|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 12 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

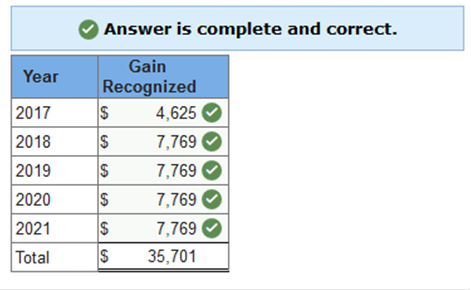

Pedro sells investment

land on September 1, 2017. Information pertaining to the sale follows:

Each installment payment is due on September 1 of 2018, 2019, 2020, and 2021 (ignore interest). Determine the tax consequences in 2017, 2018, 2019, 2020, and 2021. (Do not round intermediate calculations. Round your final answers to nearest whole dollar value.)

Explanation

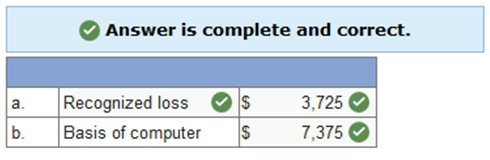

Kim owns equipment that is used exclusively in her business. The equipment has an adjusted basis of $8,950 (FMV $5,225). Kim transfers the equipment and $2,150 cash to David for a computer (also used for business purposes) that has a FMV of $7,375. What is Kim’s recognized gain or loss on the exchange? What is Kim’s adjusted basis in the computer?

Explanation Equipment – treated as a sale because they are not like-kind assets. a.

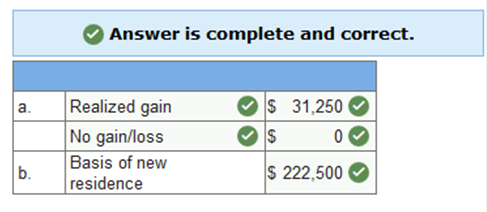

Basis is the “cost” of the computer. $5,225 FMV of equipment + $2,150 cash = $7,375 Virginia is an accountant for a global CPA firm. She is being temporarily transferred from the Raleigh, North Carolina, office to Tokyo. She will leave Raleigh on October 7, 2017, and will be out of the country for four years. She sells her personal residence on September 30, 2017, for $236,250 (her adjusted basis is $205,000). Upon her return to the United States in 2021, she purchases a new residence in Los Angeles for $222,500, where she will continue working for the same firm. (If no gain or loss is recognized, select "No gain/loss".) What are Virginia’s realized and recognized gain or loss? What is Virginia’s basis in the new residence?

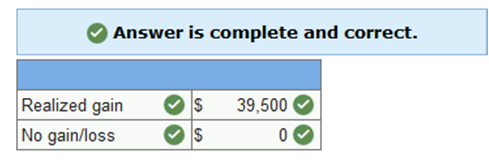

Explanation Realized gain $236,250 – $205,000 = $31,250. Recognized gain $0 §121 exclusion. Cost $222,500 Reid’s personal residence is condemned on September 12, 2017, as part of a plan to add two lanes to the existing highway. His adjusted basis is $260,000. He receives condemnation proceeds of $299,500 on September 30, 2017. He purchases another personal residence for $282,500 on October 15, 2017. What are Reid’s realized and recognized gain or loss? (If no gain or loss is recognized, select "No gain/loss".)

Explanation

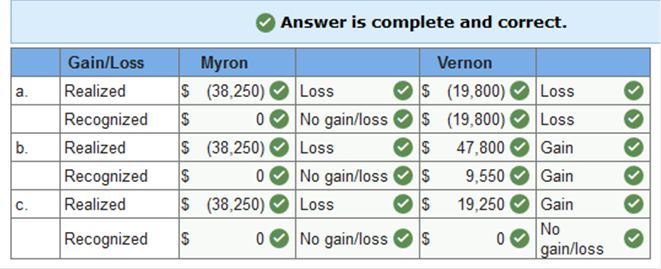

Replacement for $282,500 would normally result in a $17,000 gain recognized (proceeds in excess of replacement cost). However, since this was a personal residence, the $17,000 gain is not recognized due to the exclusion of gain for personal residences (IRC §121). On January 1, 2017, Myron sells stock that has a $47,300 FMV on the date of the sale (basis $85,550) to his son Vernon. On October 21, 2017, Vernon sells the stock to an unrelated party. In each of the following, determine the tax consequences of these transactions to Myron and Vernon: (If no gain or loss is recognized, select "No gain/loss".) Vernon sells the stock for $27,500. Vernon sells the stock for $95,100. Vernon sells the stock for $66,550.

Explanation Myron’s $38,250 loss would be disallowed under the related party rules. Vernon would recognize a $19,800 loss. Myron’s $38,250 loss would not be used and lost forever. Myron’s $38,250 loss would be disallowed under the related party rules. Vernon would recognize a $9,550 gain. The gain is actually $47,800 on the sale but it can be reduced by the $38,250 disallowed loss on the sale by Myron. Myron’s $38,250 loss would be disallowed under the related party rules. Vernon would not recognize any gain on the sale. The $19,250 gain is reduced by Myron’s disallowed loss. Myron’s additional loss of $19,000 would be lost forever. Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |