|

Accounting | Business | Computer

Science | General

Studies | Math | Sciences | Civics Exam | Help/Support | Join/Cancel | Contact Us | Login/Log Out

Intermediate Accounting (ACG 3101) Homework 2 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11 | Final Exam

Required information

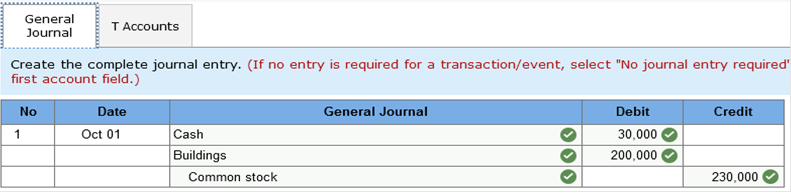

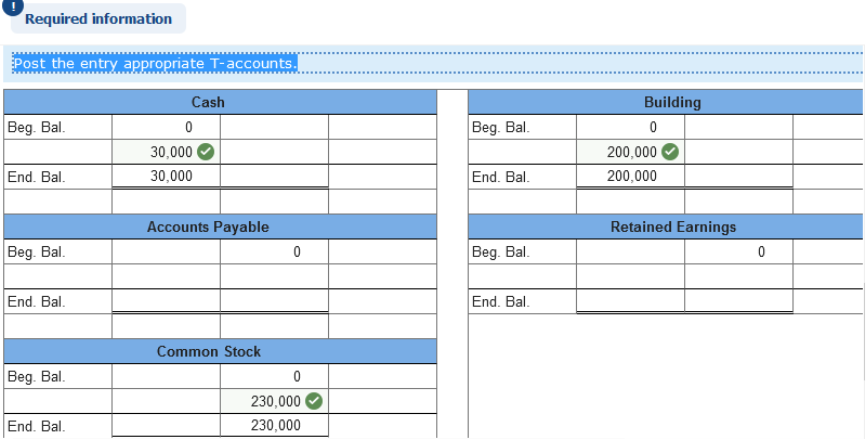

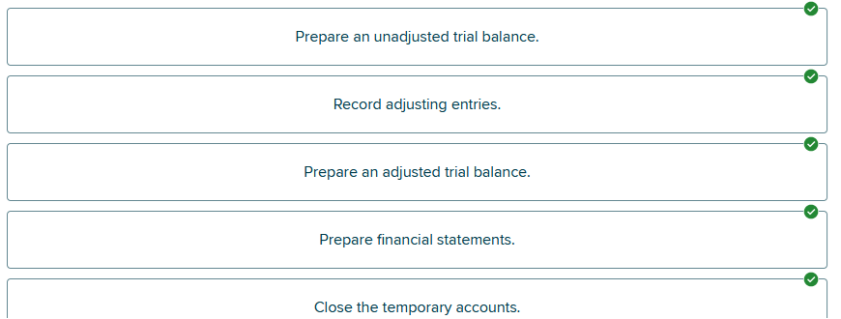

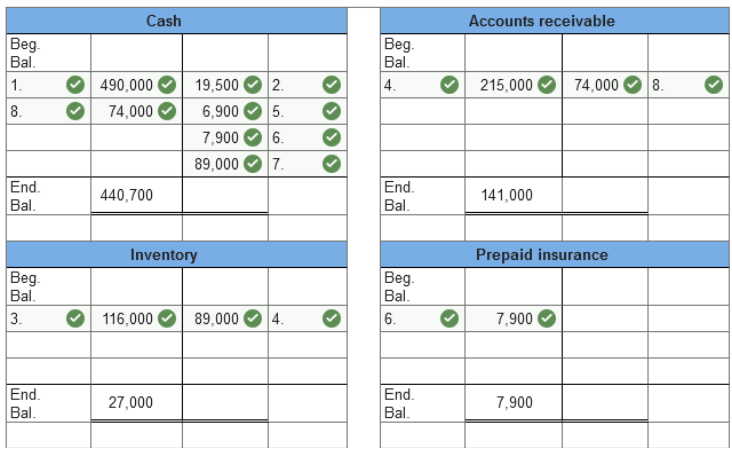

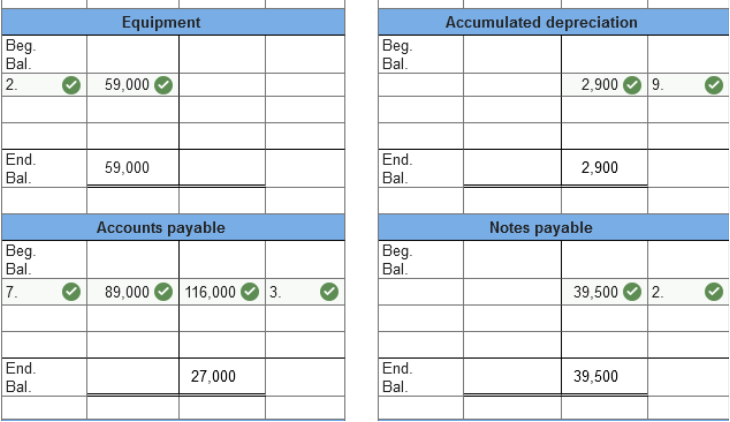

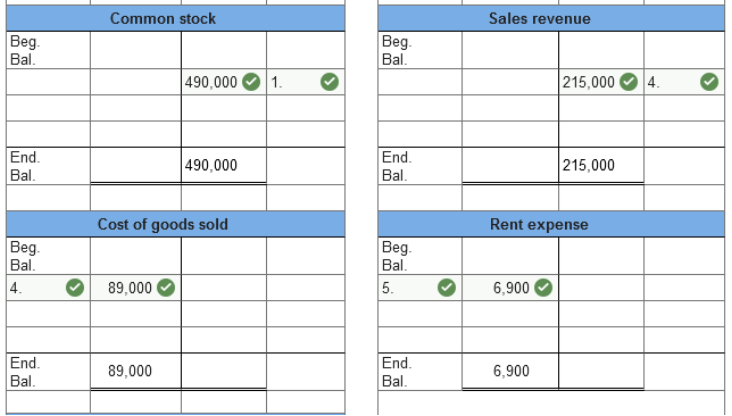

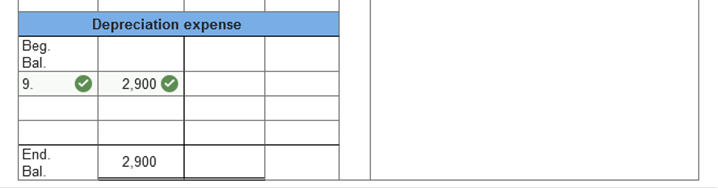

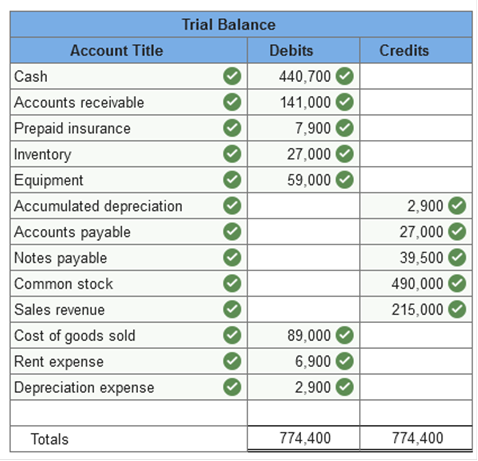

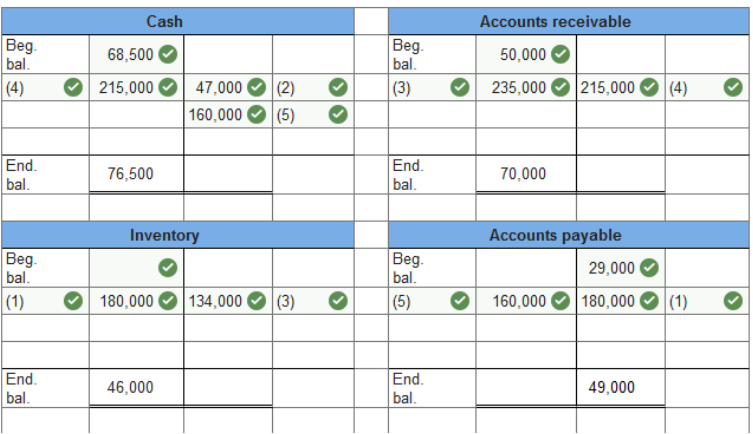

Learning Objective 02-03 Analyze and record transactions using journal entries. Skip to question [The following information applies to the questions displayed below.] After determining the dual effect of external events on the accounting equation, the transaction is recorded in a journal. A journal is a chronological list of transactions in debit/credit form. Which of the following is not a source document? Sales invoices Customer checks Newspaper advertisements Bills from suppliers The payment of utilities for the period would have what effect on the accounting equation? Assets increase; liabilities increase. Assets decrease; owners’ equity decreases. Liabilities increase; owners’ equity decreases. Liabilities decrease; ownership equity increases. The purchase of supplies on account would be recorded in a journal entry with a: Debit to Supplies Credit to Cash Debit to Accounts Payable Credit to Supplies Required information Learning Objective 02-04 Post the effects of journal entries to general ledger accounts and prepare an unadjusted trial balance. Skip to question [The following information applies to the questions displayed below.] The next step in the processing cycle is to periodically transfer, or post, the debit and credit information from the journal to individual general ledger accounts. A general ledger is simply a collection of all of the company’s various accounts. Each account provides a summary of the effects of all events and transactions on that individual account. The process of entering items from the journal to the general ledger is called posting. An unadjusted trial balance is then prepared. On October 1st, a company received $30,000 in cash and a building worth $200,000, and in return, issued common stock to an investor. Create the complete journal entry and post to the appropriate T-accounts.  Post the entry appropriate T-accounts.  A trial balance can best be explained as a list of: The balance sheet accounts used to show the equality of the accounting equation. All accounts and their balances at a particular date. Revenue, expense, and dividend accounts used to show the balances of the components of retained earnings. The income statement accounts used to calculate net income. Which of the following statements regarding adjusting entries is correct? Adjusting entries are recorded for all external transactions. Adjusting entries are recorded to make sure all cash inflows and outflows are recorded in the current period. After adjusting entries, all temporary accounts should have a balance of zero. Adjusting entries are needed because we use accrual-basis accounting. A characteristic of an accrued expense is: Cash is paid, but an expense is never recorded. An expense is recognized, but the cash payment is never paid. Cash payment occurs before expense recognition. The expense is recognized before the payment of cash. Learning Objective 02-06 Record adjusting journal entries in general journal format, post entries, and prepare an adjusted trial balance. Skip to question [The following information applies to the questions displayed below.] Adjusting entries are recorded in the general journal and posted to the ledger accounts at the end of any period when financial statements must be prepared for external use. After these entries are posted to the general ledger accounts, an adjusted trial balance is prepared. Adjusting entries do not need to be posted to the general ledger. True False An adjusted trial balance is a: Trial balance adjusted for cash-basis accounting. List of all accounts and their balances after closing entries. List of all accounts and their balances before adjusting entries. List of all accounts and their balances after adjusting entries. Which statement does not report financial data over a period of time? Income Statement Statement of Stockholders’ Equity Balance Sheet Statement of Cash Flows Learning Objective 02-08 Explain the closing process. [The following information applies to the questions displayed below.] At the end of the fiscal year, a final step in the accounting processing cycle, closing, is required. The closing process serves a dual purpose: (1) the temporary accounts (revenues, expenses. and dividends) are reduced to zero balances, ready to measure activity in the upcoming accounting period, and (2) these temporary account balances are closed (transferred) to retained earnings to reflect the changes that have occurred in that account during the period. After the entries are posted to the general ledger accounts, a post-closing trial balance is prepared. The purpose of closing entries is to transfer: Cash to the owners of the company Assets and liabilities when operations are discontinued. Balances in temporary accounts to a permanent account Inventory to customers The type of system that integrates the information of departments and functions of a company into a single computer system is called a(n) Electronic Data Processing system. Accounting Data system. Enterprise Resource Planning (ERP) system. Which of the following are economic events? (Select all that apply.). A proposal to purchase $1,000 of inventory from supplier. The payment of employee salaries for the week. Borrowing $10,000 from the bank. Which of the following steps occurs only at the end of the year? Obtain information about external transactions from source documents. Record adjusting entries and post to the general ledger accounts. Close the temporary accounts to retained earnings. Prepare the financial statements. Which of the following is the correct formula to calculate cost of goods sold? Ending inventory + purchases - beginning inventory Beginning inventory - purchases + ending inventory Beginning inventory + purchases - ending inventory Beginning inventory + ending inventory – purchases Adjusting entries are recorded: when the financial statements are prepared after closing entries have been prepared at the beginning of an accounting period after the financial statements have been prepared True or false: The objective of an Enterprise Resource Planning (ERP) system is to create a customized software program that integrates the information of departments and functions of a company into a single computer system. True False One of the purposes of adjusting entries is to record all external transactions at the end of the year. ensure debits equal credits. make assets equal liabilities plus owners' equity. recognize all revenues earned during the period. A(n) ___ event is any event that directly affects the financial position of the company. (Enter one word per blank) Economic Adjusting journal entries are necessary for three situations: deferrals, accruals, and ___. (Enter only one word.) Estimates Click and drag on elements in order Place the steps at the end of the accounting period in the correct order.  Prepayments occur when: manufactured goods await quality control inspections. cash flow precedes expense or revenue recognition. customers are unable to pay the full amount due when goods are delivered. sales are delayed pending credit approval. Millburg Corp. uses the periodic inventory method. Millburg's beginning inventory is $10,000. During the year, Millburg purchases $8,000 of inventory. Ending inventory is $5,000. Cost of goods sold is $13,000. $18,000. $7,000. $3,000. Beginning balance $10,000 + $8,000 purchases - $5,000 ending inventory = $13,000 cost of goods sold. Prepaid expenses are: expenses paid at the time incurred. expensed in a later period than cash was paid. expenses incurred before cash is paid. Entries made at the end of the accounting period before the financial statements are prepared are called ___ entries. (Enter only one word.) adjusting The contra account used to record depreciation is ___ depreciation. (Enter only one word.) Accumulated Adjusting entries help a company accurately measure (Select all that apply.) the cash received and paid during the year. revenues and expenses for the period. the company's financial performance. The normal balance in a contra asset account is debit either debit or credit credit Adjusting journal entries are necessary for three situations: deferrals, ___ , and estimates. (Enter only one word.) Accruals A deferred revenue liability appears on the balance sheet for. revenue earned before cash is collected. cash received at the same time revenue is earned. cash received before revenue is earned. Which of the following are examples of prepayments? Purchasing supplies that will be used later. Revenue collected when it is earned. Expense paid when it is incurred. To record an adjusting entry when deferred revenue is recognized: deferred revenue is debited. revenue is credited. revenue is debited. deferred revenue is credited. Prepaid expenses are the cost of ___ acquired in one accounting period and ___ in a future period. (Enter one word per blank.) Assets Expensed Accruals involve transactions where the cash outflow or inflow takes place in a period ______ expense or revenue recognition. before after the same as The balance sheet account that depreciation is recorded to is: accumulated depreciation depreciation expense plant and equipment Expenses incurred in one accounting period and paid for in a future accounting period are ___ liabilities. (Enter only one word.) Accrued The normal balance of the contra asset accumulated depreciation account is a(n) ____ . (Enter one word per blank) Credit True or false: The stated interest rate on debt instruments is always stated as an annual rate. True Deferred revenue is a(n): revenue on the income statement expense on the income statement asset on the balance sheet liability on the balance sheet Interest earned, but not yet received is an example of: an accrued expense a prepaid expense an accrued receivable On October 1, Year 1, Swift Corporation received $1,200 from customers for services to be performed evenly over the next 12 months. Swift recorded the original transaction in a balance sheet account. The adjusting journal entry on December 31, Year 1, will include which of the following entries? Debit revenue $300. Credit to revenue $1,200. Debit to deferred revenue $300. Credit deferred revenue $1,200. How are items classified on the income statement? current and noncurrent assets and liabilities operating and nonoperating operating, investing, and financing Recognizing revenue before cash flow is an example of: an accrual adjusting entry. a prepayment adjusting entry. an estimate adjusting entry. The process in which temporary accounts are reduced to zero balances and transferred to retained earnings is the ______ process. closing zero adjusting opening Accrued liabilities are costs incurred in an accounting period: before a cash payment after a cash payment at the same time of a cash payment ___ basis accounting measures income based on accomplishments and resource sacrifices during the period. (Enter only one word.) Accrual ___ basis accounting measures the difference between cash receipts and cash disbursements during a reporting period. (Enter only one word.) Cash On July 1, Perry Company signed a note with principal of $80,000 and a stated interest rate of 4%. The principal and interest are due on April 1 of the following year. Perry will accrue interest on December 31st of $4,800 $3,200 $0 $1,600 An accrued receivable occurs when revenue is earned: at the same time as cash flow before cash flow after cash flow The components of the income statement are usually classified as: (Select all that apply.) financing items operating items investing items non-operating items The first step in the closing process is to reduce the balances in the temporary accounts to zero. The second step is to transfer the effects of step 1 to which account? retained earnings cash common stock dividends Accrual accounting measures: the difference between cash receipts and cash disbursements an entity's accomplishments and resource sacrifices during the period net income relative to timing of cash movement Exercise 2-3 (Algo) T-accounts and trial balance [LO2-4] The following transactions occurred during March 2021 for the Wainwright Corporation. The company owns and operates a wholesale warehouse. Issued 49,000 shares of common stock in exchange for $490,000 in cash. Purchased equipment at a cost of $59,000. $19,500 cash was paid and a notes payable to the seller was signed for the balance owed. Purchased inventory on account at a cost of $116,000. The company uses the perpetual inventory system. Credit sales for the month totaled $215,000. The cost of the goods sold was $89,000. Paid $6,900 in rent on the warehouse building for the month of March. Paid $7,900 to an insurance company for fire and liability insurance for a one-year period beginning April 1, 2021. Paid $89,000 on account for the merchandise purchased in 3. Collected $74,000 from customers on account. Recorded depreciation expense of $2,900 for the month on the equipment. Post the above transactions to the below T-accounts. Assume that the opening balances in each of the accounts is zero. Prepare a trial balance from the ending account balances. Post the above transactions to the below T-accounts. Assume that the opening balances in each of the accounts is zero. (Enter the number of the transaction in the column next to the amount.)     Prepare a trial balance from the ending account balances.  Exercise 2-13 (Algo) Closing entries [LO2-8] American Chip Corporation’s reporting year-end is December 31. The following is a partial adjusted trial balance as of December 31, 2021.

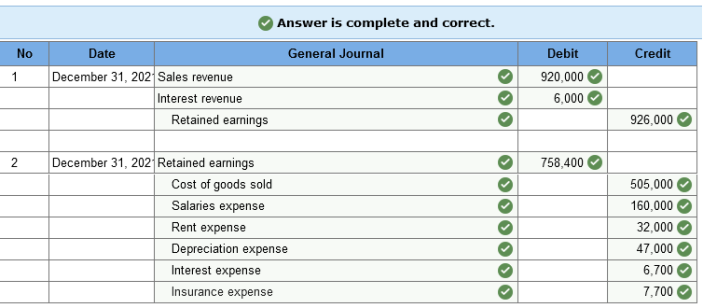

Required: Prepare the necessary closing entries at December 31, 2021. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)  Exercise 2-15 (Algo) Cash versus accrual accounting; adjusting entries [LO2-5, 2-6, 2-9] The Righter Shoe Store Company prepares monthly financial statements for its bank. The November 30 and December 31, 2021, trial balances contained the following account information:

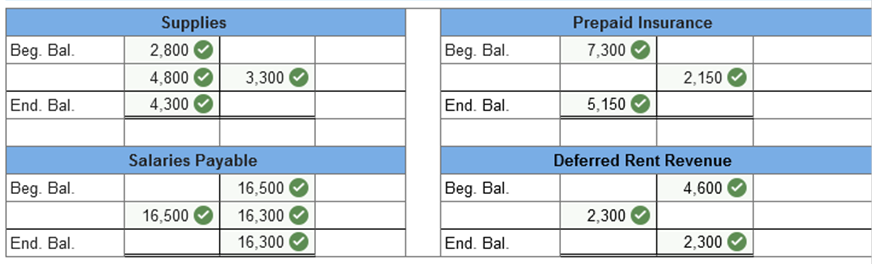

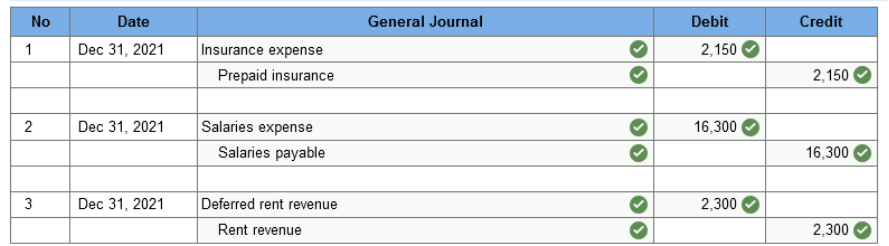

The following information also is known: The December income statement reported $3,300 in supplies expense. No insurance payments were made in December. $16,500 was paid to employees during December for salaries. On November 1, 2021, a tenant paid Righter $6,900 in advance rent for the period November through January. Deferred rent revenue was credited. Required: 1. Using the above information for December, complete the T-accounts below. The beginning balances should be the balances as of November 30. 2. Using the above information, prepare the adjusting entries Righter recorded for the month of December.   The following transactions occurred during 2021 for the Beehive Honey Corporation:

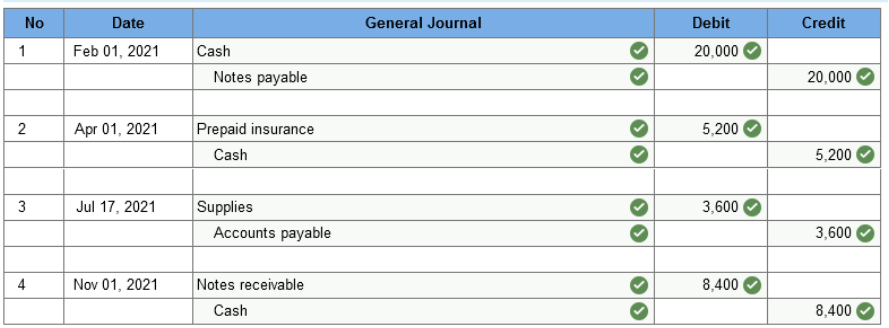

Required: 1. Record each transaction in general journal form. 2. Prepare any necessary adjusting entries at the year-end on December 31, 2021. No adjusting entries were recorded during the year for any item. Record each transaction in general journal form. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)  Prepare any necessary adjusting entries at the year-end on December 31, 2021. No adjusting entries were recorded during the year for any item. (Do not round intermediate calculations. If no entry is required for a particular transaction/event, select, "No journal entry required" in the first account field.)  Pastina Company sells various types of pasta to grocery chains as private label brands. The company’s reporting year-end is December 31. The unadjusted trial balance as of December 31, 2021, appears below.

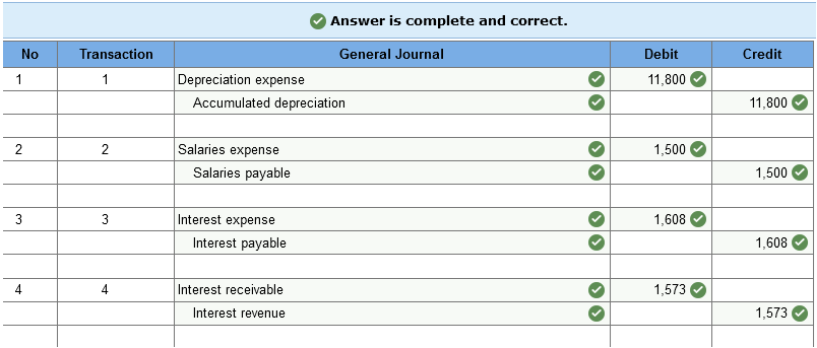

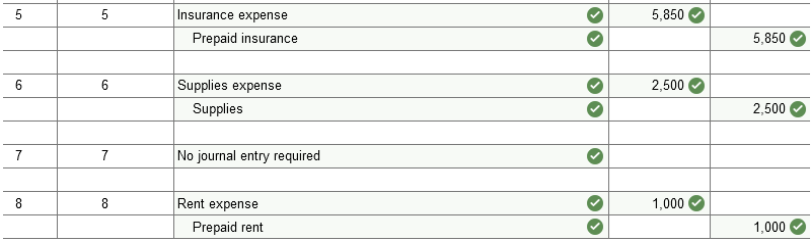

Information necessary to prepare the year-end adjusting entries appears below. · Depreciation on the office equipment for the year is $11,800. · Employee salaries are paid twice a month, on the 22nd for salaries earned from the 1st through the 15th, · and on the 7th of the following month for salaries earned from the 16th through the end of the month. · Salaries earned from December 16 through December 31, 2021, were $1,500. · On October 1, 2021, Pastina borrowed $53,600 from a local bank and signed a note. The note requires interest to be paid annually on September 30 at 12%. The principal is due in 10 years. · On March 1, 2021, the company lent a supplier $23,600 and a note was signed requiring principal, and interest at 8% to be paid on February 28, 2022. · On April 1, 2021, the company paid an insurance company $7,800 for a one-year fire insurance policy. The entire $7,800 was debited to prepaid insurance. · $800 of supplies remained on hand at December 31, 2021. · A customer paid Pastina $1,200 in December for 1,608 pounds of spaghetti to be delivered in January 2022. Pastina credited deferred sales revenue. · On December 1, 2021, $2,000 rent was paid to the owner of the building. The payment represented rent for December 2021 and January 2022, at $1,000 per month. The entire amount was debited to prepaid rent. Required: Prepare the necessary December 31, 2021, adjusting journal entries. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Do not round intermediate calculations. Round your final answers to nearest whole dollar amount.)   Problem 2-8 (Algo) Adjusting entries [LO2-6] Excalibur Corporation sells video games for personal computers. The unadjusted trial balance as of December 31, 2021, appears below. December 31 is the company’s reporting year-end. The company uses the perpetual inventory system.

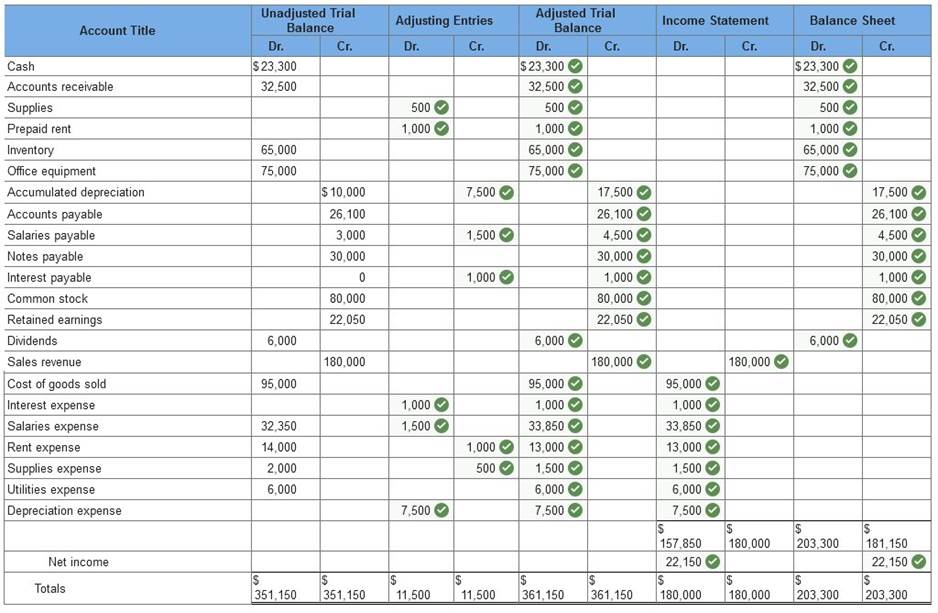

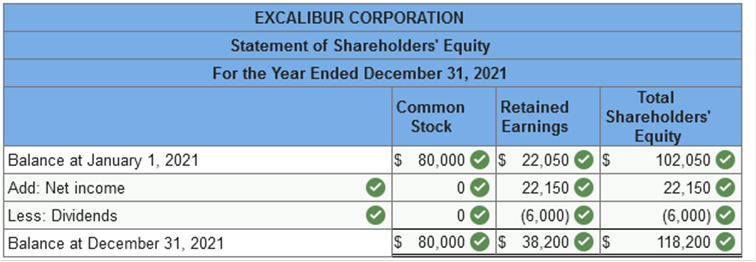

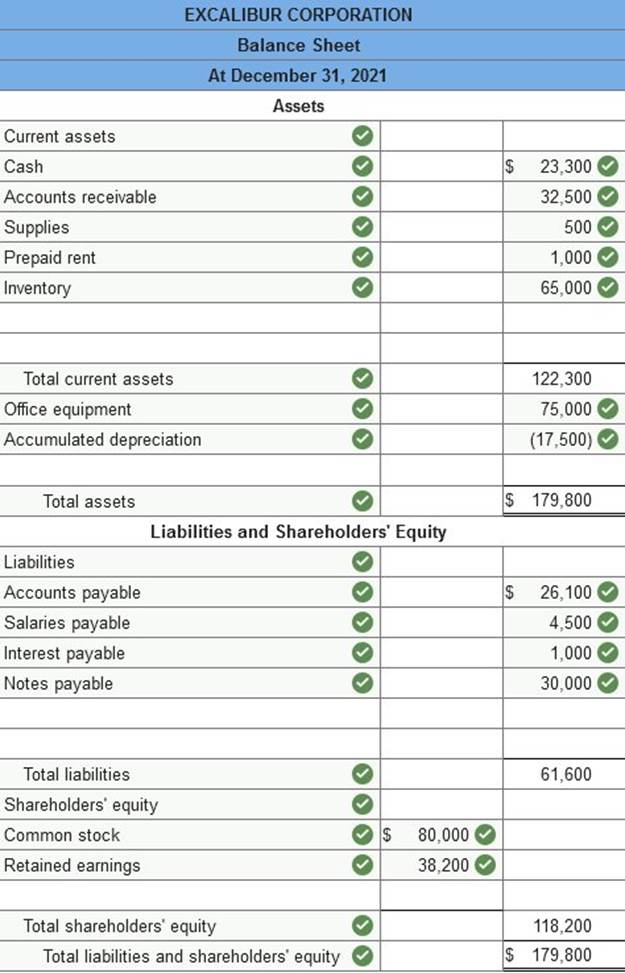

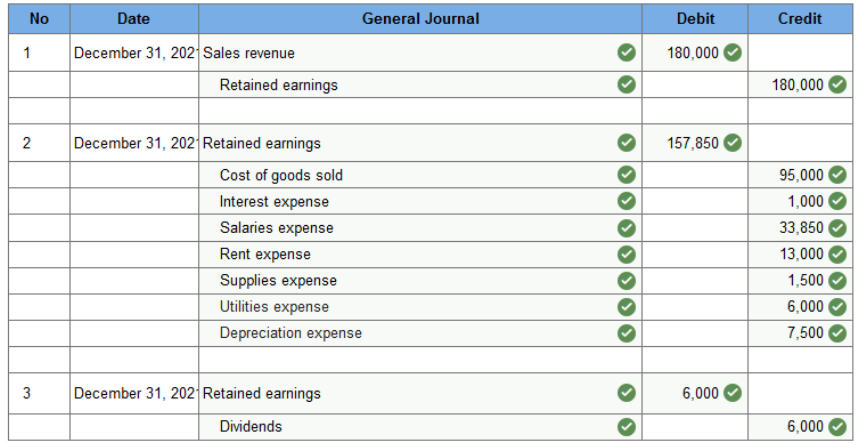

Information necessary to prepare the year-end adjusting entries appears below. · The office equipment was purchased in 2019 and is being depreciated using the straight-line method over an nine-year useful life with no salvage value. · Accrued salaries at year-end should be $5,250. · The company borrowed $35,000 on September 1, 2021. The principal is due to be repaid in 12 years. Interest is payable twice a year on each August 31 and February 28 at an annual rate of 12%. · The company debits supplies expense when supplies are purchased. Supplies on hand at year-end cost $550. · Prepaid rent at year-end should be $1,500. Required: Prepare the necessary December 31, 2021, adjusting entries. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field. Do not round intermediate calculations.)  Problem 2-13 (Static) Worksheet [Appendix 2A] Excalibur Corporation sells video games for personal computers. The unadjusted trial balance as of December 31, 2021, appears below. December 31 is the company's reporting year-end. The company uses the perpetual inventory system.

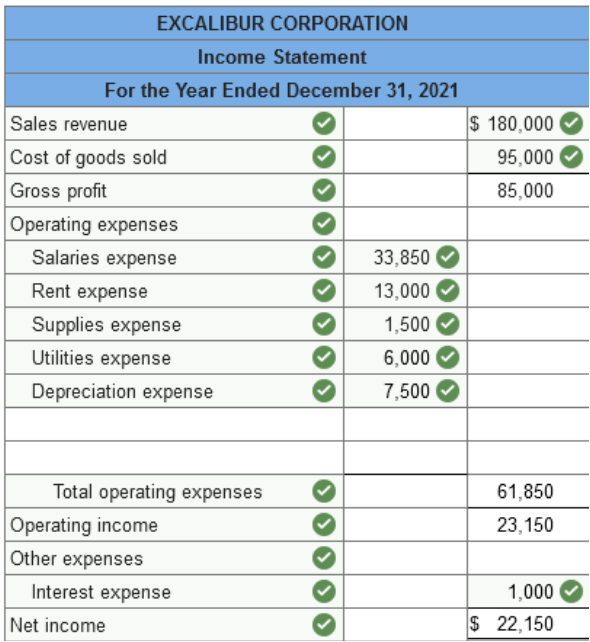

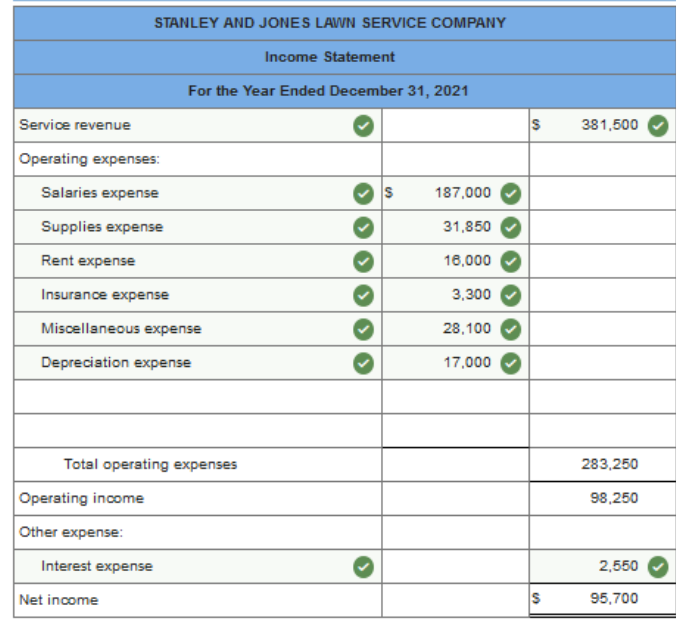

Information necessary to prepare the year-end adjusting entries appears below. The office equipment was purchased in 2019 and is being depreciated using the ten useful life with no salvage value. Accrued salaries at year-end should be $4,500. The company borrowed $30,000 on September 1, 2021. The principal is due to be repaid in 10 years. Interest is payable twice a year on each August 31 and February 28 at an annual rate of 10%. The company debits supplies expense when supplies are purchased. Supplies on hand at year-end cost $500. Prepaid rent at year-end should be $1,000. 1. Complete the worksheet below. 2-a. Use the information in the worksheet to prepare an income statement for 2021. 2-b. Use the information in the worksheet to prepare a statement of shareholders’ equity for 2021. 2-c. Use the information in the worksheet to prepare a balance sheet as of December 31, 2021. 3. Prepare the necessary closing entries assuming that adjusting entries have been correctly posted to the accounts.      Exercise 2-18 (Algo) Cash versus accrual accounting [LO2-9] Stanley and Jones Lawn Service Company (S&J) maintains its books on a cash basis. However, the company recently borrowed $170,000 from a local bank, and the bank requires S&J to provide annual financial statements prepared on an accrual basis. During 2021, the following cash flows were recorded:

You are able to determine the following information about accounts receivable, prepaid expenses, and accrued liabilities:

In addition, you learn that the bank loan was dated September 30, 2021, with principal and interest at 6% due in one year. Depreciation on the company’s equipment is $17,000 for the year. Required: Prepare an accrual basis income statement for 2021. (Ignore income taxes.)  When a business makes an end-of-period adjusting entry with a debit to supplies expense, the usual credit entry is made to: Supplies The income statement summarizes the operating activity of a company at a particular point in time. False A revenue. An asset. A liability. A contra asset until used. Dave's Duds reported cost of goods sold of $2,000,000 this year. The inventory account increased by $220,000 during the year to an ending balance of $595,000. What was the cost of merchandise that Dave's purchased during the year? $2,595,000. $2,220,000. $1,405,000. $1,780,000. Explanation

Purchases = $2,000,000 − $375,000 + $595,000 = $2,220,000 Fink Insurance collected premiums of $18,200,000 from its customers during the current year. The adjusted balance in the Deferred premiums revenue account increased from $5.0 million to $10.0 million dollars during the year. What is Fink's revenue from insurance premiums recognized for the current year? $23,200,000. $13,200,000. $18,200,000. $8,200,000. Explanation

Carolina Mills purchased $270,000 in supplies this year. The supplies account increased by $13,000 during the year to an ending balance of $67,000. What was supplies expense for Carolina Mills during the year? $309,000. $231,000. $257,000. $283,000. Explanation

Supplies expense = $54,000 + $270,000 − $67,000 = $257,000 On December 31, 2020, Coolwear, Inc. had a balance in its prepaid insurance account of $50,400. During 2021, $88,000 was paid for insurance. At the end of 2021, after adjusting entries were recorded, the balance in the prepaid insurance account was $43,000. Insurance expense for 2021 was: $95,400. $138,400. $88,000. $7,400. Explanation Insurance expense = $50,400 + $88,000 − $43,000 = $95,400 The supplies account increased by $10,000 during the year to an ending balance of $66,000. What was supplies expense for Carolina Mills during the year? $300,000. $280,000. $260,000. $240,000. Explanation

Supplies expense = $56,000 + $270,000 – $66,000 = $260,000 On September 1, 2021, Fortune Magazine sold 600 one-year subscriptions for $81 each. The total amount received was credited to Deferred subscription revenue. What is the required adjusting entry at December 31, 2021? Multiple Choice Deferred subscription revenue 48,600 Subscription revenue 16,200 Prepaid subscriptions 32,400 Deferred subscription revenue 16,200 Subscription revenue 16,200 Deferred subscription revenue 16,200 Subscription payable 16,200 Deferred subscription revenue 32,400 Subscription revenue 32,400 Explanation

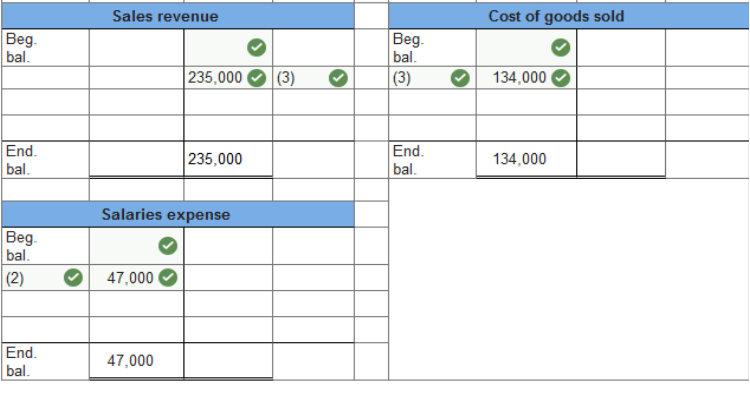

Amount recorded as revenue: $48,600 × 4/12 (4 months expired) = $16,200 The Marchetti Soup Company entered into the following transactions during the month of June: (1) purchased inventory on account for $180,000 (assume Marchetti uses a perpetual inventory system); (2) paid $47,000 in salaries to employees for work performed during the month; (3) sold merchandise that cost $134,000 to credit customers for $235,000; (4) collected $215,000 in cash from credit customers; and (5) paid suppliers of inventory $160,000. Post the above transactions to the below T-accounts. Assume that the opening balances in each of the accounts is zero except for cash, accounts receivable, and accounts payable that had opening balances of $68,500, $50,000, and $29,000, respectively. (Enter the transaction number in the column next to the amount.)   Making insurance payments in advance is an example of: An accrued receivable transaction. An accrued liability transaction. A deferred revenue transaction. A prepaid expense transaction. After an unadjusted trial balance is prepared, the next step in the accounting processing cycle is the preparation of financial statements. False The balance in retained earnings at the end of the year is determined by retained earnings at the beginning of the year: Plus revenues, minus liabilities. Plus accruals, minus deferrals. Plus net income, minus dividends. Plus assets, minus liabilities. The employees of Neat Clothes work Monday through Friday. Every other Friday the company issues payroll checks totaling $40,000. The current pay period ends on Friday, July 3. Neat Clothes is now preparing quarterly financial statements for the three months ended June 30. What is the adjusting entry to record accrued salaries at the end of June? Salaries expense 8,000 Salaries payable 8,000 Salaries expense 28,000 Salaries payable 28,000 Salaries expense 28,000 Prepaid salaries 12,000 Salaries payable 40,000 Prepaid salaries 12,000 Salaries payable 12,000 Explanation Amount accrued: $40,000 × 7/10 (7 days of 10 days to be paid) = $28,000 Somerset Leasing received $55,200 for 12 months' rent in advance. How should Somerset record this transaction? Prepaid rent 55,200 Rent expense 55,200 Cash 55,200 Deferred rent revenue 55,200 Interest expense 55,200 Interest payable 55,200 Salaries expense 55,200 Salaries payable 55,200 On December 31, 2021, the end of Larry's Used Cars' first year of operations, the accounts receivable was $54,100. The company estimates that $2,500 of the year-end receivables will not be collected. Accounts receivable in the 2021 balance sheet will be valued at: $2,500. $56,600. $54,100. $51,600. Explanation Accounts receivable = $54,100 − $2,500 = $51,600 On September 15, 2021, Oliver's Mortuary received a $3,600, nine-month note bearing interest at an annual rate of 8% from the estate of Jay Hendrix for services rendered. Oliver's has a December 31 year-end. What adjusting entry will the company record on December 31, 2021? Interest receivable 204 Interest revenue 204 Interest receivable 84 Interest revenue 84 Interest receivable 84 Notes receivable 84 Interest receivable 288 Interest revenue 84 Cash 204 Explanation Accrued interest revenue: $3,600 × 8% × 3.5/12 = $84 The adjusting entry required when amounts previously recorded as deferred revenues are recognized includes: A debit to a liability. A debit to an asset. A credit to a liability. A credit to an asset. Somerset Leasing received $12,000 for 12 months' rent in advance. How should Somerset record this transaction? Prepaid rent 12,000 Rent expense 12,000 Cash 12,000 Deferred rent revenue 12,000 Interest expense 12,000 Interest payable 12,000 Salaries expense 12,000 Salaries payable 12,000 A company has a fiscal year-end of December 31: (1) on October 1, $17,000 was paid for a one-year fire insurance policy; (2) on June 30 the company advanced its chief financial officer $15,000; principal and interest at 5% on the note are due in one year; and (3) equipment costing $65,000 was purchased at the beginning of the year for cash. Depreciation on the equipment is $13,000 per year. Prepare the necessary adjusting entries at December 31 for each of the above items. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)  Explanation Insurance expense = $17,000 × 3/12 = $4,250 Interest receivable = $15,000 × 5% × 6/12 = $375 Intermediate Accounting Homework 1 2 3 4 5 6 7 8 9 10 11 | Exams Chapters 1-3 4-7 8-9 10-11

| Final Exam

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Home |

Accounting & Finance | Business |

Computer Science | General Studies | Math | Sciences |

Civics Exam |

Everything

Else |

Help & Support |

Join/Cancel |

Contact Us |

Login / Log Out |