|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

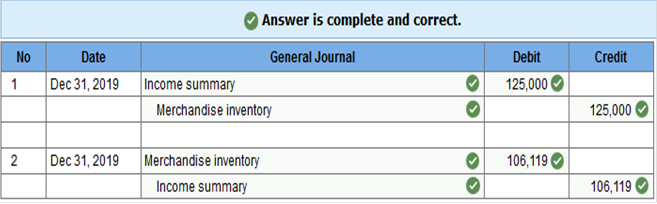

Homework Chapter 01 02 03 04 05 06 07 08 09 10 11 12 13 Test 01 02 03 04 05 06 07 08 09 10 11 12 13 Final Exam 01 02 Project Office Accounting: Homework Chapter 12 General Questions & Answers Exercise 12.1 Determining the adjustments for inventory. LO 12-1 The beginning inventory of Norcal Wholesalers was $125,000, and the ending inventory is $106,119. What entries are needed at the end of the fiscal period to adjust Merchandise Inventory?

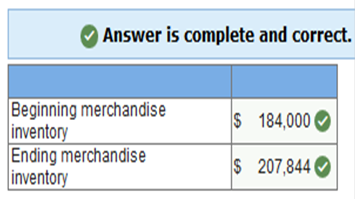

Exercise 12.2 Determining the adjustments for inventory. LO 12-1 The Income Statement section of the Johnson Company worksheet for the year ended December 31, 2019, has $184,000 recorded in the Debit column and $207,844 in the Credit column on the line for the Income Summary account. What were the beginning and ending balances for Merchandise Inventory?

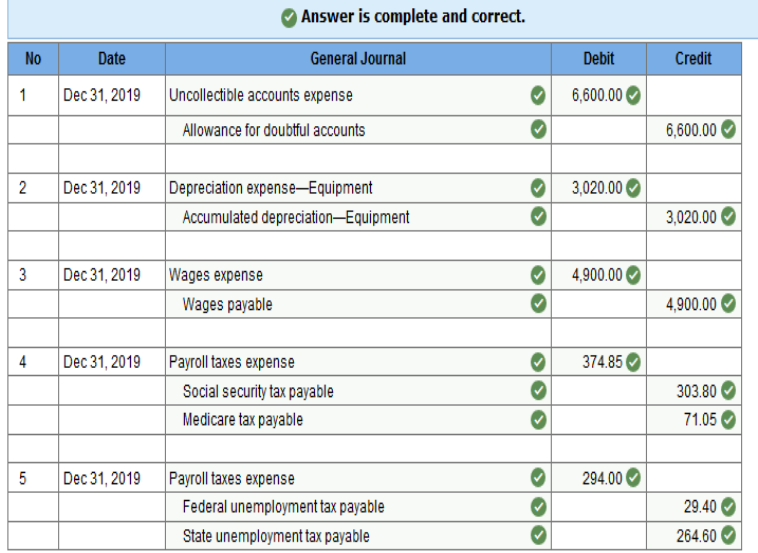

Exercise 12.3 Computing adjustments for uncollectible accounts, depreciation, and payroll items. LO 12-2 During the year 2019, Sampson Company had net credit sales of $1,100,000. Past experience shows that 0.6 percent of the firm’s net credit sales result in uncollectible accounts. Equipment purchased by Park Consultancy for $28,180 on January 2, 2019, has an estimated useful life of 9 years and an estimated salvage value of $1,000. What adjustment for depreciation should be recorded on the firm’s worksheet for the year ended December 31, 2019? On December 31, 2019, Giant Plumbing Supply owed wages of $4,900 to its factory employees, who are paid weekly. On December 31, 2019, Giant Plumbing Supply owed the employer’s social security (6.2 percent) and Medicare (1.45 percent) taxes on the entire $4,900 of accrued wages for its factory employees. On December 31, 2019, Giant Plumbing Supply owed federal (0.6 percent) and state (5.4 percent) unemployment taxes on the entire $4,900 of accrued wages for its factory employees. For each of the above independent situations, Prepare the adjusting entries that must be made on the December 31, 2019, worksheet. (Round your answers to 2 decimal places.)

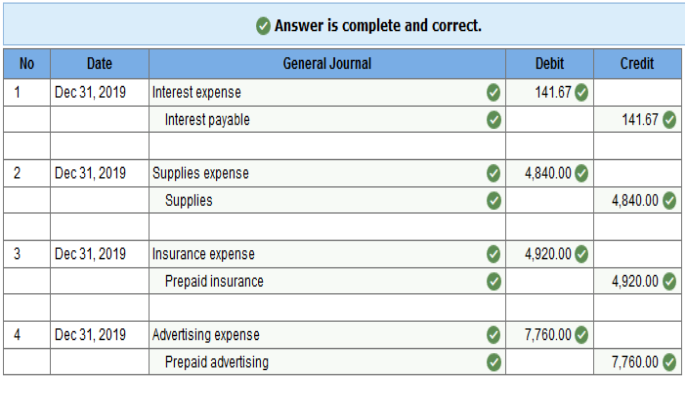

Exercise 12.4 Computing adjustments for accrued and prepaid expense items. LO 12-2 On December 31, 2019, the Notes Payable account at Northwood Manufacturing Company had a balance of $8,500. This balance represented a three-month, 10 percent note issued on November 1. On January 2, 2019, Hitech Computer Consultants purchased flash drives, paper, and other supplies for $6,560 in cash. On December 31, 2019, an inventory of supplies showed that items costing $1,720 were on hand. The Supplies account has a balance of $6,560 On September 1, 2019, North Dakota Manufacturing paid a premium of $14,760 in cash for a one-year insurance policy. On December 31, 2019, an examination of the insurance records showed that coverage for a period of four months had expired. On May 1, 2019, Headcase Beauty Salon signed a one-year advertising contract with a local radio station and issued a check for $11,640 to pay the total amount owed. On December 31, 2019, the Prepaid Advertising account has a balance of $11,640. For each of the above independent situations, prepare the adjusting entries that must be made on the December 31, 2019, worksheet assuming no previous adjusting entries have been made during the year. (Round your answers to 2 decimal places.)

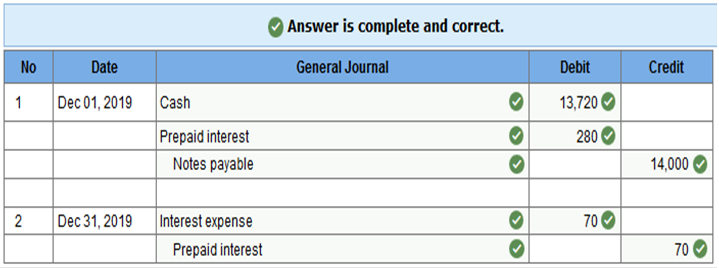

Exercise 12.5 Recording adjustments for prepaid interest. LO 12-2 On December 1, 2019, Jim’s Java Joint borrowed $14,000 from its bank in order to expand its operations. The firm issued a four-month, 6 percent note for $14,000 to the bank and received $13,720 in cash because the bank deducted the interest for the entire period in advance. In general journal form, show the entry that would be made to record this transaction and the adjustment for prepaid interest that should be recorded on the firm’s worksheet for the year ended December 31, 2019.

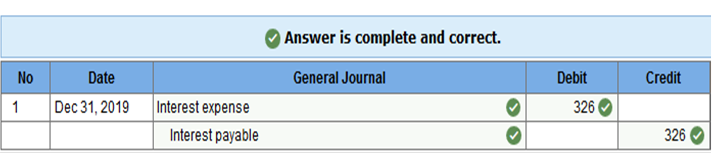

Exercise 12.6 Recording adjustments for accrued interest. LO 12-2 On December 31, 2019, the Notes Payable account at Vanessa’s Boutique Shop had a balance of $65,200. This amount represented funds borrowed on a six-month, 6 percent note from the firm’s bank on December 1. Record the journal entry for interest expense on this note that should be recorded on the firm’s worksheet for the year ended December 31, 2019.

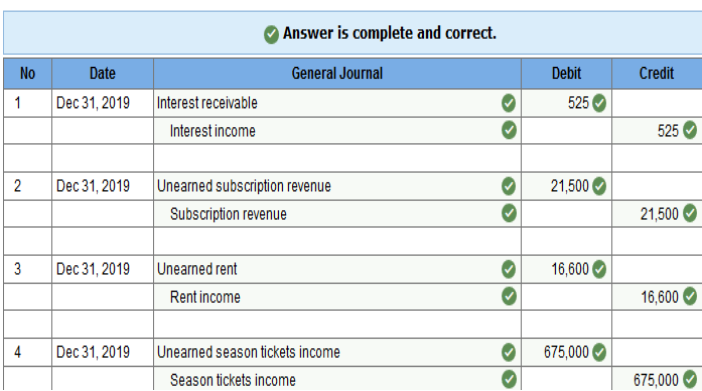

Exercise 12.7 Recording adjustments for accrued and deferred income items. LO 12-3 On December 31, 2019, the Notes Receivable account at P. Davis Materials Corporation had a balance of $17,500, which represented a six-month, 12 percent note received from a customer on October 1. During the week ended June 7, 2019, McCormick Media received $43,000 from customers for subscriptions to its magazine Modern Business. On December 31, 2019, an analysis of the Unearned Subscription Revenue account showed that half of the subscriptions were earned in 2019. On November 1, 2019, Perez Realty Company rented a commercial building to a new tenant and received $49,800 in advance to cover the rent for six months. Upon receipt, the $49,800 was recorded in the Unearned Rent account. On November 1, 2019, the Mighty Bucks Hockey Club sold season tickets for 40 home games, receiving $5,400,000. Upon receipt, the $5,400,000 was recorded in the Unearned Season Tickets Income account. At December 31, 2019, the Mighty Bucks Hockey Club had played 5 home games. For each of the above independent situations, indicate the adjusting entry that must be made on the December 31, 2019, worksheet assuming no previous adjusting entries have been made during the year.

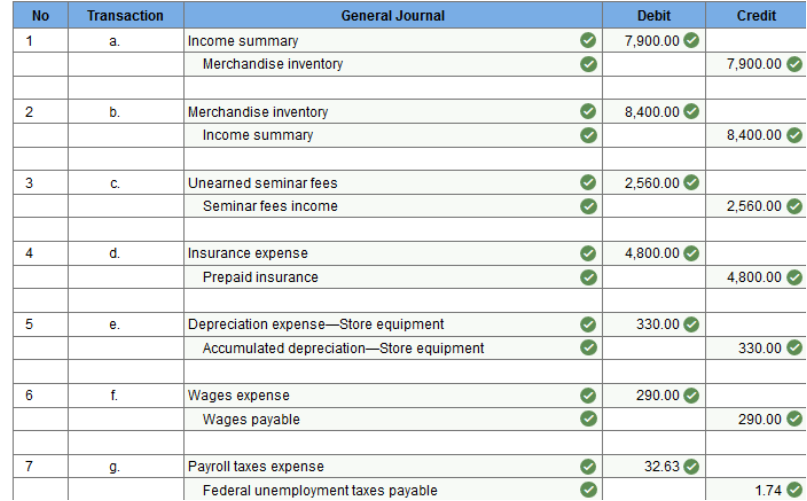

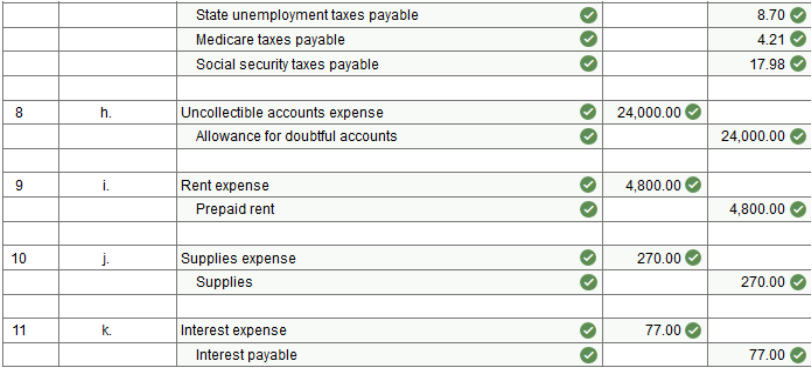

a.-b. Merchandise Inventory, before adjustment, has a balance of $7,900. The newly counted inventory balance is $8,400. Unearned Seminar Fees has a balance of $6,400, representing prepayment by customers for five seminars to be conducted in June, July, and August 2019. Two seminars had been conducted by June 30, 2019. Prepaid Insurance has a balance of $14,400 for six months’ insurance paid in advance on May 1, 2019. Store equipment costing $5,820 was purchased on March 31, 2019. It has a salvage value of $540 and a useful life of four years. Employees have earned $290 that has not been paid at June 30, 2019. The employer owes the following taxes on wages not paid at June 30, 2019: SUTA, $8.70; FUTA, $1.74; Medicare, $4.21; and social security, $17.98. Management estimates uncollectible accounts expense at 1 percent of sales. This year’s sales were $2,400,000. Prepaid Rent has a balance of $7,200 for six months’ rent paid in advance on March 1, 2019. The Supplies account in the general ledger has a balance of $440. A count of supplies on hand at June 30, 2019, indicated $170 of supplies remain. The company borrowed $7,700 from First Bank on June 1, 2019, and issued a four-month note. The note bears interest at 12 percent. Required: Based on the information above, record the adjusting journal entries that must be made for Sufen Consulting on June 30, 2019. The company has a June 30 fiscal year-end. Analyze: After all adjusting entries have been journalized and posted, what is the balance of the Prepaid Rent account? Based on the above information, record the adjusting journal entries that must be made for Sufen Consulting on June 30, 2019. The company has a June 30 fiscal year-end. (Round your final answers to 2 decimal places.)

===============================================

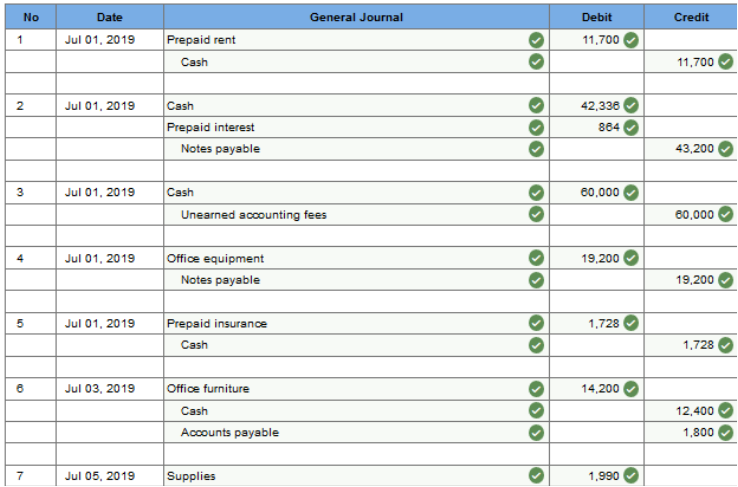

Problem 12.2A Recording adjustments for accrued and prepaid expense items and unearned income. LO 12-2, 12-3 On July 1, 2019, Tim Stein established his own accounting practice. Selected transactions for the first few days of July follow.

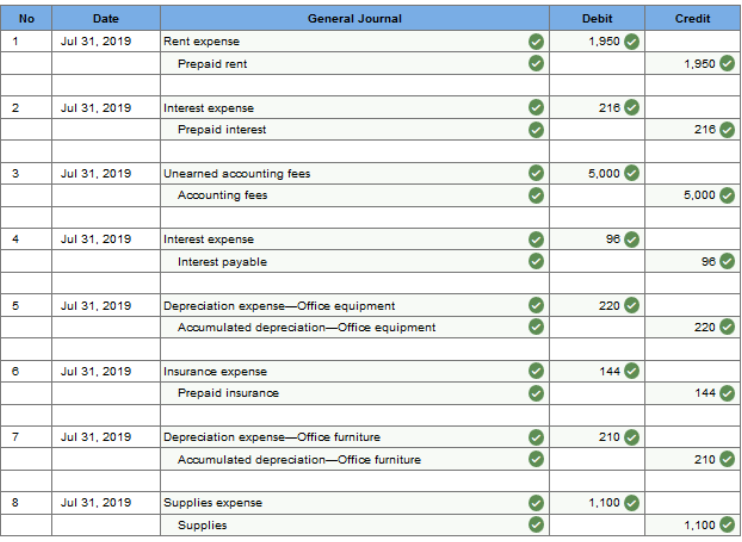

Required: Record the transactions in the general journal. Assume that the firm initially records prepaid expenses as assets and unearned income as a liability for the year 2019. Record the adjusting journal entries that must be made on July 31, 2019. Analyze: What balance should be reflected in Unearned Accounting Fees at July 31, 2019?

Problem 12.3A Recording adjustments for accrued and prepaid expense items and earned income. LO 12-2, 12-3 On July 31, 2019, after one month of operation, the general ledger of Michael Domenici, Consultant, contained the accounts and balances given below.

ADJUSTMENTS On July 31, an inventory of the supplies showed that items costing $575 were on hand. On July 1, the firm paid $8,850 in advance for six months of rent. On July 1, the firm purchased a one-year insurance policy for $1,560. On July 1, the firm paid $356 interest in advance on a four-month note that it issued to the bank. On July 1, the firm purchased office furniture for $10,453. The furniture is expected to have a useful life of six years and a salvage value of $1,525. On July 1, the firm purchased office equipment for $6,315. The equipment is expected to have a useful life of five years and a salvage value of $1,575. On July 1, the firm issued a three-month, 6 percent note for $7,600. On July 1, the firm received a consulting fee of $4,680 in advance for a one-year period. Required: Prepare a partial worksheet with the following sections: Trial Balance, Adjustments, and Adjusted Trial Balance. Use the data about the firm’s accounts and balances to complete the Trial Balance section. Enter the adjustments described above in the Adjustments section. Complete the Adjusted Trial Balance section. Analyze: By what total amount were the expense accounts of the business adjusted?

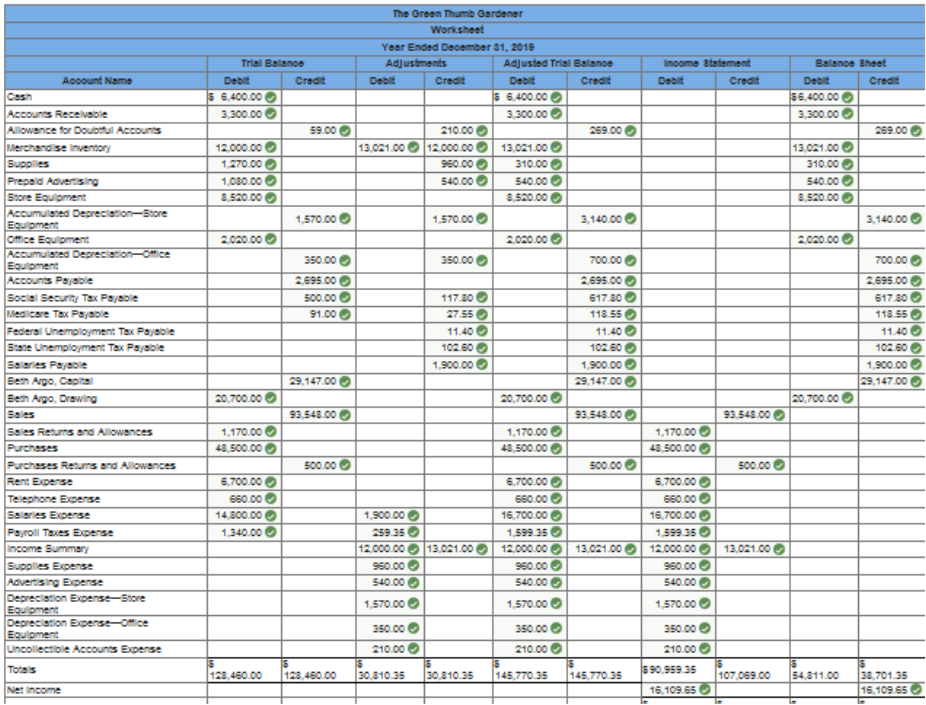

Problem 12.4A Recording adjustments and completing the worksheet. LO 12-1, 12-2, 12-3, 12-4 The Green Thumb Gardener is a retail store that sells plants, soil, and decorative pots. On December 31, 2019, the firm's general ledger contained the accounts and balances that appear below.

ADJUSTMENTS a.–b. Merchandise inventory on December 31, 2019, is $13,021. During 2019, the firm had net credit sales of $42,000; the firm estimates that 0.5 percent of these sales will result in uncollectible accounts. On December 31, 2019, an inventory of the supplies showed that items costing $310 were on hand. On October 1, 2019, the firm signed a six-month advertising contract for $1,080 with a local newspaper and paid the full amount in advance. On January 2, 2018, the firm purchased store equipment for $8,520. At that time, the equipment was estimated to have a useful life of five years and a salvage value of $670. On January 2, 2018, the firm purchased office equipment for $2,020. At that time, the equipment was estimated to have a useful life of five years and a salvage value of $270. On December 31, 2019, the firm owed salaries of $1,900 that will not be paid until 2020. On December 31, 2019, the firm owed the employer’s social security tax (assume 6.2 percent) and Medicare tax (assume 1.45 percent) on the entire $1,900 of accrued wages. On December 31, 2019, the firm owed federal unemployment tax (assume 0.6 percent) and state unemployment tax (assume 5.4 percent) on the entire $1,900 of accrued wages. Required: Prepare the Trial Balance section of a 10-column worksheet. The worksheet covers the year ended December 31, 2019. Enter the adjustments above in the Adjustments section of the worksheet. Complete the worksheet. Analyze: By what amount were the assets of the business affected by adjustments?

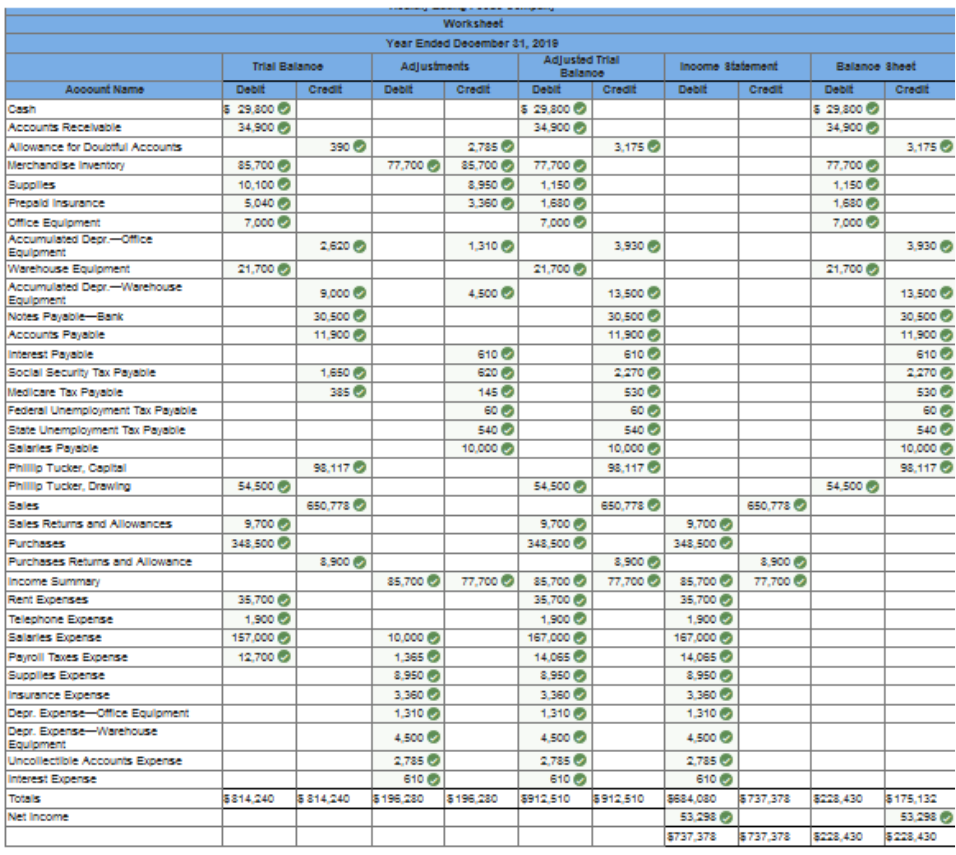

Explanation Analyze: The total assets (assets, less accumulated depreciation) were decreased $2,609 by adjustments. Problem 12.5A Recording adjustments and completing the worksheet. LO 12-1, 12-2, 12-3, 12-4 Healthy Eating Foods Company is a distributor of nutritious snack foods such as granola bars. On December 31, 2019, the firm’s general ledger contained the accounts and balances that follow.

ADJUSTMENTS a.–b. Merchandise inventory on December 31, 2019, is $77,700. During 2019, the firm had net credit sales of $557,000; past experience indicates that 0.50 percent of these sales should result in uncollectible accounts. On December 31, 2019, an inventory of supplies showed that items costing $1,150 were on hand. On May 1, 2019, the firm purchased a one-year insurance policy for $5,040. On January 2, 2017, the firm purchased office equipment for $7,000. At that time, the equipment was estimated to have a useful life of five years and a salvage value of $450. On January 2, 2017, the firm purchased warehouse equipment for $21,700. At that time, the equipment was estimated to have a useful life of four years and a salvage value of $3,700. On November 1, 2019, the firm issued a four-month, 12 percent note for $30,500. On December 31, 2019, the firm owed salaries of $10,000 that will not be paid until 2020. On December 31, 2019, the firm owed the employer’s social security tax (assume 6.2 percent) and Medicare tax (assume 1.45 percent) on the entire $10,000 of accrued wages. On December 31, 2019, the firm owed the federal unemployment tax (assume 0.6 percent) and the state unemployment ta (assume 5.4 percent) on the entire $10,000 of accrued wages. Required: Prepare the Trial Balance section of a 10-column worksheet. The worksheet covers the year ended December 31, 2019. Enter the adjustments above in the Adjustments section of the worksheet. Complete the worksheet. Analyze: When the financial statements for Healthy Eating Foods Company are prepared, what net income will be reported for the period ended December 31, 2019?

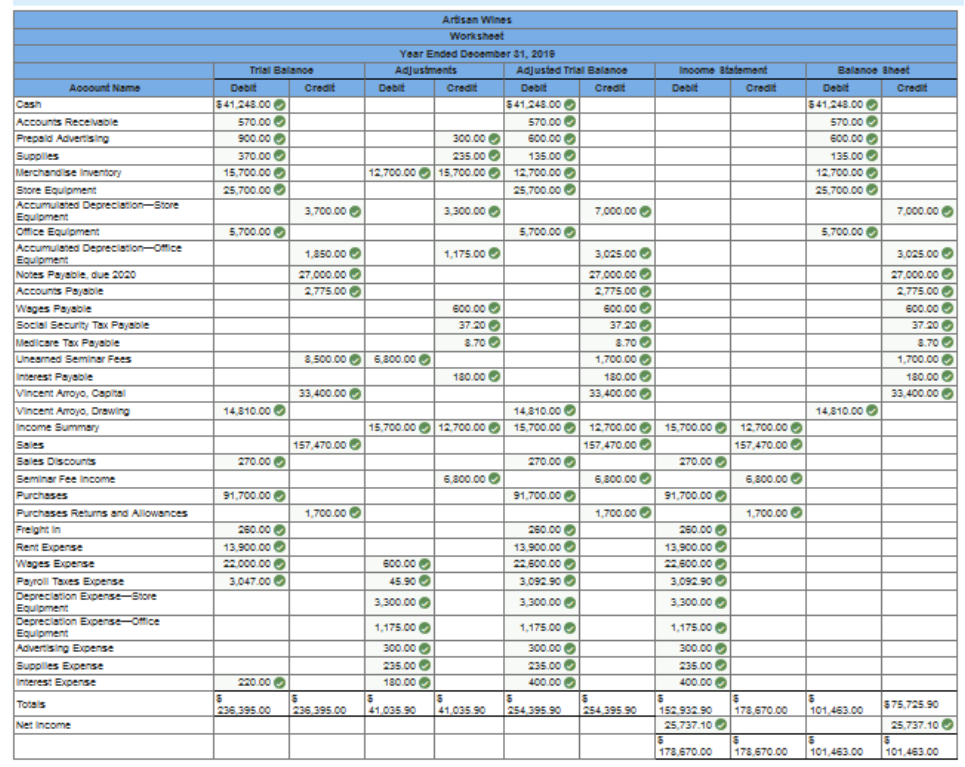

Problem 12.6A Recording adjustments and completing the worksheet. LO 12-1, 12-2, 12-3, 12-4 The Artisan Wines is a retail store selling vintage wines. On December 31, 2019, the firm’s general ledger contained the accounts and balances below. All account balances are normal.

ADJUSTMENTS: a.–b. Merchandise inventory at December 31, 2019, was counted and determined to be $12,700. The amount recorded as prepaid advertising represents $900 paid on September 1, 2019, for 12 months of advertising. The amount of supplies on hand at December 31 was $135. Depreciation on store equipment was $3,300 for 2019. Depreciation on office equipment was $1,175 for 2019. Unearned Seminar Fees represent $8,500 received on November 1, 2019, for five seminars. At December 31, four of these seminars had been conducted. Wages owed but not paid at December 31 were $600. On December 31, 2019, the firm owed the employer’s social security tax ($37.20) and Medicare tax ($8.70). The note payable bears interest at 8% per annum. One month’s interest is owed at December 31, 2019. Required: Prepare the Trial Balance section of a 10-column worksheet. The worksheet covers the year ended December 31, 2019. Enter the adjustments above in the Adjustments section of the worksheet. Complete the worksheet. Analyze: What was the amount of revenue earned by conducting seminars during the year ended December 31, 2019?

At the beginning of the current year, a company purchased machinery for $50,000. It has a salvage value of $6,000 and an estimated useful life of 8 years. How much is depreciation expense for the first year under the straight-line method? $5,500 (50,000 - 6,000) / 8 = 5,500 Corian Company purchased equipment and incurred these costs: Cash price, $24,000; Sales taxes, $1,200; Insurance during transit, $200; Annual maintenance costs, $400. What amount should be recorded as the cost of the equipment? $25,400 24,000 + 1,200 + 200 = 25,400) An asset purchased on January 1 for $40,000 has an estimated salvage value of $4,000. The current useful life is 8 years. How much is total accumulated depreciation using the straight-line method at the end of the second year of life? $9,000 40,000 - 4,000) / 8 years = 4,500 4,500 x 2 = 9,000. A company uses straight-line depreciation. It purchased a truck for $40,000. The truck's salvage value is $4,000. The truck's monthly depreciation expense is $600. What is the truck's useful life? 5 years 40,000 - 4,000 = 36,000 600 x 12 (months) = 7,200 36,000 / 7,200 = 5 Drysdale Company purchased land for $560,000. Drysdale also paid a real estate brokers' commission of $24,000 and spent $20,000 demolishing an old building on the land before construction of a new building could start. Proceeds from salvage of the demolished building was $2,000. Drysdale additionally assumed $5,000 in property taxes due on the land owed by the previous owner. Under the historical cost principle, the cost of land would be recorded at $607,000 560,000 + 24,000 + (20,000 - 2,000) + 5,000 = 607,000 Jack's Copy Shop bought equipment for $180,000 on January 1 of its first year. The equipment's original estimated useful life is 3 years and its estimated salvage value is $30,000. The company uses the straight-line method of depreciation. On December 31 of its third year, before year-end adjusting entries have been recorded, Jack's decides to extend the estimated useful life 1 year giving it a total life of 4 years. The company did not change the salvage value and continues to use the straight-line method. How much depreciation expense should be recorded for the third year? $25,000 180,000 - 30,000) / 3 = 50,000 180,000 - 2 x 50,000 - 30,000) / (4-2) = 25,000 A company has the following asset account balances: Buildings and equipment, $6,400,000 Accumulated depreciation, $1,600,000 Patents, $1,050,000 Inventory, $1,200,000 Goodwill, $4,000,000 How much will be reported on the balance sheet under property, plant & equipment? $4,800,000 6,400,000 - 1,600,000 = 4,800,000. A company's average total assets are $250,000, depreciation expense is $10,000, and accumulated depreciation is $60,000. Net income is $1,200,000. Net sales total $300,000. What is the asset turnover? 1.2 300,000 / 250,000 = 1.2 On October 1 of the current year, Mann Company purchased and places a new asset into service. The cost of the asset is $80,000 with an estimated 5-year life and $20,000 salvage value at the end of its useful life. What is the depreciation expense for the current year ending December 31 if the company uses the straight-line method of depreciation? $3,000 80,000 - 20,000 / 5 = 12,000 12,000 x 3/12 = 3,000 A company sold a plant asset for $3,000. It had a cost $10,000 and its accumulated depreciation is $7,500. What gain or loss did the company experience? $500 10,000 - 7,500 = 2,500 3,000 – 2,500 = 500 Welch Company's average total assets is $200,000, average total equity is $120,000, and net sales is $100,000. Its return on assets is 15%. What was the company's net income? $30,000 200,000 x 0.15 = 30,000. Given the following account balances at year end, how much is amortization expense on Analog Enterprises' income statement for the current year if the company amortizes intangibles over ten years? Sales revenue, $45,000,000; Patents, $2,500,000; Accounts receivable, $4,000,000; Land, $15,000,000; Equipment, $25,000,000; Trademarks, $1,200,000; Goodwill, $4,500,000; and Copyrights, $1,500,000. The company also paid $2,000,000 for research & development at the start of the current year. Assume that all of the company's intangible assets were acquired at the start of the current year. $400,000 2,500,000 + 1,500,000) / 10 = 400,000 In the current year, Pierce Company incurred $150,000 of research and development costs in its laboratory to develop a new product. It also spent $20,000 in legal fees for a patent on that new product. Later in the current year, Pierce paid $15,000 for legal fees in a successful defense of that patent. What is the total amount that should be debited to the company's Patents account in the current year? $35,000 20,000 + 15,000 = 35,000 Homework Chapter 01 02 03 04 05 06 07 08 09 10 11 12 13 Test 01 02 03 04 05 06 07 08 09 10 11 12 13 Final Exam 01 02 Project

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |