|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Personal Income Tax: Homework Chapter 11 Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

Under what circumstances

is it advantageous for a taxpayer to make a nondeductible contribution to a

traditional IRA

rather than a contribution to a Roth IRA?

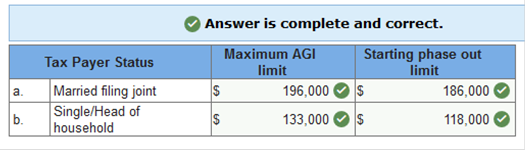

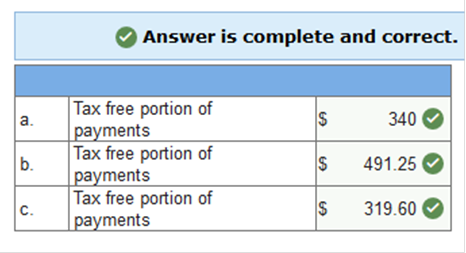

Explanation In 2017, if a taxpayer has AGI in excess of $196,000 ($133,000 for single taxpayers or head of household), a contribution to a Roth IRA is prohibited (the contribution amount begins to phase out at $186,000 for married taxpayers and at $118,000 for those who are single or head of household). Such taxpayers can still make a nondeductible contribution to a traditional IRA. Determine the tax-free amount of the monthly payment in each of the following instances. Use the life expectancy tables. Use Table I, Table III and Table V. Person A is age 63 and purchased an annuity for $88,000. The annuity pays $1,000 per month for life. (Round exclusion percentage computation to one decimal place.) Person B is 72 and purchased an annuity for $86,000. The annuity pays $1,250 per month for life. (Round exclusion percentage computation to one decimal place. Round your final answer to 2 decimal places.) Person C is 65 and purchased an annuity for $46,000 that pays a monthly payment of $850 for 12 years. (Round exclusion percentage computation to one decimal place. Round your final answer to 2 decimal places.)

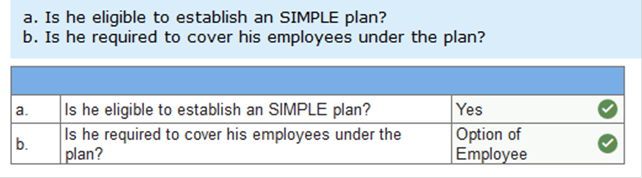

Explanation Use Table V in the Appendix for each case. The exclusion percentage is the cost of the contract divided by the expected return from the contract. The excluded amount is equal to the payment received multiplied by the exclusion percentage. In case (a), the expected return is 21.6 years × 12 × $1,000 = $259,200. The exclusion percentage is $88,000 / $259,200 = 34.0% (rounded). Thus, $340 of each payment is tax-free. In case (b), the expected return is 14.6 years × 12 × $1,250 = $219,000. The exclusion percentage is $86,000 / $219,000 = 39.3% (rounded). Thus, $491.25 of each payment is tax-free. In case (c), the expected return is $850 per month for 144 months (12 years × 12), or $122,400. The exclusion percentage is $46,000 / $122,400 = 37.6% (rounded). Thus, $319.60 of each payment is tax-free. Ken is a self-employed architect in a small firm with four employees: himself, his office assistant, and two drafters, all of whom have worked for Ken full-time for the last four years. The office assistant earns $32,000 per year and each drafter earns $44,000. Ken’s net earnings from self-employment (after deducting all expenses and one-half of self-employment taxes) are $314,000. Ken is considering whether to establish an SIMPLE plan and has a few questions. Is he eligible to establish an SIMPLE plan? Is he required to cover his employees under the plan? If his employees must be covered, what is the maximum amount that can be contributed on their behalf? If the employees are not covered, what is the maximum amount Ken can contribute for himself? If Ken is required to contribute for his employees and chooses to contribute the maximum amount what is the maximum amount Ken can contribute for himself? (Hint: Calculate the employee amounts first.) Ignore any changes in Ken’s self-employment tax.

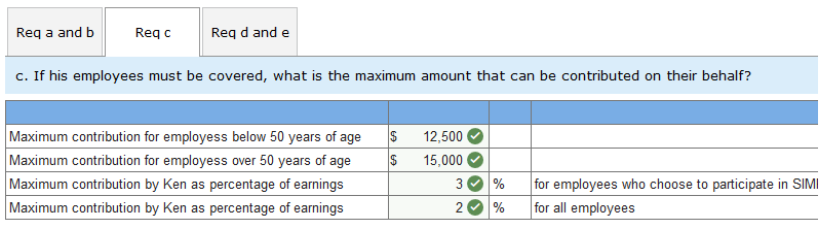

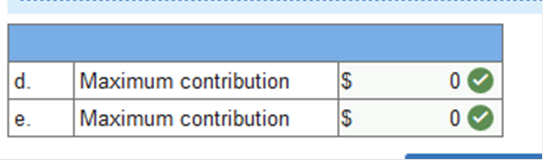

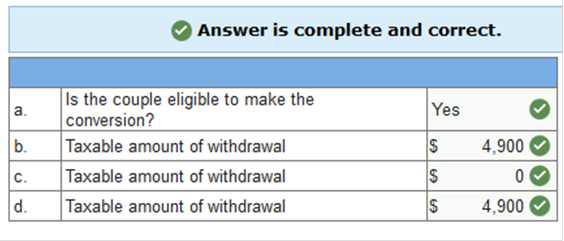

Explanation Ken is eligible to establish a SIMPLE plan for his employees. Employees can choose to participate, but are not required to do so. The maximum amount employees can contribute is $12,500 each based on an established percentage of their compensation or a fixed dollar amount. Employees over 50 years old can contribute another $2,500 if they choose. Ken would be required to make a 3% contribution for those employees who choose to participate or contribute 2% for all employees. Ken is not eligible to cover himself in the plan since he is not an employee. Ken is not eligible to cover himself in the plan since he is not an employee. Pablo and his wife Bernita are both age 52. Their combined AGI is $93,000. Neither is a participant in an employer-sponsored retirement plan. They have been contributing to a traditional IRA for many years and have built up an IRA balance of $120,000. They are considering rolling the traditional IRA into a Roth IRA. Is the couple eligible to make the conversion? Assume that the couple does not make the conversion but, instead, establishes a separate Roth IRA in the current year and properly contributes $2,150 per year for four years, at which point the balance in the Roth is $21,000 (contributions plus investment earnings). At the end of four years, they withdraw $13,500 to pay for an addition to their house. What is the amount of withdrawal that is taxable, if any? Assume same facts as in requirement b, except that they instead withdrew only $6,000. What is the amount of withdrawal that is taxable? What is the taxable amount if the $13,500 withdrawal is used to pay qualified education expenses for their daughter who is attending college?

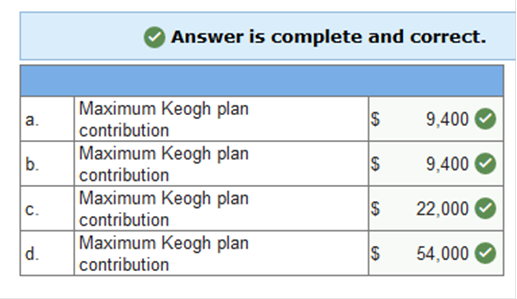

Explanation Yes. Taxpayers can roll a traditional IRA to a Roth IRA at any time. The amount rolled will be included in their gross income in the year converted. In 2017, there is no AGI limitation that might prohibit conversion. If a Roth has not been in existence for at least five years, a withdrawal is taxable if it exceeds contributions made to the Roth. Withdrawals are deemed to first come from contributions and then from earnings. In this case, the Roth has been in existence for only four years and the $13,500 withdrawal exceeds accumulated contributions of $8,600. Thus, the withdrawal is taxable to the extent of the $4,900 excess. Yes. None of the withdrawal is taxable because it does not exceed accumulated contributions. $4,900 of the withdrawal will continue to be taxable. A withdrawal of earnings within the first five years is taxable except in very limited circumstances. Education expenses are not an exception. Determine the maximum contribution that can be made to a Keogh plan in each of the following cases. In all instances, the individual is self-employed, and the self-employment tax reduction has already been taken. Self-employment income of $47,000. Self-employment income of $47,000 and wage income of $30,500. Self-employment income of $110,000. Self-employment income of $291,000.

Explanation In all cases, the maximum Keogh contribution is limited to the lesser of $54,000 or 25% of earned income from self-employment (limited to $270,000) after the Keogh contribution. The amount of self-employment income after the Keogh contribution can be determined by the formula: x = [SE income before Keogh – .25x] The amount of self-employment income after the Keogh contribution is $37,600. Thus, the maximum Keogh contribution is $9,400 (the lesser of $54,000 or 25% of $37,600). The answer to part (b) is the same as part (a). The wage income of $30,500 does not affect the calculations since it is not income from self-employment. The amount of self-employment income after the Keogh contribution is $88,000. Thus, the maximum Keogh contribution is $22,000 (the lesser of $54,000 or 25% of $88,000). Here, self-employment income exceeds the $270,000 maximum. Thus, the amount of allowed self-employment income after the Keogh contribution is $216,000 (based on the $270,000 maximum, not the $291,000 earnings from self-employment). The maximum Keogh contribution is $54,000 (the lesser of $54,000 or 25% of $216,000). Homework 01 02 03 04 05 06 07 08 09 10 11 12 13 | Exam 1 2 3 4 5 6 7 8 9 10 11 12 13 | Unit Test Final Exam 1 2 | Final Project

|

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |