|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Intermediate Accounting (ACG 3101) Homework 8 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11 | Final Exam

Required information

Learning Objective 08-01 Explain the types of inventory and the differences between a perpetual inventory system and a periodic inventory system. Skip to question [The following information applies to the questions displayed below.] Inventory for a manufacturing company includes raw materials, work in process, and finished goods. Inventory for a merchandising company includes goods primarily in finished form ready for sale. In a perpetual inventory system, inventory is continually adjusted for each change in inventory. Cost of goods sold is adjusted each time goods are sold or returned by a customer. A periodic inventory system adjusts inventory and records cost of goods sold only at the end of a reporting period. Which of the following statements about the types of inventory is (are) correct? (Select all that apply.) Check All That Apply When the manufacturing process is complete, the cost of the related inventory items is transferred into finished goods. Inventory is classified as an asset in the balance sheet until it is sold, at which time the cost is transferred to cost of goods sold in the income statement. Explanation Knowledge Check 01 Merchandising companies purchase goods that are primarily in finished form. Unlike merchandising companies, manufacturing companies Abbott Company uses a perpetual inventory system. When does Abbott record transactions relating to its inventory? Sales revenue and cost of goods sold are both recorded at the time of the sale. Explanation Knowledge Check 01 When a company uses a perpetual inventory system, the system continually records sales to customers and the cost of inventory sold. Barrington Company began the year with inventory of $100,000. During the year, the company purchased inventory in the amount of $750,000. Sales revenue for the year totaled $800,000. A physical count determined the cost of inventory at the end of the year to be $90,000. The adjusting entry needed at the end of the year under a periodic inventory system includes a: Debit to Cost of Goods Sold for $760,000. Explanation Knowledge Check 01

The journal entry includes a debit to Cost of Goods Sold for $760,000, a debit to Inventory for $90,000 (the ending inventory amount), Learning Objective 08-02 Explain which physical units of goods should be included in inventory. Skip to question [The following information applies to the questions displayed below.] Generally, determining the physical quantity that should be included in inventory is a simple matter because it consists of items in the possession of the company. However, at the end of a reporting period it’s important to determine the ownership of goods that are in transit Hales Inc. ships goods on December 30 to Osher Inc., who receives the goods on January 2. Both companies have December 31 year-ends. If the goods are shipped f.o.b. shipping point, which of the following statements is (are) correct? (Select all that apply.) Osher will include the goods in its December 31 inventory. Hales will record the sale on December 30. Osher will record the purchase on December 30. Explanation Knowledge Check 01 If the goods are shipped f.o.b. shipping point, then legal title to the goods changes hands at the point of shipment (December 30) when the seller delivers the goods to the carrier. On December 15, Reynolds Inc. ships goods on consignment to Manella Inc., who receives the goods on December 20. Manella sells the goods to a customer on January 5 of the following year. Both companies have December 31 year-ends. Which of the following statements is correct? Reynolds will include the goods in its December 31 inventory. Explanation Knowledge Check 01 When Reynolds (the consignor) shipped the goods on consignment to Manella (the consignee), the goods were physically transferred to Manella, Bluestein Inc. purchases goods from one of its suppliers and incurs freight charges to have the goods delivered. The company uses a perpetual system. Which of the following statements is correct? Bluestein will record the freight charges in its Inventory account. Platter Inc. purchases goods from a supplier and later returns those goods. Platter uses a perpetual system. Which of the following statements is correct? Platter will record the return by reducing its Inventory account. Learning Objective 08-03 Account for transactions that affect net purchases and prepare a cost of goods sold schedule. Skip to question [The following information applies to the questions displayed below.] The cost of inventory includes all expenditures necessary to acquire the inventory and bring it to its desired condition and location for sale or use. Generally, these expenditures include the purchase price of the goods reduced by any returns and purchase discounts, plus freight-in charges. Platen purchased inventory on August 17 and received an invoice with a list price amount of $5,900 and payment terms of 4/10, n/30. Platen uses the net method to record purchases. For what amount should Platen record the purchase? $5664 Explanation Knowledge Check 01 Platen will record the purchase on August 17 with a debit to Purchases (periodic system) and a credit to Accounts Payable for $5,664, computed as $5,900 less 4%. $ 5,900 − ($5,900 × 4%) = $5,664 Jameson Company uses average cost and a perpetual system. On January 1, the company had 600 units of inventory at an average cost of $55 per unit Purchases: January 10: 1,000 units at $59 = $59,000 January 20: 800 units at $62 = $49,600 Sales: January 12: 1,200 units January 28: 900 units What is the average cost per unit that should be used to determine the cost of the units sold on January 28? (Round your answer to two decimal points.) $60.50 Explanation Knowledge Check 01 At January 10: Cost of units available for sale = $33,000 + $59,000 = $92,000 Units available for sale = 600 + 1,000 = 1,600 Average cost per unit = $92,000 ÷ 1,600 units = $57.50 At January 12: 1,600 units available − 1,200 units sold = 400 units Cost of units available for sale = 400 × $57.50 = $23,000 At January 20: Cost of units available for sale = $23,000 + $49,600 = $72,600 Units available for sale = 400 + 800 = 1,200 Average cost per unit = $72,600 ÷ 1,200 units = $60.50 Learning Objective 08-04 Differentiate between the specific identification, FIFO, LIFO, and average cost methods used to determine the cost of ending inventory and cost of goods sold. Skip to question [The following information applies to the questions displayed below.] Once costs are determined, the cost of goods available for sale must be allocated between cost of goods sold and ending inventory. Unless each item is specifically identified and traced through the system, the allocation requires an assumption regarding the flow of costs. First-in, first-out (FIFO) assumes that units sold are the first units acquired. Last-in, first-out (LIFO) assumes that the units sold are the most recent Otis Corp. uses a periodic system and the FIFO method. Otis had beginning inventory of 30 units purchased at $120 each, and made the following purchases during the year:

Sales during the year totaled 271 units. What is the cost of ending inventory? $840 Explanation Knowledge Check 01 The first-in, first-out (FIFO) method assumes that the first units purchased are sold first. Beginning inventory is sold first, followed by purchases in chronological order. Thus, we assume the 14 units in ending inventory (30 + 34 + 61 + 160 − 271) are from the last purchase on October 20. 14 units × $60 = $840 Carrington Corp. uses a periodic system and the LIFO method. Carrington had beginning inventory of 30 units purchased at $120 each and made the following purchases during the year:

Sales during the year totaled 271 units. What is the cost of ending inventory? $1,680 Explanation Knowledge Check 01 The last-in, first-out (LIFO) method assumes that units sold are the most recent units acquired. The units just purchased are sold first, 14 units × $120 = $1,680 If costs are rising, which inventory method will result in the highest cost of goods sold? lifo Learning Objective 08-08 Determine ending inventory using the dollar-value LIFO inventory method. Skip to question [The following information applies to the questions displayed below.] The dollar-value LIFO method converts ending inventory at year-end cost to base year cost using a cost index. After identifying the layers in ending inventory with the years they were created, each year’s base year cost measurement is converted to layer year cost measurement using the layer year’s cost index. The layers are then summed to obtain total ending inventory at cost. On January 1, Greenview Company adopted the dollar-value LIFO method. The inventory cost on January 1 was $112,000. On December 31, ending inventory had a cost of $136,400. The cost index for the year was 1.10. For what amount would ending inventory be reported? $125,200 Explanation Knowledge Check 01 Step 1: Convert ending inventory to base year cost by dividing ending inventory by the year’s cost index.

Step 2: Identify the layers of ending inventory created each year.

Step 3: Restate each layer using the cost index in the year acquired.

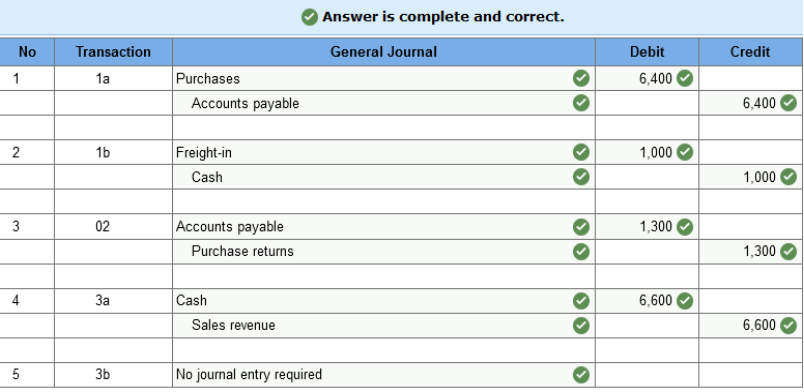

Learning Objective 09-01 Understand and apply rules for measurement of inventory at the end of the reporting period. Skip to question [The following information applies to the questions displayed below.] Companies that use FIFO, average cost, or any other method besides LIFO or the retail inventory method report inventory at the lower of cost or net realizable value (NRV). Net realizable value is selling price less costs to sell. Companies that use LIFO or the retail inventory method report inventory at the lower of cost or market. Market equals replacement cost, except that market should not (a) be greater than NRV (ceiling) or (b) be less than NRV minus an approximately normal profit margin (floor). At the end of the year, inventory has a cost of $200,000 and a net realizable value of $195,000 due to normal business circumstances. Prepare the year-end adjusting entry, if any, for inventory using the lower of cost or net realizable value approach. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) Cost of Goods Sold $5,000 Inventory $5,000 At the end of the year, inventory has a cost of $200,000, net realizable value of $195,000, replacement cost of $160,000, and normal profit margin of $25,000. Assuming normal business circumstances, prepare the year-end adjusting entry, if any, for inventory using the lower of cost or market approach. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) Cost of Goods Sold $30,000 Inventory $30,000 Explanation Knowledge Check 01 Market value equals replacement cost ($160,000), except market cannot be above the ceiling (NRV) of $195,000 or below the floor of $170,000 In this case, replacement cost is below the floor, so market becomes the floor of $170,000, which is lower Exercise 8-2 (Algo) Periodic inventory system; journal entries [LO8-1] John’s Specialty Store uses a periodic inventory system. The following are some inventory transactions for the month of May: John's purchased merchandise on account for $6,400. Freight charges of $1,000 were paid in cash. John’s returned some of the merchandise purchased in (1). The cost of the merchandise was $1,300 and John’s account was credited by the supplier. Required: Prepare the necessary journal entries to record these transactions. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)  Exercise 8-6 (Algo) Goods in transit [LO8-2] The Kwok Company’s inventory balance on December 31, 2021, was $185,000 (based on a 12/31/2021 physical count) before considering the following transactions: Goods shipped to Kwok f.o.b. destination on December 20, 2021, were received on January 4, 2022. The invoice cost was $34,000. Goods shipped to Kwok f.o.b. shipping point on December 28, 2021, were received on January 5, 2022. The invoice cost was $21,000. Goods shipped from Kwok to a customer f.o.b. destination on December 27, 2021, were received by the customer on January 3, 2022. The sales price was $44,000 and the merchandise cost $26,000. Goods shipped from Kwok to a customer f.o.b. destination on December 26, 2021, were received by the customer on December 30, 2021. The sales price was $24,000 and the merchandise cost $17,000. Goods shipped from Kwok to a customer f.o.b. shipping point on December 28, 2021, were received by the customer on January 4, 2022. The sales price was $29,000 and the merchandise cost $16,000. Required: Determine the correct inventory amount to be reported in Kwok’s 2021 balance sheet. $232,000 Explanation

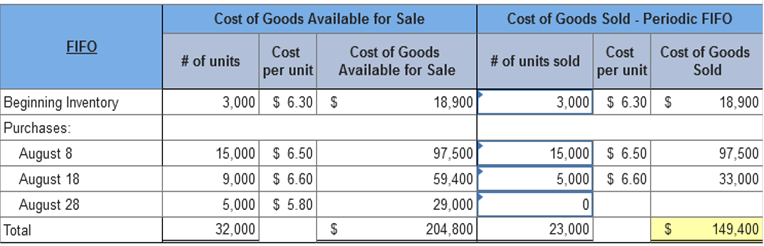

Exercise 8-13 (Algo) Inventory cost flow methods; periodic system [LO8-1, 8-4] Altira Corporation provides the following information related to its merchandise inventory during the month of August 2021:

Required: Using calculations based on a periodic inventory system, determine the inventory balance Altira would report in its August 31, 2021, balance sheet and the cost of goods sold it would report in its August 2021 income statement using each of the following cost flow methods.       Explanation Cost of goods available for sale:

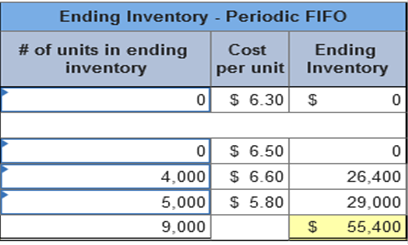

First-in, first-out (FIFO)

Cost of ending inventory:

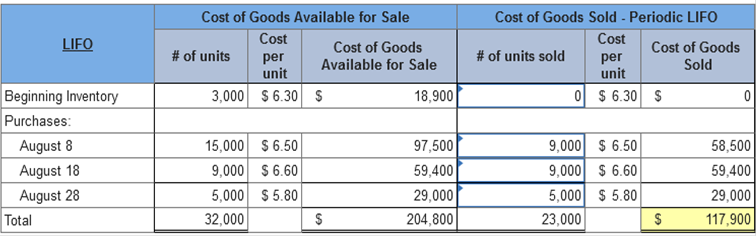

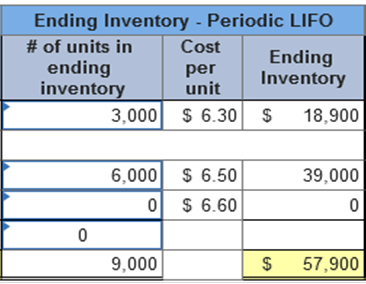

Last-in, first-out (LIFO)

Cost of ending inventory:

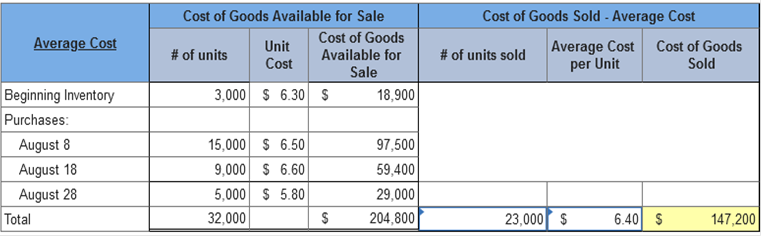

Average Cost

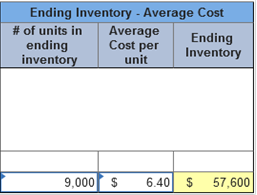

Cost of ending inventory:

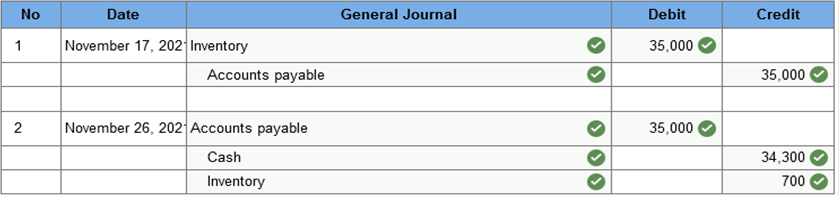

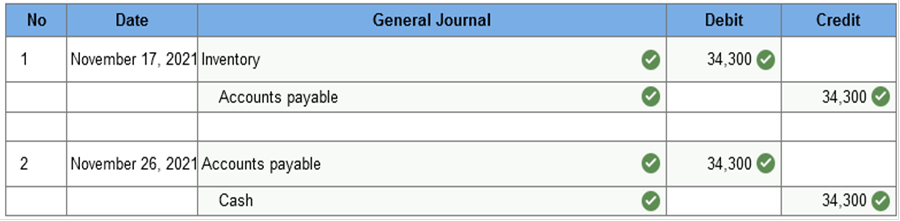

9,000 units × $6.40 = $57,600 *Alternatively, could be determined by multiplying the units sold by the average cost: 23,000 units × $6.40 = $147,200 Required information Exercise 8-11 (Static) Trade and purchase discounts; the gross method and the net method compared [LO8-3] Skip to question [The following information applies to the questions displayed below.] Tracy Company, a manufacturer of air conditioners, sold 100 units to Thomas Company on November 17, 2021. The units have a list price of $500 each, but Thomas was given a 30% trade discount. The terms of the sale were 2/10, n/30. Thomas uses a perpetual inventory system. Exercise 8-11 (Static) Parts 1 and 2 Required: 1. Prepare the journal entries to record the (a) purchase by Thomas on November 17 and (b) payment on November 26, 2021. Thomas uses the gross method of accounting for purchase discounts. 2. Prepare the journal entry for the payment, assuming instead that it was made on December 15, 2021.  In a perpetual average cost system  Explanation 1. November 17, 2021 Inventory: $500 × 70% = $350 per unit. 100 units × $350 = $35,000 November 26, 2021 Inventory: 2% × $35,000 = $700 Cash: 98% × $35,000 = $34,300 Required information Exercise 8-11 (Static) Trade and purchase discounts; the gross method and the net method compared [LO8-3] Skip to question [The following information applies to the questions displayed below.] Tracy Company, a manufacturer of air conditioners, sold 100 units to Thomas Company on November 17, 2021. The units have a list price of $500 each, but Thomas was given a 30% trade discount. The terms of the sale were 2/10, n/30. Thomas uses a perpetual inventory system. Exercise 8-11 (Static) Part 3 Prepare the journal entries to record the purchase by Thomas on November 17 and payment on November 26, 2021, and December 15, 2021 using the net method of accounting for purchase discounts.   Explanation 3. November 17, 2021 Inventory: 98% × $35,000 = $34,300 December 15, 2021 Purchase discounts lost: 2% × $35,000 = $700. Required information Exercise 8-14 (Static) Inventory cost flow methods; perpetual system [LO8-1, 8-4] Skip to question [The following information applies to the questions displayed below.] Altira Corporation provides the following information related to its merchandise inventory during the month of August 2021:

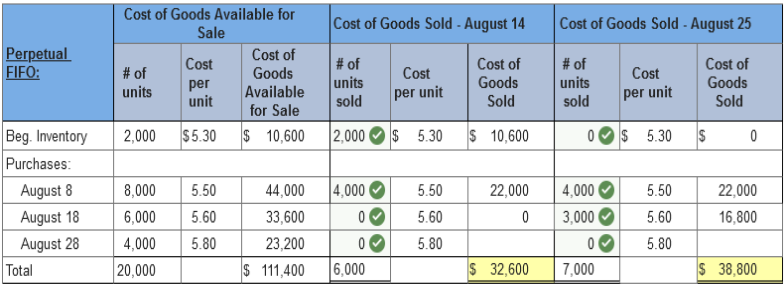

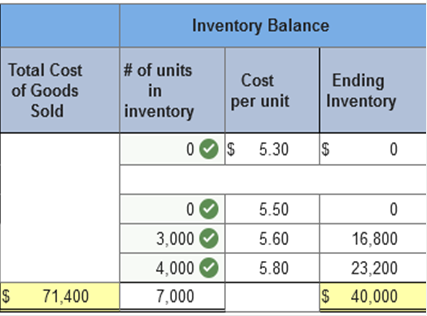

Required: 1. Using calculations based on a perpetual inventory system, determine the inventory balance Altira would report in its August 31, 2021, balance sheet and the cost of goods sold it would report in its August 2021 income statement using the FIFO method.   Explanation 1. First-in, first-out (FIFO) Cost of goods sold:

Ending inventory = (3,000 units × $5.60) + (4,000 units × $5.80) = $40,000 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11

| Final Exam

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |