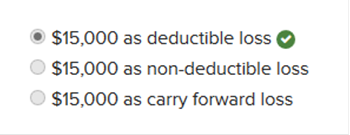

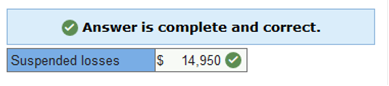

Donald has two investments in activities that are considered nonrental passive activities. He acquired Activity A six years ago, and it was profitable until the current year. He acquired Activity B in the current year. His share of the loss from Activity A in the current year is $10,500, and his share of the loss from Activity B is $4,450. What is the total of Donald’s suspended losses from these activities as of the end of the current year?

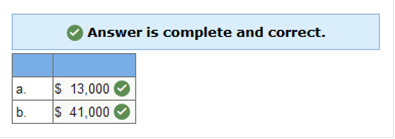

Explanation Since Donald has no passive income in the current year, the $14,950 of PAL would be suspended. Hunter has a $54,000 loss from an investment in a partnership in which he does not participate. His basis in the interest is $41,000. How much of the loss is disallowed by the at-risk rules? How much of the loss is disallowed by the passive loss rules?

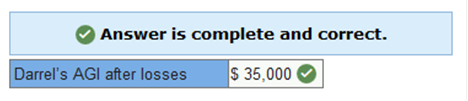

Explanation Since he has a $41,000 at-risk basis before the loss, $41,000 of the loss would be allowed and $13,000 suspended under the at-risk rules. Assuming Hunter has no other passive income from other sources, the entire $41,000 in losses would be disallowed under the PAL rules. The loss makes it through the at-risk rules but not the PAL rules. Darrell acquired an activity eight years ago. The loss from it in the current year was $36,000. The activity involves residential rental real estate in which he is an active participant. Calculate Darrell’s AGI after considering that Darrell’s AGI was $60,000 before including any potential loss.

Explanation If Darrell’s AGI was $60,000, then he would be eligible for the real estate offset up to $25,000. Thus, $25,000 of the PAL would be allowed and reduce AGI to $35,000. Lucy has AGI of $119,000 before considering losses from some rental real estate she owns (she actively participates). She had the following losses from her rental property:

How much of the losses can Lucy deduct? If Lucy’s AGI before the losses was $81,000, how much of the losses can she deduct?

Explanation a. She is allowed some of the $25,000 offset, but some of the losses do phase-out. She loses ($119,000 – $100,000)(.5) = $9,500. $15,500 ($25,000 – $9,500) of the $33,000 loss is allowed. Property 1: $15,500 × ($24,500/$33,000) = $11,508 allowed; $12,992 suspended Property 2: $15,500 × ($8,500/$33,000) = $3,992 allowed; $4,508 suspended b. $25,000 of the $33,000 loss is allowed. Property 1: $25,000 × ($24,500/$33,000) = $18,561 allowed; $5,939 suspended Property 2: $25,000 × ($8,500/$33,000) = $6,439 allowed; $2,061 suspended The components of the general business credit include all of the following except: a. Credit for employer-provided child care. b. Disabled access credit. c. Research activities credit. d. Tax credit for rehabilitation expenditures. e. All of these are components of the general business credit. Which of the following correctly describes the tax credit for rehabilitation expenditures? a. The cost of enlarging any existing business building is a qualifying expenditure. b. The cost of facilities related to the building (e.g., a parking lot) is a qualifying expenditure. c. No recapture provisions apply. d. No credit is allowed for the rehabilitation of personal use property. e. None of these. Several years ago, Sarah purchased a structure for $150,000 that was originally placed in service in 1929. In the current year, she incurred qualifying rehabilitation expenditures of $200,000. The amount of the tax credit for rehabilitation expenditures, and the amount by which the building's basis for cost recovery would increase as a result of the rehabilitation expenditures are the following amounts: a. $20,000 credit, $180,000 basis. b. $20,000 credit, $200,000 basis. c. $20,000 credit, $350,000 basis. d. $40,000 credit, $160,000 basis. e. None of these. Several years ago, Tom purchased a structure for $300,000 that was originally placed in service in 1929. Three and one-half years ago he incurred qualifying rehabilitation expenditures of $600,000. In the current year, Tom sold the property in a taxable transaction. Calculate the amount of the recapture of the tax credit for rehabilitation expenditures. a. $0 b. $24,000 c. $36,000 d. $48,000 e. None of these Cardinal Corporation hires two persons certified to be eligible employees for the work opportunity tax credit under the general rules (e.g., food stamp recipients), each of whom is paid $9,000 during the year. As a result of this event, Cardinal Corporation may claim a work opportunity credit of: a. $1,440. b. $2,880. c. $4,800. d. $7,200. e. None of these. Black Company paid wages of $180,000, of which $40,000 was qualified wages for the work opportunity tax credit under the general rules. Black Company's deduction for wages for the year is: a. $140,000. b. $164,000. c. $166,000. d. $180,000. e. None of these. Which of the following best describes the treatment applicable to unused business credits? a. Unused amounts are carried forward indefinitely. b. Unused amounts are first carried back one year and then forward for 20 years. c. Unused amounts are first carried back one year and then forward for 10 years. d. Unused amounts are first carried back three years and then carried forward for 15 years. e. None of these. Molly has generated general business credits over the years that have not been utilized. The amounts generated and not utilized follow: 2010 $ 2,500 2011 7,500 2012 5,000 2013 4,000 In the current year, 2014, her business generates an additional $15,000 general business credit. In 2014, based on her tax liability before credits, she can utilize a general business credit of up to $20,000. After utilizing the carryforwards and the current year credits, how much of the general business credit generated in 2014 is available for future years? a. $0. b. $1,000. c. $14,000. d. $15,000. e. None of these. Ahmad is considering making a $10,000 investment in a venture which its promoter promises will generate immediate tax benefits for him. Ahmad, who normally itemizes his deductions, is in the 28% marginal tax bracket. If the investment is of a type where the taxpayer may claim either a tax credit of 25% of the amount of the expenditure or an itemized deduction for the amount of the investment, what treatment normally would be most beneficial to Ahmad and by how much will Ahmad's tax liability decline because of the investment? a. $0, take neither the itemized deduction nor the tax credit. b. $2,500, take the tax credit. c. $2,800, take the itemized deduction. d. Both options produce the same benefit. e. None of these. Refundable tax credits include the: a. Foreign tax credit. b. Tax credit for rehabilitation expenses. c. Credit for certain retirement plan contributions. d. Earned income credit. e. None of these. Roger is considering making a $6,000 investment in a venture that its promoter promises will generate immediate tax benefits for him. Roger, who does not anticipate itemizing his deductions, is in the 30% marginal income tax bracket. If the investment is of a type that produces a tax credit of 40% of the amount of the expenditure, by how much will Roger's tax liability decline because of the investment? a. $0 b. $1,800 c. $2,200 d. $2,400 e. None of these Green Company, in the renovation of its building, incurs $9,000 of expenditures that qualify for the disabled access credit. The disabled access credit is: a. $8,750. b. $4,500. c. $4,375. d. $4,250. e. None of these. Amber is in the process this year of renovating the office building (originally placed in service in 1976) used by her business. Because of current Federal Regulations that require the structure to be accessible to handicapped individuals, she incurs an additional $11,000 for various features, such as ramps and widened doorways, to make her office building more accessible. The $11,000 incurred will produce a disabled access credit of what amount? a. $0 b. $5,000 c. $5,125 d. $5,500 e. None of these Paul reported the following itemized deductions on his 2021 tax return. His AGI for 2021 was $65,000. The mortgage interest is all qualified mortgage interest to purchase his personal residence. For AMT, compute his total adjustment for itemized deductions. Medical expenses (after the 7.5% of AGI floor) $ 6,000 State income taxes 3,600 Home mortgage interest 11,500 Charitable contributions 3,200 a. $ 0. b. $ 3,600. c. $ 9,600. d. $24,300. After computing all tax preferences and AMT adjustments, Phillip and his wife Carmin have AMTI of $1,210,000. If Phillip and Carmin file a joint tax return, what exemption amount can they claim for AMT for 2021? a. $ 0. b. $73,900 c. $73,600 d. $114,600 114,600 - [25% (1,210,000 - 1,047,200)] Harry and Wilma are married and file a joint income tax return. On their tax return, they report $44,000 of adjusted gross income ($20,000 salary earned by Harry and $24,000 salary earned by Wilma) and claim two exemptions for their dependent children. During the year, they pay the following amounts to care for their 4-year old son and 6- year old daughter while they work. ABC Day Care Center $3,200 Blue Ridge Housekeeping Services 2,000 Mrs. Mason (Harry's mother) 1,000 Harry and Wilma may claim a credit for child and dependent care expenses of: a. $840. b. $1,040. c. $1,200. d. $1,240. e. None of these. Kevin and Sue have two children, ages 8 and 14. They spend $6,200 per year on eligible employment related expenses for the care of their children after school. Kevin earned a salary of $20,000 and Sue earned a salary of $18,000. What is the amount of the credit for child and dependent care expenses? a. $690 b. $713 c. $1,380 d. $1,426 e. None of these Which of the following correctly reflects current rules regarding estimated tax payments for individuals? a. Employees are not subject to the estimated tax payment provisions. b. Any penalty imposed for underpayment is deductible for income tax purposes. c. Married taxpayers may not make joint estimated tax payments unless they file a joint income tax return. d. No quarterly payments are required if the taxpayer's estimated tax is under $1,000. e. None of these. D Carter, an unmarried individual, had an AGI of $180,000 in the current year before any other above-the-line deductions. He incurred a loss of $30,000 from rental real estate in which he actively participated. What amount of loss, if any, may be used in the current year as an offset against Carter's active or portfolio income? A. $0 B. $12,500 C. $25,000 D. $30,000 During the current year, Eleanor earns $120,000 in wages as an employee of an accounting firm. She also earns $13,000 in gross income from an outside consulting service she operates. Deductible expenses paid in connection with the consulting service amount to $3,000. Eleanor also has a recognized long-term capital gain of $1,000 from the sale of a stock investment. She must pay a self-employment tax on: a. $0. b. $10,000. c. $13,000. d. $14,000. e. None of these. Pat generated self-employment income in 2014 of $76,000. The self-employment tax is: a. $0. b. $5,369.23. c. $10,738.46. d. $11,628.00. e. None of these. The ceiling amounts and percentages for 2014 for the two portions of the self-employment tax are: Social Security portion Medicare portion a. $113,700; 12.4% Unlimited; 2.9% b. $113,700; 15.3% Unlimited; 2.9% c. $117,000; 12.4% Unlimited; 2.9% d. $117,000; 2.9% Unlimited; 13.3% e. None of these. The 2016 FICA employee withholding rate is A. 6.75% B. 7.25% C. 7.5% D. 7.65% MSC, Inc. is a closely held C corporation that manufactures boilers. The company has been in business for over 45 years. MSC has active income this year of $250,000 and no passive or portfolio income. The company also leases equipment that generates passive losses of $120,000 per year. How much of the passive loss can the company use this year? A. $120,000 B. $100,000 C. $0 D. $25,000 Which of the following statements concerning the credit for child and dependent care expenses is not correct? a. A taxpayer is not allowed both an exclusion from income on the same amount. b. A taxpayer is not allowed both a deduction as a medical expenses on the same amount. c. If a taxpayer's adjusted gross income exceeds $43,000, the rate expenses is 20%. d. If a taxpayer's adjusted gross income exceeds $15,000 but is not over $17,000, the rate for the credit for child and dependent care expenses is 35%. e. All of these are correct. In 2016, Ellen and Paul are married and had the following deductions: $6,000 mortgage interest, $2,000 real estate taxes, $2,000 state income tax, and medical expenses of $2,000. Assuming Ellen and Paul file a joint return, had an adjusted gross income of $50,000 and are both age 25, which of the following is CORRECT? A. Ellen and Paul should take a standard deduction of $12,600. B. Ellen and Paul should take a standard deduction of $9,300. C. Ellen and Paul should take a standard deduction of $12,000. D. Ellen and Paul should take a standard deduction of $10,000. Margie, a single taxpayer, owned and used her home as a principal residence for 18 months. She then sold her home because of a new job in another city, realizing a gain on the scale of $300,000. What would Margie's reportable gain be? A. $0 B. $112,500 C. $187,500 D. $300,000 During the current tax year, Jim has $10,000 of passive income from a publicly traded limited partnership. He also has a nonpublicly traded limited partnership that will generate a $10,000 passive loss. How much of this passive loss, if any, is deductible by Jim during the current tax year? A) $1,000 B) $6,500 C) $0 D) $10,000 Jim has the following items from four investments: Passive income from a publicly traded limited partnership$16,000Passive loss from a publicly traded limited partnership$ (8,500) Passive income from a non-publicly traded limited partnership $13,000Passive loss from a non-publicly traded limited partnership$(20,000) What is the total amount of passive losses that may be deducted during the current year? A) $13,000 B) $29,000 C) $20,000 D) $28,500 Hadley has a 33% marginal income tax rate, and she would likely to invest in State of Texas bonds. If similar taxable investments yield 10%, what must Hadley earn on the bonds to make sure the investment is worthwhile? A. 5% B. 6.7% C. 10% D. 15.6% Jermaine and Kesha are married, file a joint tax return, have AGI of $82,500, and have two children. Devona is beginning her freshman year at State University during Fall 2014, and Arethia is beginning her senior year at Northeast University during Fall 2014 after having completed her junior year during the spring of that year. Both Devona and Arethia are claimed as dependents on their parents' tax return. Devona's qualifying tuition expenses and fees total $4,000 for the fall semester, while Arethia's qualifying tuition expenses and fees total $6,200 for each semester during 2014. Full payment is made for the tuition and related expenses for both children during each semester. The American Opportunity credit available to Jermaine and Kesha for 2014 is: a. $2,500. b. $3,000. c. $5,000. d. $6,000. e. None of these. You are a CFP® professional and are meeting with your client Brenda to monitor her ongoing financial status. Brenda owns a vacation home in New Mexico. She is now renting the property to others for the entire year except for 10 days during the summer when she and her family used it for their vacation. The gross rental income that Brenda received is $65,000. The expenses for the home for both the rental period and her personal use total $5,000. Brenda would like you to explain how this will change her income tax situation, in particular, how much of the rental expenses are deductible. After reviewing the documents she sent to you prior to the meeting, you have an answer for Brenda. How much of a deduction for rental expenses can Brenda take on her tax return? A) $3,411 B) $5,000 C) $4,863 D) $4,721 355 / 365 x 5,000 = 4,863.013699 During the current year, Kate received salary of $50,000 dividends of $3,000, tax-exempt interest of $1,000, and a gift of $20,000 from her parents. What amount will Kate report as a gross income on her tax return? A. $50,000 B. $53,000 C. $54,000 D. $74,000 How much of the medical expense will be deductible? A. $0 B. $500 C. $7,500 D. $8,000 Paula purchased an interest in a master limited partnership (MLP) that produced a loss of $7,000 this year. She also purchased a real estate limited partnership (RELP) that generated $10,000 of passive income this year. How much, if any, of the passive loss from the MLP could be used to offset Paula's income from the RELP in the current year? A) $0 B) $3,500 C) $7,000 D) $3,000 Paula purchased an interest in an MLP with a current loss of $7,000. If she purchased a RELP with $10,000 of passive income generated this year, how much, if any, of the passive loss from the MLP could be used to offset Paula's income in the current year? A. $0 B. $3,000 C. $7,000 D. $10,000 In March 2014, Gray Corporation hired two individuals, both of whom were certified as long-term recipients of family assistance benefits. Each employee was paid $11,000 during 2014. Only one of the individuals continued to work for Gray Corporation in 2015, earning $9,000 during the year. No additional workers were hired in 2015. Gray Corporation's work opportunity tax credit amounts for 2014 and 2015 are: a. $4,000 in 2014, $4,000 in 2015. b. $8,000 in 2014, $4,500 in 2015. c. $8,000 in 2014, $5,000 in 2015. d. $8,000 in 2014, $9,000 in 2015. e. None of these. Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project2

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |