|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Intermediate Accounting (ACG 3101) Homework 4 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11 | Final Exam

The distinction between

operating and nonoperating activities relate to the:

Primary activities of the business. Learning Objective 04-01 Discuss the importance of income from continuing operations and describe its components. [The following information applies to the questions displayed below.] The components of income from continuing operations are revenues, expenses (including income taxes), gains, and losses, excluding those related to discontinued operations. Companies often distinguish between operating and nonoperating income within continuing operations. Income statement formats Knowledge Check 01 Which of the following statements are correct regarding the two income statement formats? (Select all that apply.) Check All That Apply No specific standard dictates the format of the income statement. Companies usually report income tax expense in a separate line in the income statement regardless of the format used. The multiple-step format provides information that might be useful in analyzing trends. Explanation Although the items are grouped differently, therefore subtracted in a specific order, once net income is reached, it is the same under both presentation formats. Which of the following is likely to be part of temporary earnings? Loss on the sale of investments. the discontinued component had operating income of $4,000,000. At the time of the sale, the assets of the discontinued component had book values of $10,000,000 and were sold for $12,000,000. Income from operations of the continuing parts of the company were $14,000,000 for the year. Assuming a 40% tax rate, what amount would Merrell report as income from discontinued operations? $3,600,000 Explanation Knowledge Check 01

Learning Objective 04-05 Discuss additional reporting issues related to accounting changes, error corrections, and earnings per share (EPS). Accounting changes include changes in principle, changes in estimate, or changes in reporting entity. Their effects on the current period and prior period financial statements are reported using various approaches— retrospective, modified retrospective, and prospective. Error corrections are made by restating prior period financial statements. Any correction to retained earnings is made with an adjustment to the beginning balance in the current period. Earnings per share (EPS) is the amount of income achieved during a period expressed per share of common stock outstanding. EPS must be disclosed for income from continuing operations and for discontinued operations. Taylor Company purchased a machine and plans to depreciate it over its estimated useful life of 10 years. Over the next four years, the machine was used more extensively than originally estimated, so Taylor revised the useful life estimate to a total of 8 years. This change should be accounted for as a: Change in accounting estimate, with a prospective approach. The correction of an error in the financial statement of a prior period should be reported: As an adjustment to the beginning balance of retained earnings in the statement of shareholders’ equity. Alpha Company has sales revenue of $5,000,000, cost of goods sold of $2,000,000, and net income of $750,000. For the last three years, the company has 1,000,000 shares of common stock authorized and 200,000 shares of common stock issued and outstanding. The company does not have any preferred stock. What is basic EPS for Alpha Company?  Explanation Basic EPS is calculated as net income minus preferred dividends, divided by the weighted-average number of common stock shares outstanding. Net income is $750,000, there are no preferred dividends, and there are 200,000 shares of common stock outstanding throughout the year. EPS = $750,000 ÷ 200,000 shares = $3.75 per share Which of the following activities affects operating cash inflows? Selling 100 units of inventory for cash. Sale of the old factory after the company moves into a new factory.

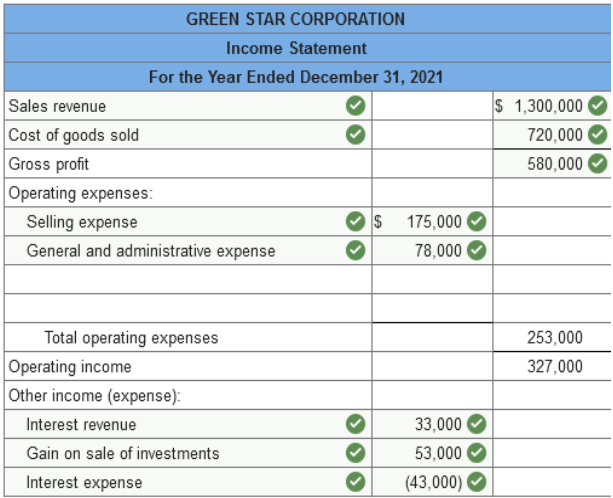

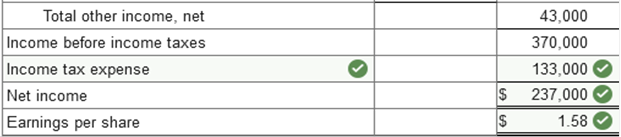

What are Fortuna’s total cash outflows for financing activities?  (Select all that apply) Statement of Operations Statement of Changes in Financial Position Statement of Business Activities Statement of Earnings (Select all that apply.) Expenses Losses Revenues Gains Which of the following items are included in calculating operating income? (Select all that apply.) revenues related to primary revenue-generating activities expenses related to primary revenue-generating activities Multiple choice question. As part of other expenses. As a separate line item. As part of general expenses. operating and nonoperating single-step and multiple-step current and noncurrent direct and indirect Statement of Performance Indicators Statement of Business Activities Statement of Operations Statement of Cash Flows (Enter only one word per blank.) Temporary, permanent ABC Tax Advisors - Service Revenue Best Buy - Sales revenue earnings may not increase more than 10% without a penalty. income is averaged with historical numbers. earnings have a steady stream over time. income is deferred until contractual relations are negotiated. (Select all that apply.) revenues selling expenses interest expense administrative expenses in which the business is conducted are called _________________ costs restructuring Multiple choice question. In extraordinary gains and losses. In other comprehensive income. In a separate line. In other expenses. Multiple choice question. they are netted against cost of goods sold. they are often nonrecurring. the gains were included in revenues. they are often recurring. The two approaches for preparing an income statement are the __________ step and _________________ step approaches. Single Multi Non-GAAP earnings are calculated Multiple choice question. based on assets that are expected to be converted to cash in the next operating cycle. based on historical cost assumptions. based on statistical analysis of time series data. based on management's assumptions of permanent earnings. Analyzing earnings quality requires an analyst to Multiple choice question. separate a company's temporary and permanent earnings. score a company based on its historical earnings. combine all earnings for analysis. determine whether the auditor was correct in calculating earnings. If discontinued operations have a _____ effect on the income statement, they must be reported separately. Multiple choice question. negative positive minimal material Income smoothing describes the concept that. managers manipulate the pattern of income to not vary much between years. income is averaged over a 10-year moving average. income is not reported until approved by the board of directors. A discontinued operation is reported when a ___________________ of an entity either (a) has been disposed of or (b) is classified as held for sale. (Enter one word per blank) component _____ costs include costs associated with shutdown or relocation of facilities. Multiple choice question. Refunding Restructuring Moving Closing If a component of the business qualifies for discontinued operations treatment, which of the following statements are true? (Select all that apply.) Revenue from the discontinued operations is listed immediately below revenue in the operating section of the income statement. The tax expense effect is removed from continuing operations. All related revenues, expenses, gains, and losses must be removed from continuing operations. Revenues and expenses are reported in continuing operations, but gains and losses are reported as discontinued operations. Nonoperating items that are not expected to continue into the future are considered a ______ component of earnings and should be __________ when forecasting future performance. temporary; included permanent; included temporary; excluded permanent; excluded Which of the following is a category of accounting change? Liability classification Reporting entity Reporting class Entity classification Management's assessment of permanent earnings are referred to as what? Income from continuing operations Non-GAAP earnings Perpetual income Net income When an immaterial error is discovered in the same year it is made before the financial statements are issued, what is the appropriate course of action? Reverse the erroneous journal entry, record the correct entry, and include a note to the financial statements. Reverse the erroneous journal entry, record the correct entry, include a note to the financial statements, and report the error to the authorities. Reverse the erroneous journal entry and record the correct entry. How are discontinued operations reported? (Select all that apply.) As a separate line item on the income statement. With separate reporting of the tax effect on the item of discontinued operations. Above income from continuing operations. Below income from continuing operations. With tax on the discontinued operation included in total income tax expense. Basic earnings per share is calculated as net income available to common shareholders divided by average stockholders' equity. average total assets. ending retained earnings. weighted average common shares outstanding. To qualify as an operation for purposes of determining discontinued operations, which of the following must occur? (Select all that apply.) The operation must have been in business for more than 3 years. A strategic shift is represented that will have a major effect on financial results. A component of the entity has been sold, disposed of, or is held for sale. The operation must have completed a separate tax return in the past 2 years. Net income is a part of comprehensive income gross income cost of goods sold gross margin Revenues, expenses, gains, losses, and income tax related to a(n) ________________ __________________must be removed from continuing operations and reported separately on the income statement. Discontinued operations The potential tax expense or benefits of items reported as components of Other Comprehensive Income must be aggregated for all items and reported as one line item can be shown separately for each item or aggregated and reported as one line item must be presented separately for each item The three types of accounting changes are a change in - accounting principle. - accounting estimate. - reporting entity. Accumulated other comprehensive income represents the total of other comprehensive income to date. The majority of errors discovered are not _______________, and are corrected in the year discovered. material U.S. GAAP requires that a statement of cash flows must be presented for a. each period for which a balance sheet and income statement are prepared. b. every reporting period to date. c. each period in which an income statement is not prepared. Which of the following is computed by dividing income available to common shareholders by the weighted-average number of common shares outstanding? a. Return on equity b. Diluted earnings per share c. Basic earnings per share d. Price to earnings The statement of cash flows is useful because - it reveals the company's ability to generate positive cash flow from its normal operations - it provides information about liquidity Net income is a portion of comprehensive income. True The classifications on the statement of cash flows are cash flows from - financing activities. - investing activities. - operating activities. Which of the following are acceptable methods for reporting comprehensive income? (Select all that apply.) In one single statement of comprehensive income in two consecutive statements - income statement and comprehensive income statement Where are the elements of net income found on a cash basis rather than an accrual basis? Operating activities section of the statement of cash flows Other comprehensive income is reported in the current reporting period on the income statement or as an addition to the income statement, and _________________ other comprehensive income is reported on the balance sheet. (Enter only one word.) accumulated Cash flows from ____ activities are related to the purchase and sale of long-term assets used in business operations. (Enter only one word.) investing The financial statement that provides information about cash receipts and cash disbursements for the period is the statement of cash flows. Which type of activities involve cash inflows and outflows from transactions with creditors and owners? Financing The statement of cash flows is useful because accrual-based income is not an indication of cash flows. Which is a significant noncash activity? Signing a note payable in exchange for land. The statement of cash flows classifies items as operating, investing, and financing. What is the formula for the asset turnover ratio? Net sales divided by average total assets. The operating activities section on the statement of cash flows includes the elements of net income on a(n) ________________ basis rather than a(n) __________________ basis. (Enter one word per blank.) Cash, Accrual Financial statements covering periods of less than one year are called _________ interim reports Investing activities involve the acquisition and sale of (Select all that apply.) inventories sold in normal operations. long-lived assets used in business operations. nonoperating investment assets. financing Some _____ recognition is modified in interim reporting to cause interim statements to relate better to annual statements. expense or cost Which of the following are significant noncash activities? Acquiring equipment by issuing a long-term note. Acquiring land by issuing common stock. How are discontinued operations and unusual items treated in interim financial statements under U.S. GAAP? The full amount should be separately reported in the period in which the discontinued operation or unusual item occurs. Gulf Corp. has the following information: End of Year 1 Net sales $ 80,000 Total assets 600,000 Accounts receivable 30,000 End of Year 1 Net sales $ 100,000 Total assets 800,000 Accounts receivable 50,000 What is the asset turnover ratio for year 2 rounded to the nearest 1/1000? 0.143 Computations for EPS for interim reports under U.S. GAAP are based on what? Conditions actually existing during the particular interim period. quarterly When an accounting change occurs during an interim period, the change is applied retrospectively. In subsequent interim periods of the same fiscal year, which of the following are disclosed? (Select all that apply.) - Affect on income from continuing operations. - Affect on related per share amounts. - Affect on net income. Which of the following are required minimum disclosures in interim financial statements? (Select all that apply.) - contingencies - Net income - Sales Which of the following would require modified accounting treatment for interim reporting under U.S. GAAP? (Select all that apply.) - Advertising expenses incurred in the second quarter that will benefit the remainder of the year. - Property taxes paid in January for the entire year assessment. The treatment of discontinued operations and unusual items in interim reporting under U.S. GAAP is more consistent with the _____ view. discrete The earnings per share calculation for interim financial reporting under U.S. GAAP is consistent with which view? Discrete view Accounting changes made in an interim period are reported retrospectively Which of the following are required minimum disclosures in interim financial statements? (Select all that apply.) Significant changes in financial position Changes in accounting principles Fair value of financial instruments When an expense benefits more than just the period in which it is incurred, how is the expense treated under U.S. GAAP? The expense should be allocated among the periods benefited. Exercise 4-2 (Algo) Income statement format; single step and multiple step [LO4-1, 4-5] The following is a partial trial balance for the Green Star Corporation as of December 31, 2021:

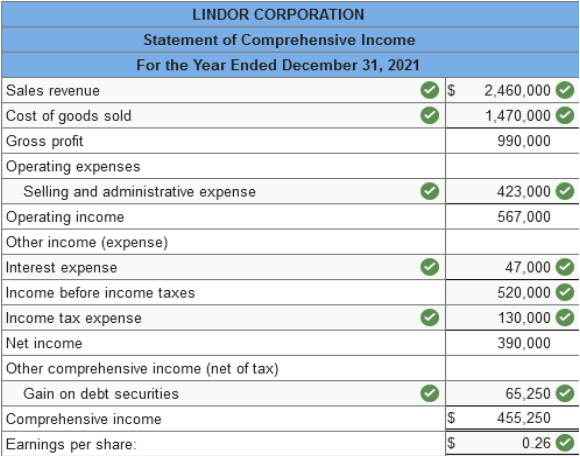

There were 150,000 shares of common stock outstanding throughout 2021. Required: Prepare a single-step income statement for 2021, including EPS disclosures. Prepare a multiple-step income statement for 2021, including EPS disclosures. Prepare a single-step income statement for 2021, including EPS disclosures. (Round EPS answer to 2 decimal places.) Prepare a multiple-step income statement for 2021, including EPS disclosures. (Amounts to be deducted should be indicated with a minus sign. Round EPS answer to 2 decimal places.)   The trial balance for Lindor Corporation, a manufacturing company, for the year ended December 31, 2021, included the following accounts:

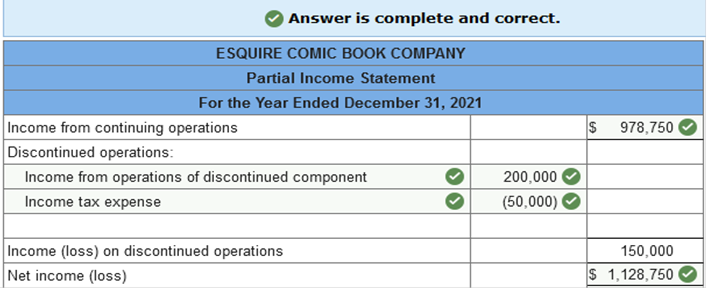

The gain on debt securities is unrealized and classified as other comprehensive income. The trial balance does not include the accrual for income taxes. Lindor's income tax rate is 25%. There were 1,500,000 shares of common stock outstanding throughout 2021. Required: Prepare a single, continuous multiple-step statement of comprehensive income for 2021, including appropriate EPS disclosures. (Round EPS answer to 2 decimal places.)  Explanation Income tax expense = $520,000 × 25% = $130,000 Gain on debt securities = $87,000 − ($87,000 × 25%) Exercise 4-7 (Algo) Income statement presentation; discontinued operations; restructuring costs [LO4-1, 4-3, 4-4] Esquire Comic Book Company had income before tax of $1,400,000 in 2021 before considering the following material items: Esquire sold one of its operating divisions, which qualified as a separate component according to generally accepted accounting principles. The before-tax loss on disposal was $380,000. The division generated before-tax income from operations from the beginning of the year through disposal of $580,000. The company incurred restructuring costs of $95,000 during the year. Required: Prepare a 2021 income statement for Esquire beginning with income from continuing operations. Assume an income tax rate of 25%. Ignore EPS disclosures. (Amounts to be deducted should be indicated with a minus sign.)  Explanation Income from operations of discontinued component (including loss on disposal of $380,000) = $200,000 Income from continuing operations:

Exercise 4-9 (Algo) Discontinued operations; disposal in subsequent year; solving for unknown [LO4-4] On September 17, 2021, Ziltech, Inc., entered into an agreement to sell one of its divisions that qualifies as a component of the entity according to generally accepted accounting principles. By December 31, 2021, the company’s fiscal year-end, the division had not yet been sold, but was considered held for sale. The net fair value (fair value minus costs to sell) of the division’s assets at the end of the year was $16 million. The pretax income from operations of the division during 2021 was $6 million. Pretax income from continuing operations for the year totaled $19 million. The income tax rate is 25%. Ziltech reported net income for the year of $9.0 million. Required: Determine the book value of the division's assets on December 31, 2021. (Enter your answer in whole dollars not in millions.)  Explanation

$5,250,000 ÷ 75%* = $7,000,000 = Pretax loss from discontinued operations. *1 − tax rate of 25% = 75%

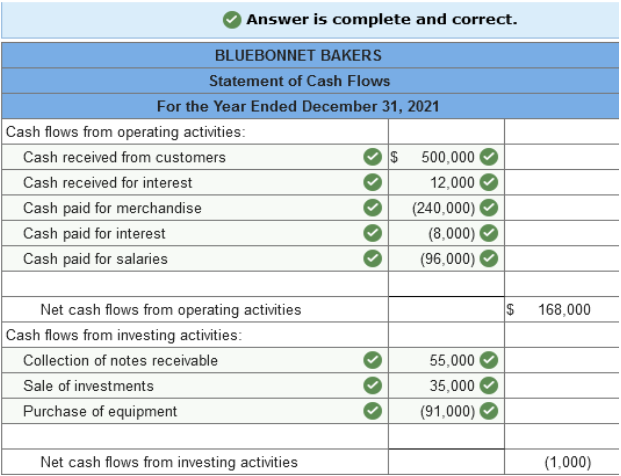

Exercise 4-13 (Algo) Statement of cash flows preparation; direct method [LO4-8] The following summary transactions occurred during 2021 for Bluebonnet Bakers:

The balance of cash and cash equivalents at the beginning of 2021 was $27,000. Required: Prepare a statement of cash flows for 2021 for Bluebonnet Bakers. Use the direct method for reporting operating activities. (Amounts to be deducted should be indicated with a minus sign.)   The accounting records of Hampton Company provided the data below ($ in thousands).

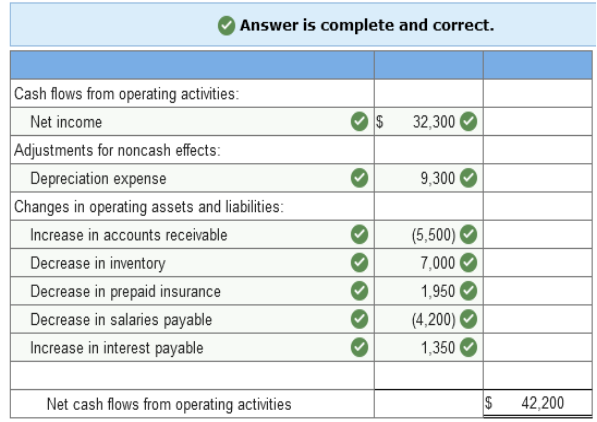

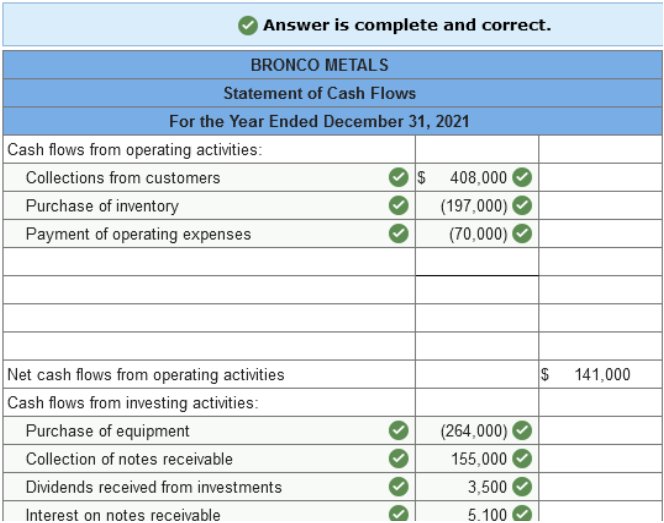

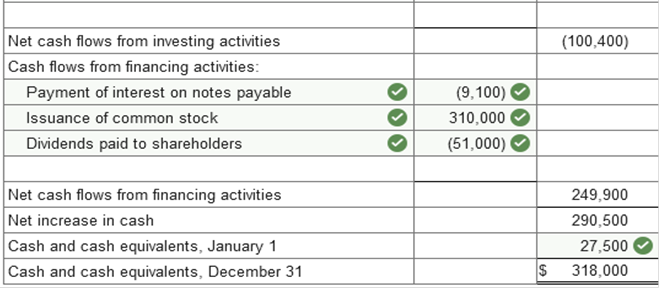

Required: Prepare a reconciliation of net income to net cash flows from operating activities. (Amounts to be deducted should be indicated with a minus sign. Enter your answers in thousands.)  Exercise 4-19 (Algo) IFRS; statement of cash flows [LO4-8, 4-9] The statement of cash flows for the year ended December 31, 2021, for Bronco Metals is presented below.

Required: Prepare the statement of cash flows assuming that Bronco prepares its financial statements according to International Financial Reporting Standards. Where IFRS allows flexibility, use the classification used most often in IFRS financial statements. (Amounts to be deducted should be indicated with a minus sign.)   Explanation Consistent with U.S. GAAP, international standards also require a statement of cash flows. Consistent with U.S. GAAP, cash flows are classified as operating, investing, or financing. However, the U.S. standard designates cash outflows for interest payments and cash inflows from interest and dividends received as operating cash flows. Dividends paid to shareholders are classified as financing cash flows. IAS No. 7, on the other hand, allows more flexibility. Companies can report interest and dividends paid as either operating or financing cash flows and interest and dividends received as either operating or investing cash flows. Interest and dividend payments usually are reported as financing activities. Interest and dividends received normally are classified as investing activities. TB MC Qu. 4-109 (Static) Shively Mfg. Co. sold... Shively Mfg. Co. sold for $18,000 equipment that cost $40,000 and had a book value of $30,000. Shively would report: Investing cash inflows of $18,000. Provincial would report the following amount of income tax expense as a separately stated line item in the income statement: $150,000. Explanation ($700,000 − $100,000) × 25% = $150,000 The Claxton Company manufactures children's toys and also has a division that makes automobile parts. Due to a change in its strategic focus, the company sold the automobile parts division. The division qualifies as a component of the entity according to GAAP. How should Claxton report the sale in its income statement? Report the income or loss from operations of the division in discontinued operations. Major Co. reported 2021 income of $307,000 from continuing operations before income taxes and a before-tax loss on discontinued operations of $73,000. All income is subject to a 25% tax rate. In the income statement for the year ended December 31, 2021, Major Co. would show the following line-item amounts for income tax expense and net income: $76,750 and $175,500 respectively. Explanation

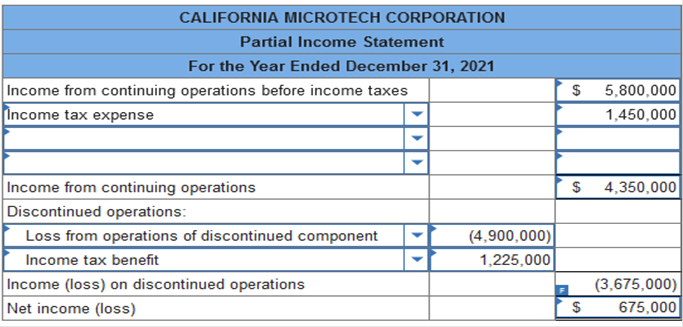

Which of the following is added to net income as an adjustment under the indirect method of preparing the statement of cash flows? Loss on the sale of equipment. Intraperiod income tax presentation is primarily a matter of: Allocation. Brief Exercise 4-9 (Algo) Discontinued operations [LO4-4] The semiconductor business of the California Microtech Corporation qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $15 million. The loss from operations of the segment during 2021 was $3.90 million. Pretax income from continuing operations for the year totaled $5.80 million. The income tax rate is 25%. Assume instead that the estimated fair value of the segment’s assets, less costs to sell, on December 31 was $14 million rather than $15 million. Prepare the lower portion of the 2021 income statement beginning with income from continuing operations before income taxes. Ignore EPS disclosures. (Amounts to be deducted and negative amounts should be indicated with a minus sign. Enter your answers in whole dollars and not in millions.)  Explanation Income tax expense = $5,800,000 × 25% = $1,450,000 Loss from operations of discontinued component:

Income tax benefit = ($4,900,000) × 25% = $1,225,000 The following are summary cash transactions that occurred during the year for Hilliard Healthcare Co. (HHC):

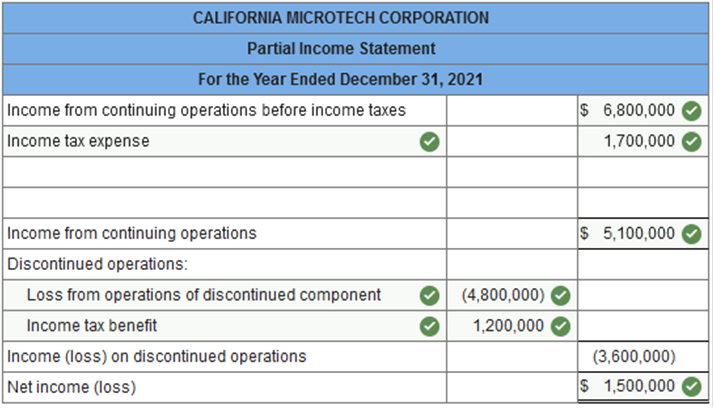

Prepare a statement of cash flows according to International Financial Reporting Standards. (Amounts to be deducted should be indicated with a minus sign.)  Explanation Under IFRS, interest received and interest paid usually are classified as investing and financing cash flows, respectively, not operating cash flows as with U.S. GAAP. Brief Exercise 4-8 (Algo) Discontinued operations [LO4-4] The semiconductor business of the California Microtech Corporation qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $17 million. The loss from operations of the segment during 2021 was $4.8 million. Pretax income from continuing operations for the year totaled $6.8 million. The income tax rate is 25%. Assume that the semiconductor segment was not sold during 2021 but was held for sale at year-end. The estimated fair value of the segment’s assets, less costs to sell, on December 31 was $19 million. Prepare the lower portion of the 2021 income statement beginning with income from continuing operations before income taxes. Ignore EPS disclosures. (Amounts to be deducted and negative amounts should be indicated with a minus sign. Enter your answers in whole dollars and not in millions.)  Exercise 4-9 (Algo) Discontinued operations; disposal in subsequent year; solving for unknown [LO4-4] On September 17, 2021, Ziltech, Inc., entered into an agreement to sell one of its divisions that qualifies as a component of the entity according to generally accepted accounting principles. By December 31, 2021, the company’s fiscal year-end, the division had not yet been sold, but was considered held for sale. The net fair value (fair value minus costs to sell) of the division’s assets at the end of the year was $15 million. The pretax income from operations of the division during 2021 was $5 million. Pretax income from continuing operations for the year totaled $18 million. The income tax rate is 25%. Ziltech reported net income for the year of $8.7 million. Required: Determine the book value of the division's assets on December 31, 2021. (Enter your answer in whole dollars not in millions.)  Explanation

$4,800,000 ÷ 75%* = $6,400,000 = Pretax loss from discontinued operations. *1 − tax rate of 25% = 75%

TB MC Qu. 4-63 (Algo) On August 1, 2021, Rocket Retailers adopted a plan to... On August 1, 2021, Rocket Retailers adopted a plan to discontinue its catalog sales division, which qualifies as a separate component of the business according to GAAP regarding discontinued operations. The disposal of the division was expected to be concluded by June 30, 2022. On January 31, 2022, Rocket's fiscal year-end, the following information relative to the discontinued division was accumulated:

In its income statement for the year ended January 31, 2022, Rocket would report a before-tax loss on discontinued operations of: $(133,000) Explanation $(121,000) + $(12,000) = $(133,000) The FASB's stated preference for reporting operating cash flows is the: Direct method TB MC Qu. 4-64 (Algo) On November 1, 2021, Jamison Inc. adopted a plan to... On November 1, 2021, Jamison Inc. adopted a plan to discontinue its barge division, which qualifies as a separate component of the business according to GAAP regarding discontinued operations. The disposal of the division was expected to be concluded by April 30, 2022. On December 31, 2021, the company's year-end, the following information relative to the discontinued division was accumulated:

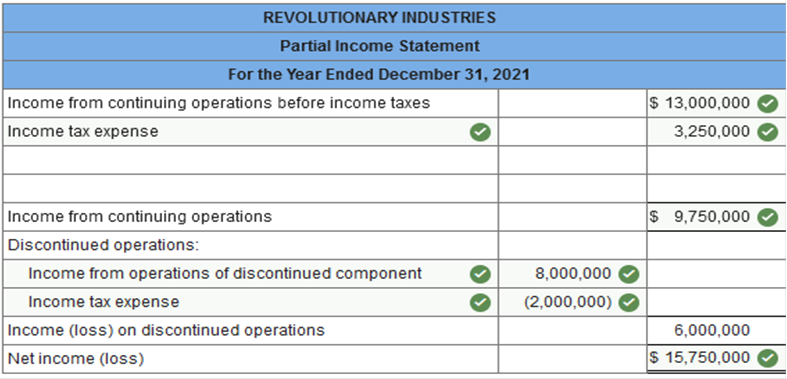

In its income statement for the year ended December 31, 2021, Jamison would report a before-tax loss on discontinued operations of: $66 million TB MC Qu. 4-104 (Algo) Schneider Inc. had salaries payable of... Schneider Inc. had salaries payable of $61,200 and $91,100 at the end of 2020 and 2021, respectively. During 2021, Schneider recorded $621,500 in salaries expense in its income statement. Cash outflows for salaries in 2021 were: $591,600. Explanation $621,500 – $29,900 increase in salaries payable = $591,600 Comprehensive income is the change in equity from: Nonowner transactions. Brief Exercise 4-6 (Algo) Discontinued operations [LO4-4] On December 31, 2021, the end of the fiscal year, Revolutionary Industries completed the sale of its robotics business for $11.0 million. The robotics business segment qualifies as a component of the entity according to GAAP. The book value of the assets of the segment was $8.0 million. The income from operations of the segment during 2021 was $5.0 million. Pretax income from continuing operations for the year totaled $13.0 million. The income tax rate is 25%. Prepare the lower portion of the 2021 income statement beginning with income from continuing operations before income taxes. Ignore EPS disclosures. (Amounts to be deducted and negative amounts should be indicated with a minus sign. Enter your answers in whole dollars and not in millions. For example, $4,000,000 rather than $4.)  Explanation Income tax expense = $13,000,000 × 25% = $3,250,000 Income from operations of discontinued component, before tax:

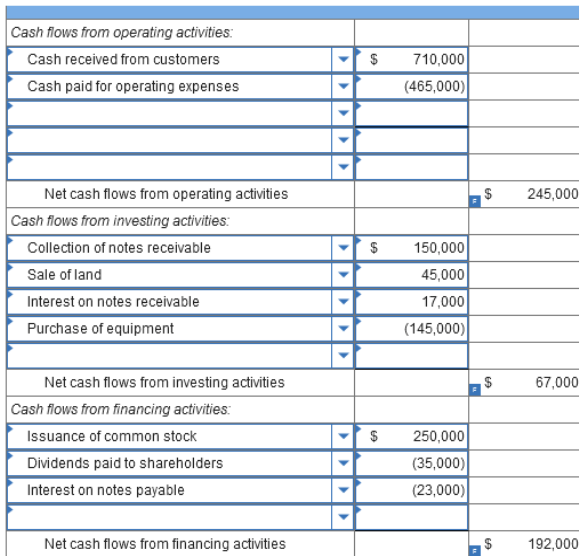

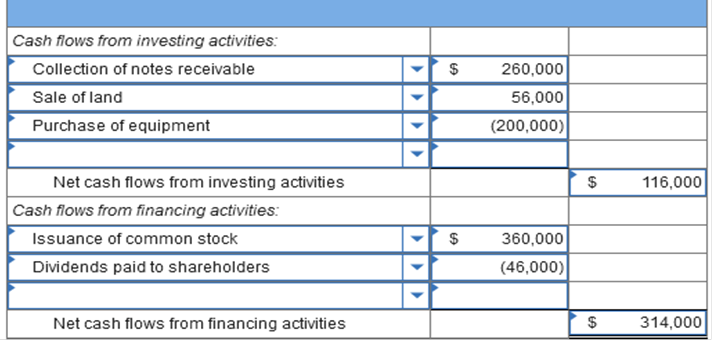

Income tax expense = $8,000,000 × 25% = $2,000,000 Brief Exercise 4-12 (Algo) Statement of cash flows; investing and financing activities [LO4-8] The following are summary cash transactions that occurred during the year for Hilliard Healthcare Co. (HHC):

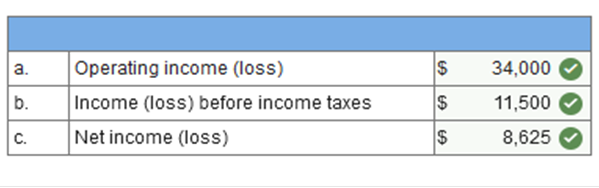

Prepare the cash flows from investing and financing activities sections of HHC’s statement of cash flows. (Amounts to be deducted should be indicated with a minus sign.)  Brief Exercise 4-4 (Algo) Multiple-step income statement [LO4-1, 4-3] The following is a partial year-end adjusted trial balance.

Income tax expense has not yet been recorded. The income tax rate is 25%. a. Determine the operating income (loss). b. Determine the income (loss) before income taxes. c. Determine the net income (loss).  Explanation a.

b.

c.

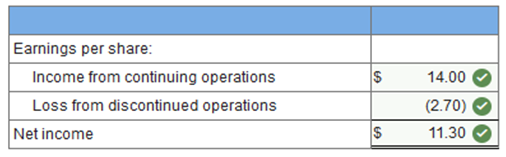

Exercise 4-10 (Algo) Earnings per share [LO4-5] The Esposito Import Company had 1 million shares of common stock outstanding during 2021. Its income statement reported the following items: income from continuing operations, $14 million; loss from discontinued operations, $2.7 million. All of these amounts are net of tax. Required: Prepare the 2021 EPS presentation for the Esposito Import Company. (Amounts to be deducted should be indicated with a minus sign. Round your answers to 2 decimal places.)  Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11

| Final Exam

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |