|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

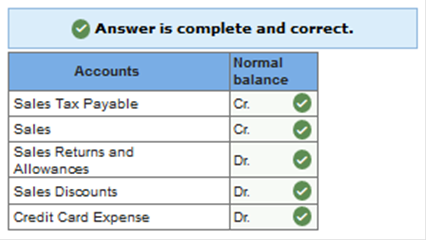

Homework Chapter 01 02 03 04 05 06 07 08 09 10 11 12 13 Test 01 02 03 04 05 06 07 08 09 10 11 12 13 Final Exam 01 02 Project Office Accounting: Homework Chapter 7 General Questions & Answers Exercise 7.1 Normal balances. LO 7-1 Identify the normal balance of the following accounts. Use “Dr” for debit or “Cr” for credit.

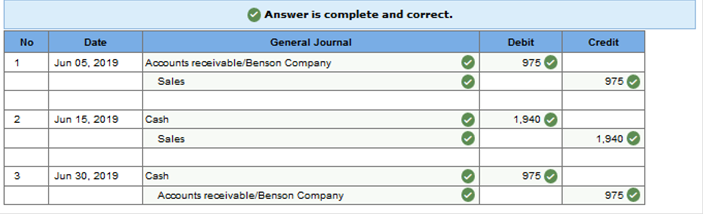

Exercise 7.2 Recording sales made for cash and on account. LO 7-1 Tsang Corporation operates in a state with no sales tax. Record the following transactions in a general journal:

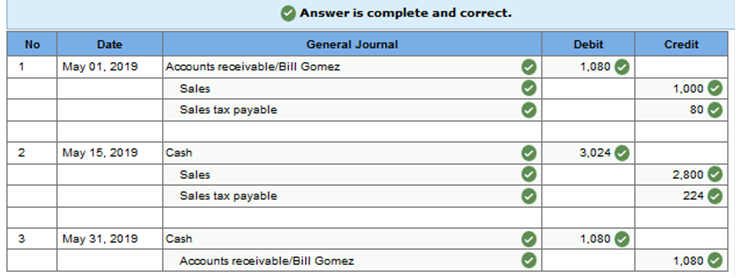

Exercise 7.3 Recording sales made for cash and on account, with 8 percent sales tax. LO 7-1 The following transactions took place at Five Flags Amusement Park during May. Five Flags Amusement Park must charge 8 percent sales tax on all sales:

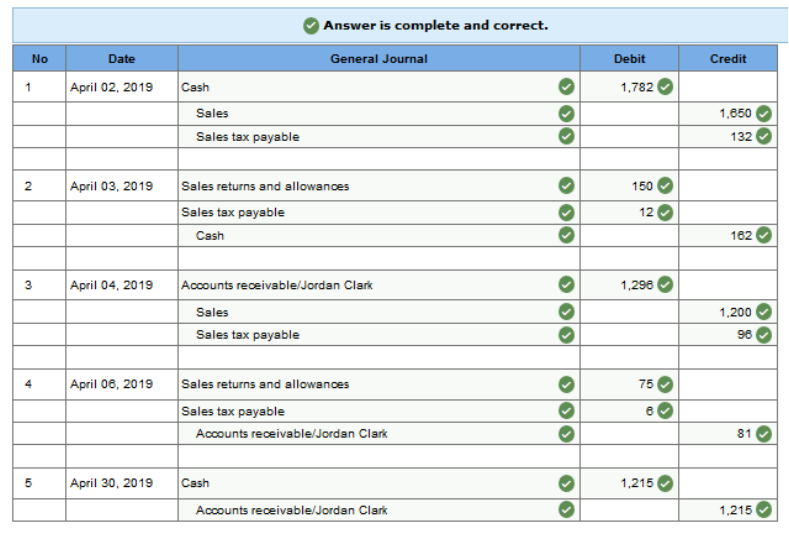

Exercise 7.4 Recording sales made for cash and on account, with 8 percent sales tax, and sales returns. LO 7-1 Record the following transactions of Fashion Park in a general journal. Fashion Park must charge 8 percent sales tax on all sales.

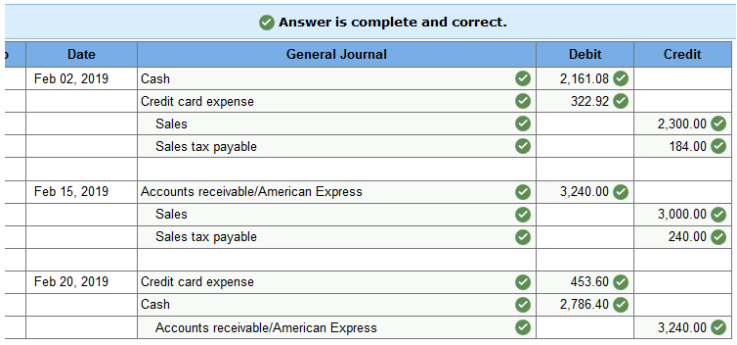

Exercise 7.5 Recording sales made with bank credit cards and American Express, with 8 percent sales tax. LO 7-1 Record the following transactions of Lisa’s Fashion Boutique in a general journal. Lisa's Fashion Boutique operates in a state with 8% sales tax. (Round your intermediate calculations and final answers to 2 decimal places):

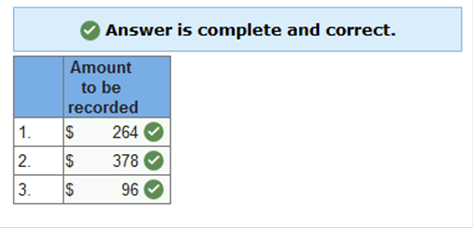

Exercise 7.6 Computing a trade discount. LO 7-2 Vicente Company made sales using the following list prices and trade discounts. What amount should be recorded for each sale? List price of $440 and trade discount of 40 percent. List price of $540 and trade discount of 30 percent. List price of $120 and trade discount of 20 percent.

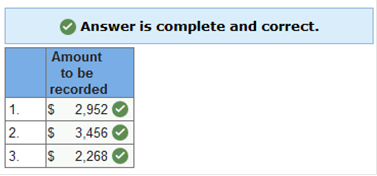

Exercise 7.7 Computing a series of trade discounts. LO 7-2 Main Street Distributors, a wholesale firm, made sales using the following list prices and trade discounts. What amount should be recorded for each sale? List price of $4,100 and trade discounts of 20 percent and 10 percent. List price of $4,800 and trade discounts of 20 percent and 10 percent. List price of $3,150 and trade discounts of 20 percent and 10 percent.

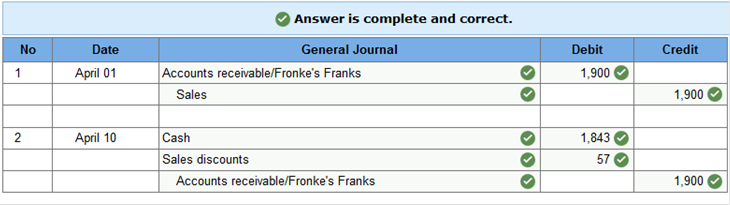

Exercise 7.8 Recording a sale made on account, with a sales discount. LO 7-3 On April 1, Moloney Meat Distributors sold merchandise on account to Fronke’s Franks for $1,900 on Invoice 1001, terms 3/10, n/30. Payment was received in full from Fronke’s Franks, less discount, on April 10. Required: Record the transactions on April 1 and April 10.

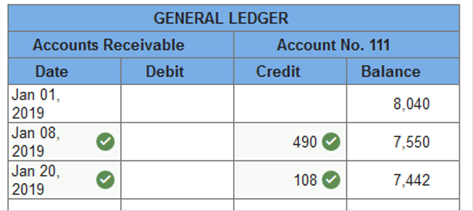

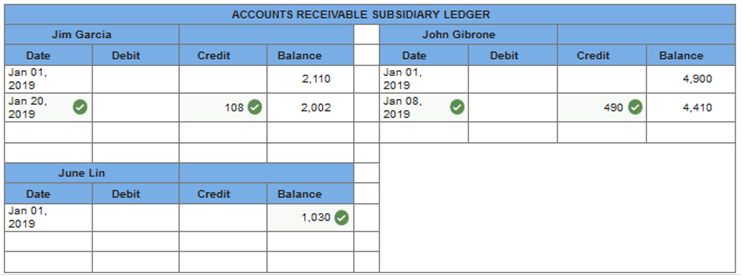

Exercise 7.9 Posting to the general ledger and the accounts receivable ledger. LO 7-4 Post the entries in the general journal below to the Accounts Receivable account in the general ledger and to the appropriate accounts in the accounts receivable ledger for Calderone Company. Assume the following account balances at January 1, 2019:

General Ledger Post the entries in the general journal above to the accounts receivable account in the general ledger for Calderone Company.

AR Ledgers Post the entries in the general journal above to the appropriate accounts in the accounts receivable ledger for Calderone Company.

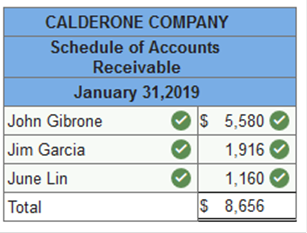

Exercise 7.10 Preparing a schedule of accounts receivable. LO 7-5 Post the entries in the general journal below to the Accounts Receivable account in the general ledger and to the appropriate accounts in the accounts receivable ledger for Calderone Company. Assume the following account balances at January 1, 2019:

Prepare a schedule of accounts receivable for Calderone Company at January 31, 2019. Should the total of your accounts receivable schedule agree with the balance of the Accounts Receivable account in the general ledger at January 31, 2019? Required 1 Prepare a schedule of accounts receivable for Calderone Company at January 31, 2019.

Required 2 Should the total of your accounts receivable schedule agree with the balance of the Accounts Receivable account in the general ledger at January 31, 2019?

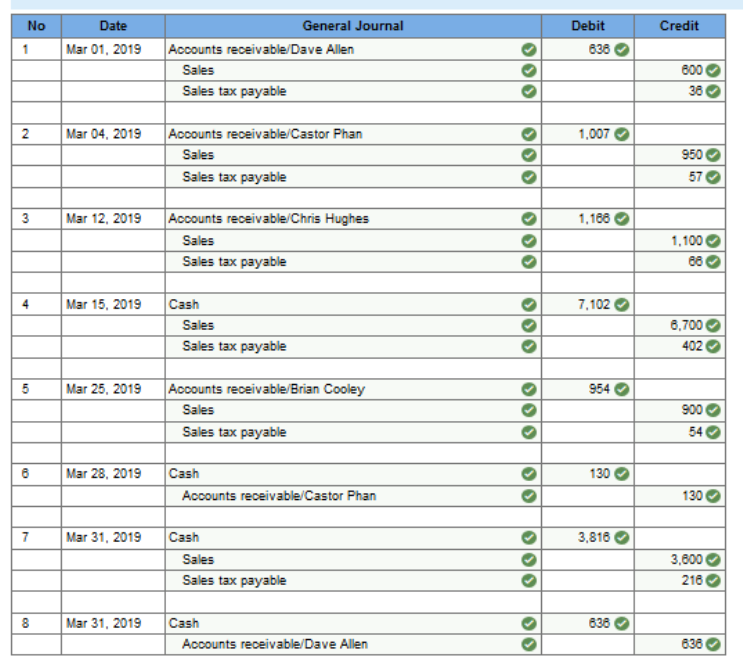

The Appliance Store began operations March 1, 2019. The firm sells its merchandise for cash and on open account. Sales are subject to a 6 percent sales tax. During March, The Appliance Store engaged in the following transactions:

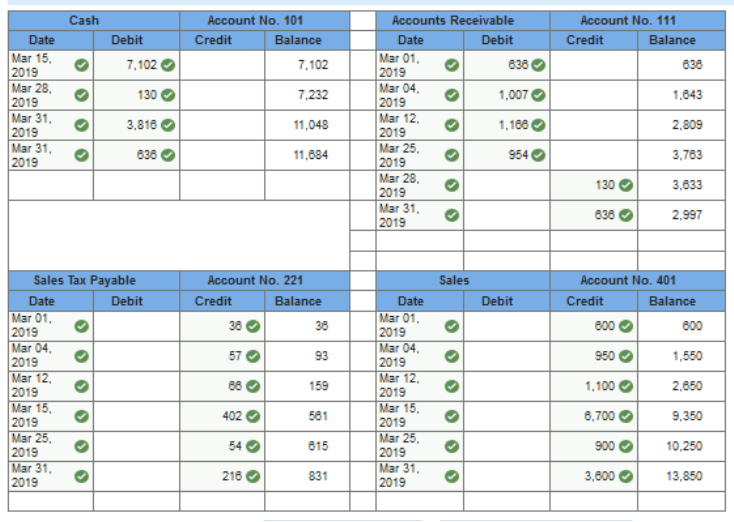

Required: Record the transactions in a general journal. Post the entries from the general journal to the appropriate general ledger accounts.

Analyze: What were the total cash receipts during March?

Explanation 2.

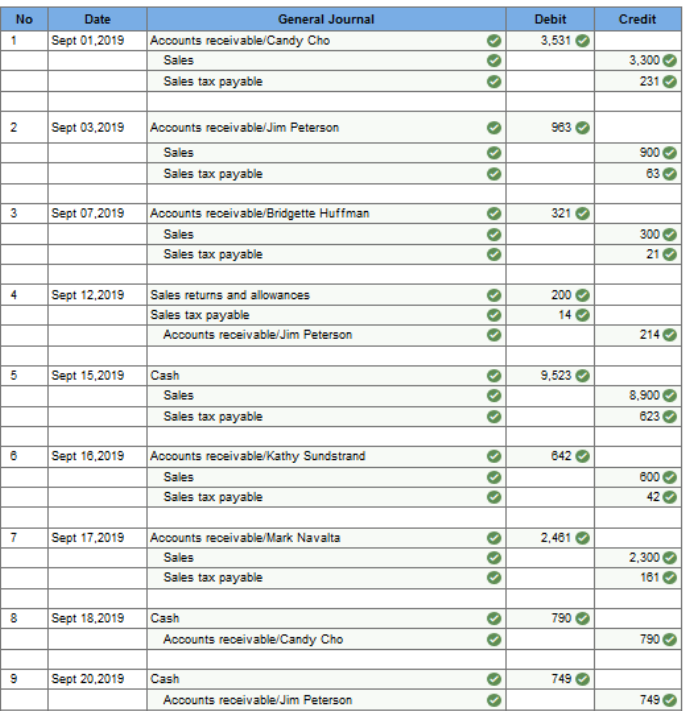

Problem 7.2A Recording sales, sales returns, and cash receipts for a retail store. LO 7-1 Exceptional Electronics began operations September 1, 2019. The firm sells its merchandise for cash and on open account. Sales are subject to a 7 percent sales tax. During September, Exceptional Electronics engaged in the following transactions:

Required: Record the transactions in a general journal. Analyze: What portion of the sales during September were for entertainment items? Assume the cash sales transactions are for non-entertainment items. (Hint: Do not forget to reduce sales by any sales returns or allowances.)

Explanation

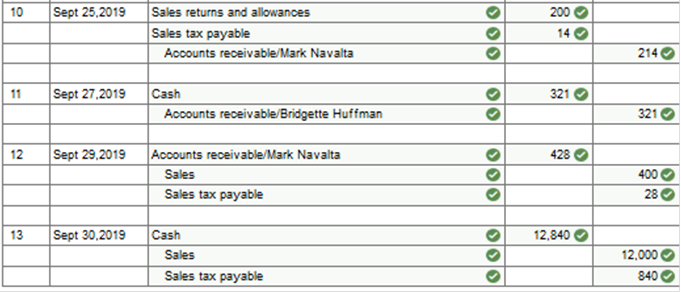

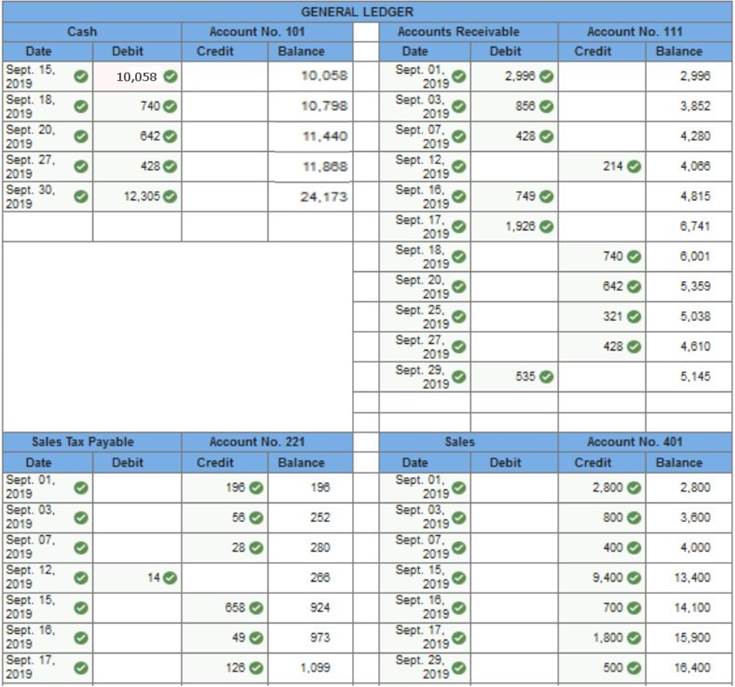

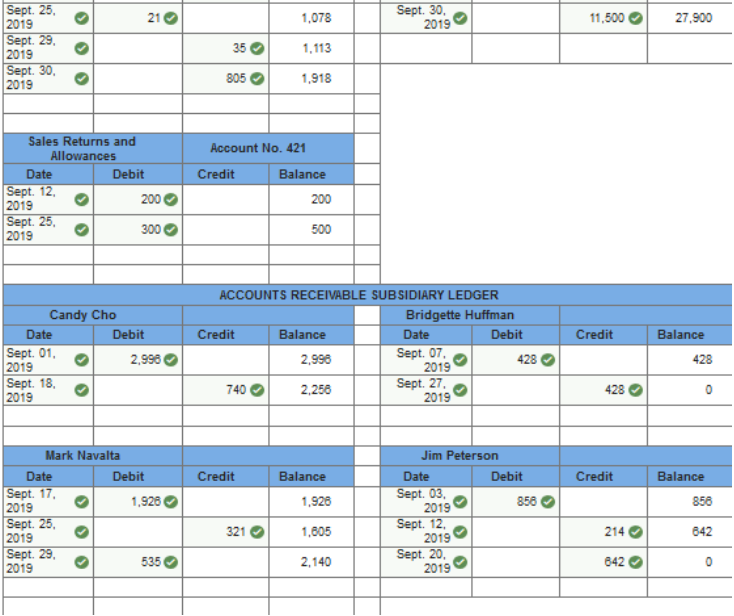

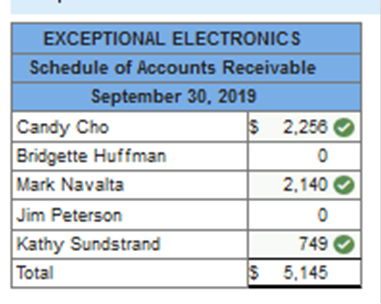

Analyze: $6,100 / $28,300 = 21.55%; 21.55% of the sales in September were for entertainment items. Problem 7.3A Posting transactions to the general ledger and accounts receivable ledger. LO 7-4, 7-5 Exceptional Electronics began operations September 1, 2019. The firm sells its merchandise for cash and on open account. Sales are subject to a 7 percent sales tax. During September, Exceptional Electronics engaged in the following transactions.

GENERAL LEDGER ACCOUNTS

ACCOUNTS RECEIVABLE LEDGER ACCOUNTS

Required: Post the entries from the general journal into the appropriate accounts in the general ledger and in the accounts receivable ledger. Prepare a schedule of accounts receivable. Analyze: What is the amount of sales tax owed at September 30, 2019?

Explanation 2.

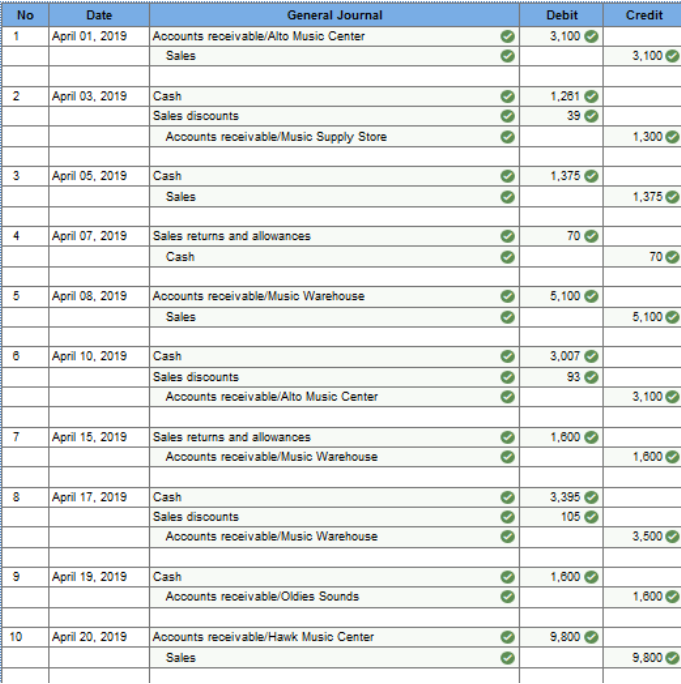

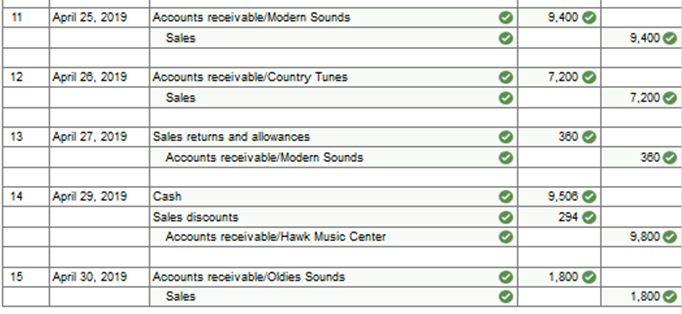

Problem 7.4A Recording sales, sales returns, cash discounts, and cash receipts for a wholesale business. LO 7-1, 7-3 Incredible Sounds is a wholesale business that sells musical instruments. Transactions involving sales and cash receipts for the firm during April 2019 follow. The firm sells its merchandise for cash and on open account. During April, Incredible Sounds engaged in the following transactions:

Required: Record the transactions in a general journal. Analyze: What was the amount of the cash discount taken by Hawk Music Center on April 29?

Explanation

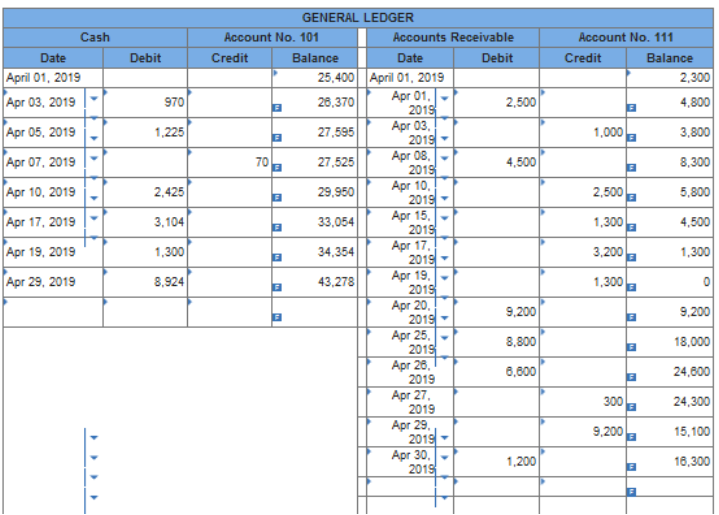

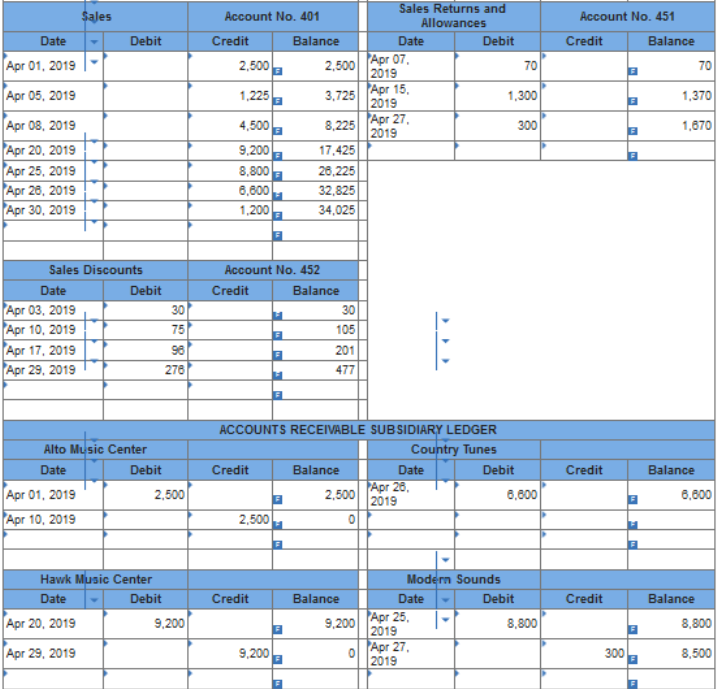

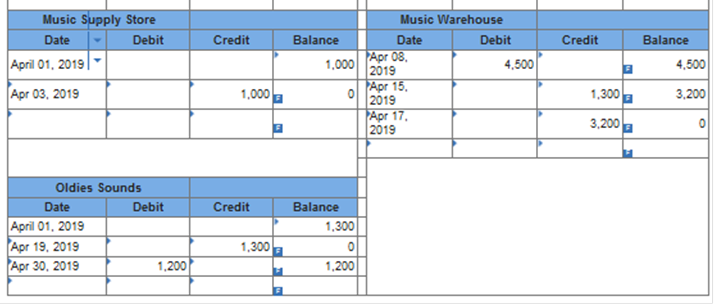

Problem 7.5A Posting transactions to the general ledger and accounts receivable ledger. LO 7-4, 7-5 Incredible Sounds is a wholesale business that sells musical instruments. Transactions involving sales and cash receipts for the firm during April 2019 follow. The firm sells its merchandise for cash and on open account. During April, Incredible Sounds engaged in the following transactions:

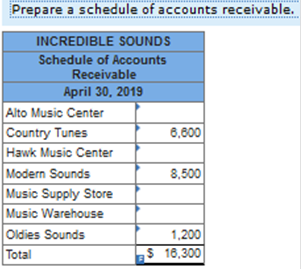

Required: Post the above transactions to the appropriate accounts in the general ledger and in the accounts receivable ledger. Prepare a schedule of accounts receivable.

Post the above transactions to the appropriate accounts in the general ledger and in the accounts receivable ledger.

Prepare a schedule of accounts receivable

Analyze: What were the total sales on account in April, prior to any returns, allowances, or discounts?

Explanation 2.

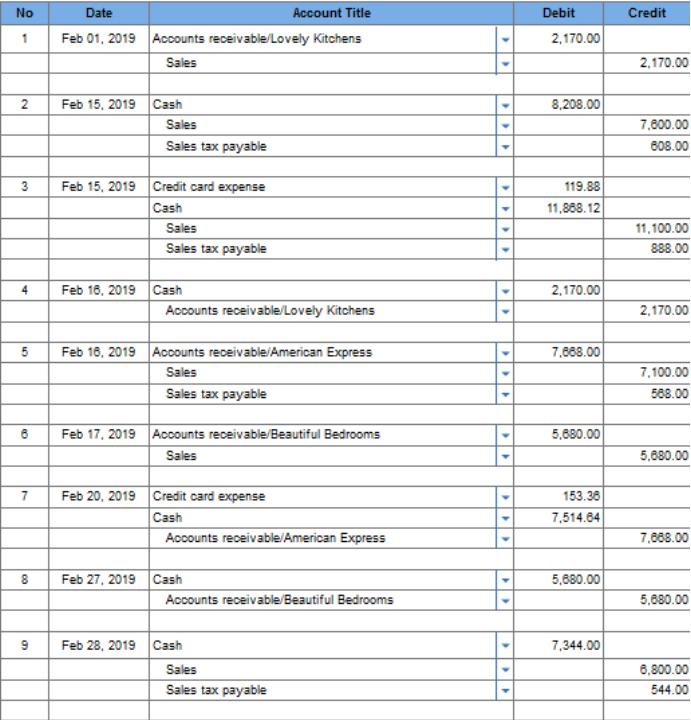

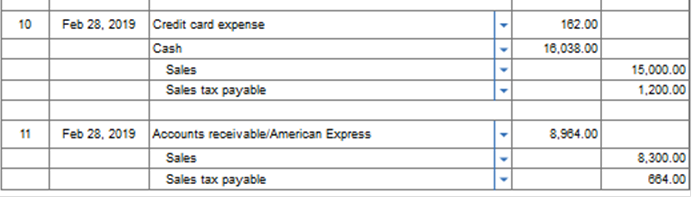

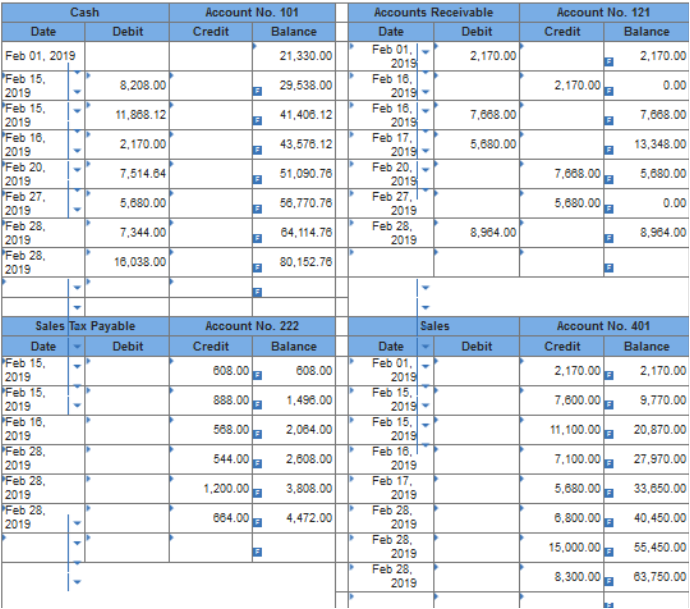

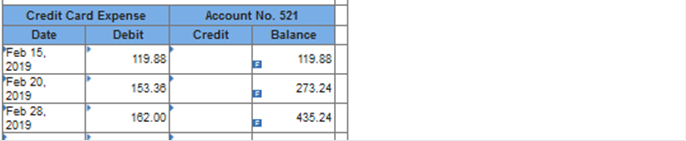

Problem 7.6A Recording sales made for cash, on open account, and with credit cards. LO 7-1, 7-2, 7-4 Royal Gift Shop sells cards, supplies, and various holiday greeting cards. Sales to retail customers are subject to an 8 percent sales tax. The firm sells its merchandise for cash; to customers using bank credit cards, such as MasterCard and Visa; and to customers using American Express. The bank credit cards charge a 1 percent fee. American Express charges a 2 percent fee. Royal Gift Shop also grants trade discounts to certain wholesale customers who place large orders. These orders are not subject to sales tax. During February 2019, Royal Gift Shop engaged in the following transactions:

Required: Record the transactions in a general journal. Post the entries from the general journal to the appropriate accounts in the general ledger.

Record the transactions in a general journal. (Round your intermediate calculations and final answers to 2 decimal places.)

Post the entries from the general journal to the appropriate accounts in the general ledger.

Analyze: What was the total credit card expense incurred in February?

Explanation 2.

Suppose the list price of goods is $1,500 and the trade discount is 40 percent. What is the net price? (List price - trade discount) $900 1,500 – (1,500 x .40) = 900 Suppose the list price is $1,500 and the trade discount is quoted as a series of 25 and 15 percent. What is the net price? (List price - first discount - second discount) $956.25 1,500 - 375.00 - 168.75 = 956.25 Firms that do a large volume of business with credit card companies might use separate ____________ ___________ accounts. general ledger At the end of each month, after all the accounts have been posted, Maxx-Out Sporting Goods prepares the _______ ________ ____________. sales tax return Three accounts are involved in the sales tax return: Sales Tax Payable, Sales, Sales Returns and Allowances What are the three types of business operations? service, merchandising, and manufacturing What is another name for a merchandising business? retailer Retailers of merchandising business sell _____________ to the customer. directly Merchandise inventory is the stock of goods a merchandising business keeps on hand. Merchandise Inventory is an asset account which will appear on the _____________ ____________. balance sheet Because of the complexity of buying and then reselling that merchandise and having to keep track of customer purchases/payments, etc., a __________________ may need to use special journals and subsidiary ledgers to record its business _______________________. merchandiser, transactions A ____________ _____________ is a journal used to record only one specific type of transaction. special journal A subsidiary ledger is a ____________________ ______________ for an account in the general ledger. supporting ledger There are several special journals which are very common in business including: Sales, Purchases, Cash receipts, and Cash payments The ______________________ ___________________ is NOT a special journal, but it is used for transactions that are not journalized in any special journal. General Journal The four credit sales require twelve postings to the general ledger: Four postings to Accounts Receivable Four postings to Sales Tax Payable Four postings to Sales The __________ ___________ tells us who the customer is and the sales amount, the sales tax charges and the total amount that the customer must pay. sales slip In a __________ journal, only one line is needed to record all information for each transaction, which helps avoid repetition. sales First, we enter the date, then the ________ __________ _____________, then the customer's name. sales slip number Next, enter the Sales amount __________ ___________ in the Sales column. before taxes Then enter the sales tax owed in the ________ __________ _____________ column and finally, enter the total of the sales slip in the Accounts Receivable column. Sales Tax Payable Even in a special journal, the total of the __________________. debits must equal the total of the credits A ________ _____________has specialized columns for accounts that are used most often. sales journal Once the journal has been ____________ and checked for ______________, then the column totals are ready to be posted. footed, equality With a ___________ journal, it is not necessary to post each sale individually. sale Instead ________________ _______________ are made at the end of the month based on the column totals of the sales journal. summary postings In a retail business such as Maxx-Out Sporting Goods, the data needed for each entry is taken from a copy of the customer's _________ __________. sales slip Post from the sales journal to the ___________ ______________ accounts. general ledger The ______________ ________________ ledger has three money columns. accounts receivable The ___________________ column is presumed to contain debit amounts. Balance Post from the sales journal to the ____________ ___________ in the accounts receivable subsidiary ______________. customer's accounts, ledger A comparison of the total of the schedule of accounts _________________ and the balance of the Accounts Receivable accounts shows that the two figures are ______ ___________. receivable, the same The basic procedures used by __________________ to handle sales and accounts receivable are _______ __________ as those used by _______________. wholesalers, the same, retailers Many wholesalers offer Cash discounts and __________ discounts. Trade What discounts do wholesalers offer? Cash and Trade Open-account credit is an example of types of ___________ sales. credit Business credit cards are an example of types of ___________ sales. credit Bank credit cards are an example of types of _________ sales. credit Cards issued by credit card companies are an example of types of ____________ sales. credit Record credit card sales in appropriate ________________. journals Businesses that have few transactions with credit card companies normally ____________ the amounts of such sales to the usual Accounts Receivable account in the general ledger and ___________ them to the same Sales account that is used for cash sales and other types of credit sales. debit, credit Payment from a credit card company is recorded in the ______ _______________ journal. cash receipts With a __________ _________________ it is not necessary to post each credit sale individually to general ledger accounts. sales journal Instead, _________________ ___________________ are made at the end of the month after the transaction amount columns of the sales journal are totaled. summary postings Sales taxes apply only to _______________ transactions. retail A _________________ business does not need to account for sales taxes. wholesale The __________ journal has a single amount column. sales The volume of both sales and profits will increase if buyers are given a period of a month or more to pay for the goods or services they purchase. This is _______________ of Credit Sales. advantages Each __________ sale recorded in the sales journal is posted to the appropriate customer's account in the accounts receivable subsidiary ledger. credit When a credit customer pays an outstanding bill, the cash collected is first recorded in a _____________. cash receipts journal A _________ is entered in the accounting records when the goods are _________ or the service is provided. sale, sold If something is wrong with the goods or service, the firm may allow a _________ __________ or give a sales _____________. sales return, allowance A _________ to the Sales Returns and Allowances account is preferred to making a direct ________ to the Sales. debit, debit Each sales return or allowance must be posted from the _____________ to the appropriate customer's account in the accounts receivable subsidiary ledger. journal The use of an _____________ ____________________ ledger does not eliminate the need for the Accounts Receivable account in the general ledger. accounts receivable The Accounts Receivable account (in the General Ledger) is now considered a _____________ account. control At the end of each month, after all the postings have been made, the balances in the ____________ ledger must be proved against the balance of the Accounts Receivable general ledger account. accounts receivable The _________________ _________________ account numbers are entered in parentheses under column totals. general ledger Homework Chapter 01 02 03 04 05 06 07 08 09 10 11 12 13 Test 01 02 03 04 05 06 07 08 09 10 11 12 13 Final Exam 01 02 Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |