|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Intermediate Accounting (ACG 3101) Homework 6 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11 | Final Exam

What account tracks the inflow of

net assets that occurs when a business provides goods or services to its

customers?

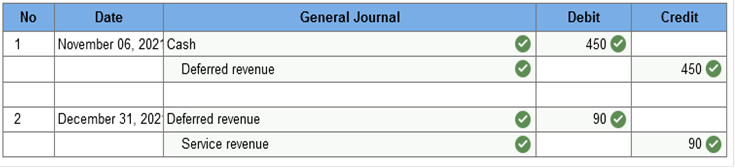

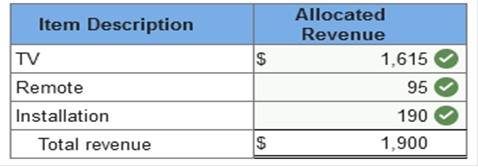

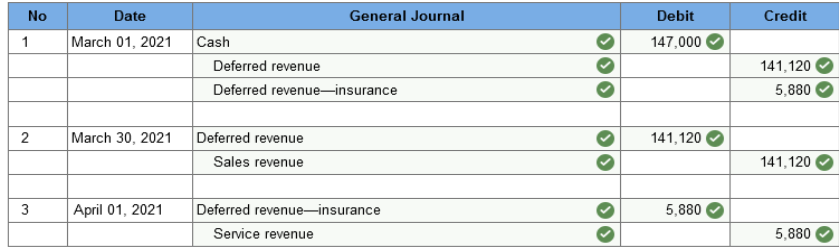

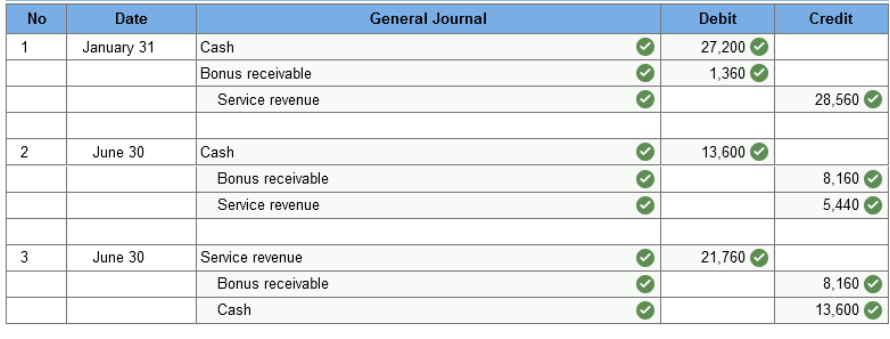

revenues The core revenue recognition principle stipulates that companies recognize revenue when goods or services are transferred to customers Which of the following likely will lead to revenue recognition at a point in time? (Select all that apply.) Buyer has accepted the asset Buyer has legal title to the asset Which of the following services are commonly performed over time? (Select all that apply.) Consulting engagements Financial statement audits Lending of money What method(s) can be used to estimate progress toward completion for the purpose of recognizing revenue over time? (Select all that apply.) Input method Output method The inflow of cash or other assets that a business receives when it provides goods or services to customers is referred to as revenues For a promise to provide a good or service to be accounted for as a separate performance obligation, the good or service must be distinct from other goods and services in the contract. The concept or principle that states that companies should recognize revenue when goods or services are transferred to customers for the amount the company expects to be entitled to receive in exchange for goods and services is referred to as the: Core revenue recognition principle The transaction price is the amount the seller expects to ______ from the customer in exchange for providing goods and services. be entitled to receive. Which of the following are key indicators that control of goods or services has been transferred to the customer? (Select all that apply.) Customer has legal title to the asset Customer has physical possession of the asset Customer accepted asset. The amount at which a good or service is sold separately under similar circumstances is referred to as the stand-alone selling price. Revenue recognition for services such as lending money and performing financial statement audits is typically ___. over time Arthur Inc. provides services to consulting clients. Arthur should recognize the related revenue when _____. the related performance obligation is satisfied. Methods that can be used to estimate progress toward completion are referred to as (1)-based and (2)-based methods. (Enter one word per blank.) output input A contract is an agreement that creates ____ enforceable rights and obligations. (Enter only one word.) legally Which of the following support(s) the conceptual basis for separating contractual promises into several performance obligations? Financial statements better reflect timing of transfer of goods and services Promises that can be viewed on a stand-alone basis should be separated. A prepayment from a customer typically creates a performance obligation. False The _____ price is the amount the seller expects to be entitled to receive from the customer in exchange for providing goods and services. transaction Which of the following are indicators that a company is a principal? (Select all that apply.) it sets the sales price It has primary responsibility for providing the product or service it owns the inventory prior to delivery For the purpose of allocating the transaction price to multiple performance obligations, the stand-alone selling price of a specific good or service may be estimated if it cannot be directly observed. Which methods may be used to estimate the stand-alone prices of goods and services? (Select all that apply.) Expected cost plus margin approach Adjusted market assessment approach Residual approach Revenue is recognized when the ____ obligation is satisfied. (Enter one word.) performance Commitment to performing an obligation and enforcing related rights represents a critical aspect of a(n) contract contract Licenses typically allow customers to use the seller's ____ property. Intellectual Jones Company receives a prepayment from a customer consistent with a promise to deliver 20 new office printers to Smith Inc. The prepayment should be recorded as deferred revenue does not create a separate performance obligation. Which of the following must a seller recognize as separate line items on the balance sheet? (Select all that apply.) Contract liabilities Accounts receivable Contract assets Principal Has primary responsibility for delivering goods or services. Agent Acts as a facilitator for helping seller transact with buyers. Third Party Is not directly involved in a transaction. Munch Inc. delivers various types of construction materials to a customer's building site. Over an 18-month period, Munch's employees utilize Munch's machinery and tools to construct a new office. building for the customer. Munch identifies only one performance obligation related to this contract because Munch combines the materials, labor, and use of machinery and tools to construct a single complete building. The stand-alone price of a good or service may be estimated using the adjusted market assessment approach, the expected cost-plus margin approach, or the ____ approach. (Enter only one word.) residual Which of the following are included in the journal entry required to record construction costs for a long-term construction contract? (Select all that apply.) debit construction in progress credit raw materials Which statements are true regarding revenue recognition over time and upon completion? (Select all that apply.) The same total amount of gross profit is recognized under both methods. Revenue recognition over time provides a more realistic measure of a project's periodic performance. Agreements that allow customers to use the seller's intellectual property are referred to as ____. (Enter only one word.) licenses An estimated overall loss on a long-term contract is fully recognized in the first period the loss becomes evident, regardless of the revenue recognition method used. True A seller recognizes contract liabilities, contract assets, and accounts receivable on separate lines of its ____ ____. (Enter one word per blank.) Balance, sheet Long-term contracts require careful consideration in identifying performance obligations because these type of contracts… typically include many products and services that _____. could be viewed as separate performance obligations. What journal entry should be made to recognize accounts receivable for long-term construction projects? Debit Accounts Receivable Credit Billings on Construction Contract The essential difference between revenue recognition over time and upon completion relates to the pattern of recognition of the related gross profit. Required information Learning Objective 06-04 Allocate a contract’s transaction price to multiple performance obligations. Skip to question [The following information applies to the questions displayed below.] A contract’s transaction price is allocated to its performance obligations. The allocation is based on the stand-alone selling prices of the goods and services underlying those performance obligations. The standalone selling price must be estimated if a good or service is not sold separately. Which of the following is one of the steps used to apply the revenue recognizing principle? Identify the performance obligation(s) in the contract? Required information Learning Objective 06-05 Determine whether a contract exists, and whether some frequently encountered features of contracts, qualify as performance obligations. Skip to question [The following information applies to the questions displayed below.] A contract exists when it has commercial substance and all parties to the contract are committed to performing the obligations and enforcing the rights that it specifies. Performance obligations are promises by the seller to transfer goods or services to a customer. A promise to transfer a good or service is a separate performance obligation if it is distinct, which is the case if it is both capable of being Prepayments, rights to return merchandise, and normal quality-assurance warranties do not qualify as performance Which of the following is a performance obligation? Extended warranty on the electronics package of a car Required information Learning Objective 06-06 Understand how variable consideration and other aspects of contracts affect the calculation, and allocation of the transaction price. Skip to question [The following information applies to the questions displayed below.] When a contract includes consideration that depends on the outcome of future events, sellers estimate that variable consideration and include it in the contract’s transaction price. The seller’s estimate is based either on the most likely outcome or the expected value of the outcome. However, a constraint applies—variable consideration only should be included in the transaction price to the extent it is probable that a significant revenue reversal will not occur. The estimate of variable consideration is updated each period to reflect changes in circumstances. A seller also needs to determine if it is a principal (and recognizes as revenue the amount received from the customer) or an agent (and recognizes its commission as revenue), consider time value of money, and consider the effect of any payments by the seller to the customer. Once the transaction price is estimated, we allocate it to performance obligations according which can be estimated using the adjusted market assessment approach, the expected cost plus margin or the residual approach. Which of the following statements is true with regards to variable consideration? Variable consideration means the transaction price is uncertain. Which is correct regarding changes in estimated variable consideration? Changes in estimated variable consideration should be recognized as an adjustment to revenue in the period the change in estimate is made. Which of the following is true regarding an agent? The agent's revenue is equal to the commission it is entitled to receive on each transaction. Required information Learning Objective 06-09 Demonstrate revenue recognition for long-term contracts, both at a point in time when the contract is completed and over a period of time according to the percentage completed. Skip to question [The following information applies to the questions displayed below.] Long-term contracts usually qualify for revenue recognition over time. We recognize revenue over time by assigning a share of the project’s revenues If long-term contracts What is the relationship between Construction-in-progress (CIP) and the Billings on Construction Contract account? Billings is contra to CIP and reduces the balance of the CIP account. When revenues, costs and gross profit are recognized at the completion of the contract rather than periodically throughout the contract: Either method results in the same revenues, costs and gross profits being recognized by the end of the project. If a contract qualifies for revenue recognition over time, revenue is recognized based on progress toward: Completion. When is a loss recognized on a long-term contract? In the first period in which the loss becomes evident. Exercise 6-2 (Static) Service revenue [LO6-3] Ski West, Inc., operates a downhill ski area near Lake Tahoe, California. An all-day adult lift ticket can be purchased for $85. Adult customers also can purchase a season pass that entitles the pass holder to ski any day during the season, which typically runs from December 1, The company’s fiscal year ends on December 31. On November 6, 2021, Jake Lawson purchased a season pass for $450. Required: When should Ski West recognize revenue from the sale of its season passes? Prepare the appropriate journal entries that Ski West would record on November 6 and December 31. What will be included in the Ski West 2021 income statement and balance sheet related to the sale of the season pass to Jake Lawson?    Exercise 6-3 (Static) Allocating transaction price [LO6-4] Video Planet (VP) sells a big screen TV package consisting of a 60-inch plasma TV, a universal remote, and on-site installation by VP staff. The installation includes programming the remote to have the TV interface with other parts of the customer’s home entertainment system. VP concludes that the TV, remote, and installation service are separate performance obligations. VP sells the 60-inch TV separately for $1,700, Required: How much revenue would be allocated to the TV, the remote, and the installation service? (Do not round intermediate calculations.)  Exercise 6-5 (Static) Performance obligations [LO6-2, 6-4, 6-5] On March 1, 2021, Gold Examiner receives $147,000 from a local bank and promises to deliver 100 units of certified 1-oz. gold bars on a future date. The contract states that ownership passes to the bank when Gold Examiner delivers the products to Brink’s, a third-party carrier. In addition, The stand-alone price of a gold Brink’s picked Required: 1. How many performance obligations are in this contract? 2. to 4. Prepare the journal entry Gold Examiner would record on March 1, March 30 and April 1.   Problem 6-5 (Algo) Variable consideration [LO6-3, 6-6] On January 1, Revis Consulting entered into a contract to complete a cost reduction program for Green Financial over a six-month period. Revis will receive $27,200 from Green at the end of each month. If total cost savings reach a specific target, Revis will receive an additional $13,600 from Green at the end of the contract, but if total cost savings fall short, Revis will refund $13,600 to Green. Revis estimates an 80% chance that Required: Prepare the following journal entries for Revis: 1. to 3. Prepare the journal entry on January 31 to record the collection of cash and recognition of the first month’s revenue. Also record the entry on June 30 for receipt of the bonus assuming total cost savings exceed target. And record the entry on June 30 for payment of the penalty assuming total cost savings fall short of target. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)  Problem 6-11 (Algo) Long-term contract; revenue recognition upon completion [LO6-9] In 2021, the Westgate Construction Company entered into a contract to construct a road for Santa Clara County for $10,000,000. The road was completed in 2023. Information related to the contract is as follows:

Assume that Westgate Construction’s contract with Santa Clara County does not qualify for revenue recognition over time. Required: 1. Calculate the amount of revenue and gross profit (loss) to be recognized in each of the three years. 2-a. In the journal below, complete the necessary journal entries for the year 2021 (credit "Various accounts" for construction costs incurred). 2-b. In the journal below, complete the necessary journal entries for the year 2022 (credit "Various accounts" for construction costs incurred). 2-c. In the journal below, complete the necessary journal entries for the year 2023 (credit "Various accounts" for construction costs incurred). 3. Complete the information required below to prepare a partial balance sheet for 2021 and 2022 showing any items related to the contract. 4. Calculate the amount of revenue and gross profit (loss) to be recognized in each of the three years assuming the following costs incurred

5. Calculate the amount of revenue and gross profit (loss) to be recognized in each of the three years assuming the following costs incurred and costs to complete information.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers pay one-third of the sales price of a jet ski Because Lake has little information Lake collected $360,000 in 2020, $360,000 in 2021, and $360,000 Lake sold jet skis with a total price of $2,010,000 that cost Lake $1,206,000. Lake collected $480,000 in 2022, and $480,000 in 2023 associated with those sales. In 2023, Lake also repossessed $380,000 of jet skis that were sold in 2021. Those jet skis had a fair value of $142,500 at the time they were repossessed. Total cash collections on installment sales during 2021 would be: $1,030,000 Explanation $360,000 (2020 sales) + $670,000 (2021 sales) = $1,030,000 Revenue always is recognized once the buyer has physical possession of goods. False TB TF Qu. 6-62 (Static) When recognizing revenue over time on a... When recognizing revenue over time on a long-term contract, amounts billed and the cash actually received affect income recognition. False TB TF Qu. 6-18 (Static) If the contract is not in writing, revenue... If the contract is not in writing, revenue cannot be recognized, even though goods have been transferred and payment is expected to be received in exchange. False TB TF Qu. 6-28 (Static) To account for variable consideration using... To account for variable consideration using the most likely amount, the probability of each possible amount is multiplied by the possible amount to get an expected contract price. False TB TF Qu. 6-17 (Static) A contract between a seller and a buyer... A contract between a seller and a buyer need not be in writing to be enforceable. True TB MC Qu. 6-121 (Static) Which of the following statement is most true? Calculate cost of goods sold for the year ended August Variable consideration means that the transaction price is uncertain. Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11

| Final Exam

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |